An Alert for the Global Posse of Liquidity Junkies

In the summer of 2015 and again in December-February this year, global stock markets were rattled by weakness in the yuan’s exchange rate vs. the US dollar. Yuan weakness is widely held to exacerbate pressures on other (already weak) emerging market currencies, but more importantly, it is seen as a symptom of accelerating capital flight from China.

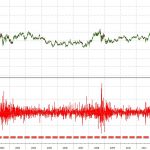

USD-CNY, daily (a rising price denotes yuan weakness) – slowly creeping toward Panicville again? Resistance is between 6.60 and 6.65 –we suspect that if that level is exceeded, all hell could break loose again

Why is it considered important whether or not China’s foreign exchange reserves are increasing or declining? Similar to Japan, China has become a major cog in the global fiat money Ponzi game, in which foreign central banks monetize US treasury bonds by recycling dollar-denominated trade surpluses.

Now, it should be clear that the term “monetization” does not refer to the creation of additional US dollars in this case – those can only be created by the Fed and the US banking system. Rather, foreign CBs are boosting their domestic money supply when they buy dollars from their exporters – since they are paying for these dollars with domestic currency they create out of thin air.

In China the effect of dollar inflows on the domestic money supply is especially pronounced. In fact, in order to stem the pace of money supply and credit growth lest it get out of hand completely, the PBoC has imposed one of the highest minimum reserve requirements in the world and is regularly altering it to influence credit and money supply growth in the country.

By way of the minimum reserve requirement the PBoC intends to at least brake additional growth of the yuan money supply (beyond the growth caused directly by its USD purchases) to some extent, i.e., money supply growth which its fractionally reserved banks are generating by granting ever more inflationary credit.

Related Posts

WalMart Carnage: Stock Plummets Most In 17 Years After Slashing Earnings Guidance, Blames Wage Hikes

WalMart Carnage: Stock Plummets Most In 17 Years After Slashing Earnings Guidance, Blames Wage Hikes Are we misguided about Bitcoin mining’s environmental impacts? Slush Pool’s CMO Kristian Csepcsar explains

Are we misguided about Bitcoin mining’s environmental impacts? Slush Pool’s CMO Kristian Csepcsar explains China’s Big Decline Providing A Sweet Entry Point

China’s Big Decline Providing A Sweet Entry Point Wells Drying Up At JPMorgan: Time To Sell

Wells Drying Up At JPMorgan: Time To Sell E

Six Weeks Of Dollar Bears – Are We Due For A Sharp Reversal?

E

Six Weeks Of Dollar Bears – Are We Due For A Sharp Reversal? Are Wages All The Rage Or Is It Profit Taking?

Are Wages All The Rage Or Is It Profit Taking?

Leave A Comment