Currencies appreciate and depreciate for many reasons and either extreme isn’t necessarily good or bad. Traditional economic theory holds that a cheaper domestic currency relative to other trading partners reduces imports and boosts exports as our widgets become cheaper from the perspective of other countries and inflation pressures rise as imports become more expensive. In the limited history of free floating global currencies, this accepted model garners too much attention. When Trump’s Treasury Secretary last week implied Trump wants a lower Dollar, the stock market sold off quickly on fears of higher inflation of imported goods and an exodus from US Treasury debt holdings by foreigners. We wrote at the time that this was Fake News as Mnuchin really didn’t care about the Dollar’s value – up or down. Sure enough, the next day Trump came out and stated the opposite, that the US Dollar should be stronger. Stocks zoomed back to new record highs as the status quo was preserved.

Mnuchin: “Obviously a weaker dollar is good for us as it relates to trade” 01-24-18 ?

Trump: “I want to see a strong dollar” 01-25-18

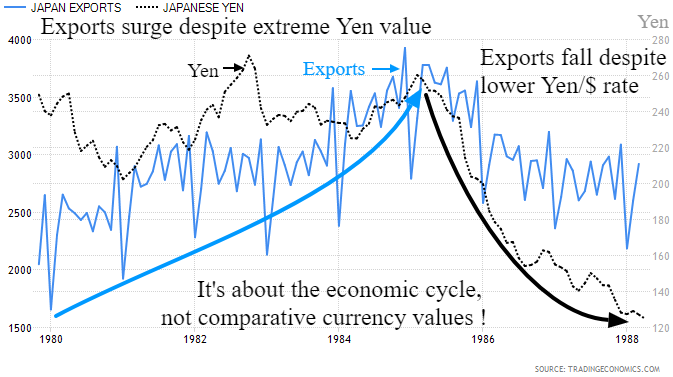

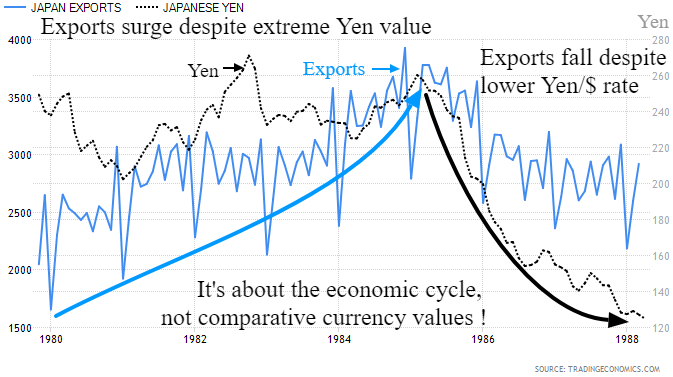

Trump may actually want a lower Dollar, but so much worry over the Dollar is mostly unfounded. In the 1970’s and 80’s when the vaunted Japanese Yen was astronomically over valued -triple its current level – their exports were soaring, contrary to economic expectations. In the 1970’s through 1990’s every President demanded a weaker Yen and a stronger Dollar, assuming this would reduce our huge trade deficit with Japan. That Trade deficit with Japan remains close to $70 Billion despite an over 70% depreciation of the Yen since the 1970’s.

Trump has continued the Yen bashing tradition with China as our new trade deficit enemy, calling for a stronger Chinese Yuan – weaker dollar policy during his Presidential campaign. Such Government policies are ineffective as imports and exports “always” move together with the economy regardless of currency trends. There is some evidence that imports grow relatively faster than exports when the Dollar appreciates and the reverse is true, to some degree. However, there are many factors more important to trade and inflation than currency values, such as tariffs, regulations and the stage of the economic cycle. When the US Dollar rose in the 1980’s and 90’s expansion cycles, our exports grew at a very healthy pace, yet when the Dollar fell in the early 2,000’s, exports also expanded at a similar rate. Governments should look at their currency as more of a byproduct of economic policy rather than a vehicle to manipulate for an illusive trade war benefit.

Related Posts

Forex Forecast: Pairs In Focus – March 11

Forex Forecast: Pairs In Focus – March 11- What Do They Know?

Indicators Suggest Some Caution Still Warranted

Indicators Suggest Some Caution Still Warranted USD/JPY Breakout Attempt Foreshadowing ’Risk’ Rally?

USD/JPY Breakout Attempt Foreshadowing ’Risk’ Rally? Price analysis 6/17: BTC, ETH, BNB, ADA, XRP, SOL, DOGE, DOT, LEO, AVAX

Price analysis 6/17: BTC, ETH, BNB, ADA, XRP, SOL, DOGE, DOT, LEO, AVAX Tech Sell-Off Continues: Here’s Why Value Is Eating FB’s And AMZN’s Lunch

Tech Sell-Off Continues: Here’s Why Value Is Eating FB’s And AMZN’s Lunch

Leave A Comment