Rio Tinto (NYSE: RIO) is one of the world’s leading miners.

It has been in business for 140 years and employs 50,000 workers in 35 countries. The company mines for aluminum, copper, diamonds, uranium and various other natural resources.

But our SafetyNet Pro’s analysis of the company tells a different story…

Last year, holders of its American depositary receipts (ADRs) received $1.70 in dividends, which equals a 3.9% yield on today’s price. The company has not declared a dividend yet for this year.

ADRs are traded on U.S. exchanges and represent shares of companies traded on foreign exchanges.

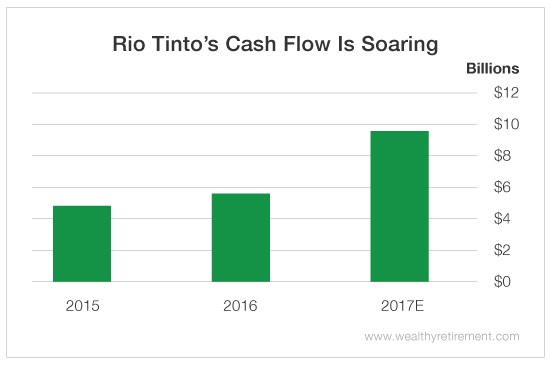

The company’s cash flow is forecast to soar this year to $9.6 billion from half that amount in 2015.

Meanwhile, Rio Tinto is expected to pay just $3.9 billion in dividends this year, a payout ratio of 41%.

The payout ratio is the percentage of earnings or cash flow paid out in dividends.

I like to see companies with payout ratios below 75%. That gives me confidence that the dividend can be maintained even if cash flow dips during a difficult period.

At just 41%, Rio Tinto has plenty of room to navigate before it has to cut the dividend if its business hits a rough patch.

So the company shouldn’t have a problem paying its dividend in the near future.

But its dividend-paying history is worth considering.

It eliminated the dividend entirely in 2009. And last year, the company lowered the dividend by 23%.

So Rio Tinto isn’t afraid to cut the dividend when it feels it needs to. In other words, the dividend is not sacrosanct in the eyes of management.

That should make investors who rely on the company’s dividend less confident.

Rio Tinto can afford to pay its dividend now. But investors shouldn’t get too comfortable with the idea of the dividend being sustained over the long term. Any serious bumps in the road will likely lead to a dividend cut in the future.

Dividend Safety Rating: C

Related Posts

JPMorgan Q4 Earnings Beat Thanks To Investment Banking

JPMorgan Q4 Earnings Beat Thanks To Investment Banking Exploring The Growth Of Medicaid Managed Care

Exploring The Growth Of Medicaid Managed Care- J.B. Hunt (JBHT) Q3 Earnings Miss Estimates, Sales Beat

- 3 Excellent Dividend ETFs For Turbulent Times

“Peddling Fiction” – US Economy Grew A Paltry 0.69% In The Fourth Quarter, Missing Expectations

“Peddling Fiction” – US Economy Grew A Paltry 0.69% In The Fourth Quarter, Missing Expectations- Luxottica and Essilor see eye-to-eye in merger

Leave A Comment