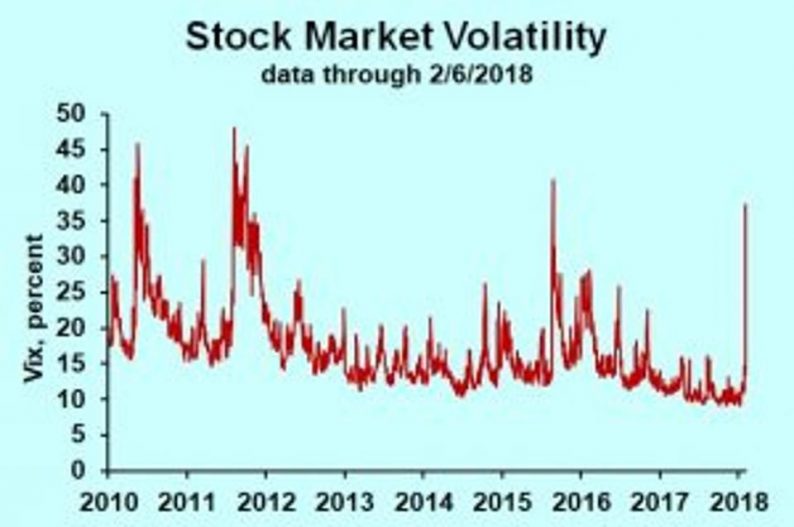

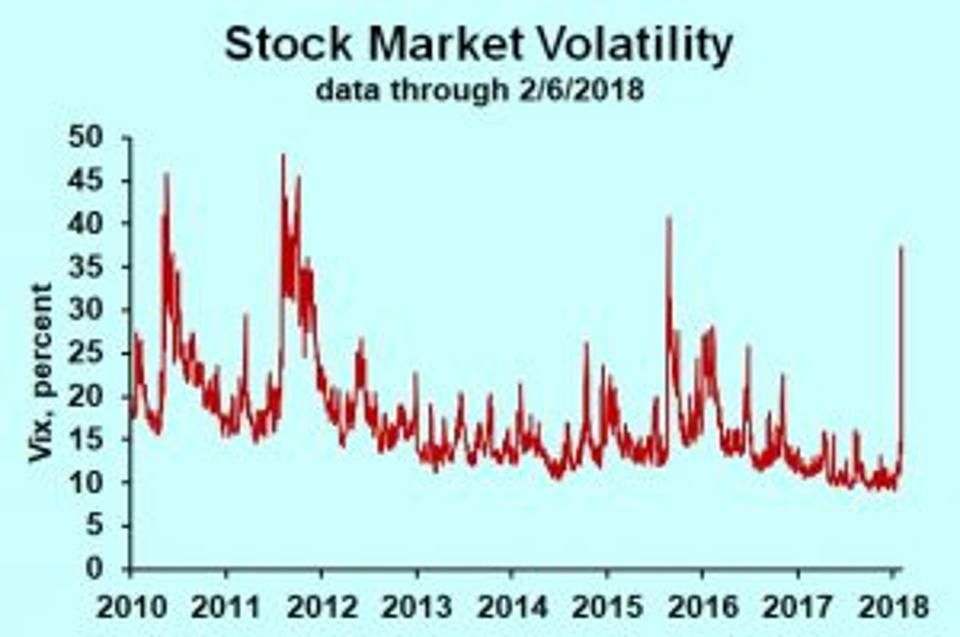

VIX — volatility index Dr. Bill Conerly based on CBOE data.

The cause of stock market volatility is different than the cause of bull markets or bear markets. The direction of stock market change is based on estimates of future business conditions relative to alternative uses of capital. But rapid changes in valuation, either up or down, indicate that investors feel a weak basis for their expectations.

When I have a view that I hold with great confidence, then my estimates are well-anchored. It takes a lot of evidence for me to change my mind. But I may have the exact same prediction of future corporate earnings only with weak anchoring. I have a view, but very low confidence that I’m right. New evidence in one direction or another can easily change my mind.

The long bull market reflected rising expectations for business conditions, and it was accompanied by very low volatility, indicating well-anchored expectations.

I felt this rise in volatility coming. At least in hindsight, I can see that it was coming. I speak at many business conferences, and there are always a few people asking me about investments. Over the past few months, though, everyday folks kept asking me what I thought of the stock market. Investors increasingly feared a market correction, though they seemed to lack a basis for a gloomy prediction. (Certainly some people have had a basis for gloom, but they tended to be the people who are always gloomy.) What was different was that folks who had been confident buy-and-hold investors were now wondering if they should take some chips off the table.

With weakly anchored expectations, a small piece of information can swing the market. A small market correction is itself a piece of information that can become a self-fulfilling prophecy.

Stock market volatility is more easily understood with the recognition that markets don’t reflect the current economy so much as expectations for the future economy. And a small change in expectations for the future can justify a substantial change in today’s valuation. Around the world, economists have been dialing up their predictions for 2018 and 2019. The effects of tax reform are generally thought to be small, but an increment to growth rates of a tenth of a percent or two, compounded over a decade, can swing current valuations. Similarly, fear of inflation, compounded over a few years, justifies some pessimism.

Related Posts

Breaking: DCG owes creditors over $3B, considering $500M VC portfolio sale

Breaking: DCG owes creditors over $3B, considering $500M VC portfolio sale Is the Bitcoin price dip toward $40K a bear trap?

Is the Bitcoin price dip toward $40K a bear trap? The Oil Short Squeeze Explained: Why Banks Are Aggressively Propping Up Energy Stocks

The Oil Short Squeeze Explained: Why Banks Are Aggressively Propping Up Energy Stocks Commodities Popped Last Week Amid Weakness Elsewhere

Commodities Popped Last Week Amid Weakness Elsewhere Today, Investor Interest Is Focused On The FOMC Minutes

Today, Investor Interest Is Focused On The FOMC Minutes Binance cuts withdrawal limits, rolls out tax reporting tool

Binance cuts withdrawal limits, rolls out tax reporting tool

Leave A Comment