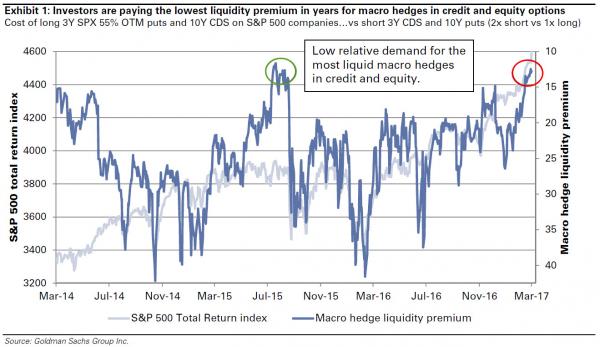

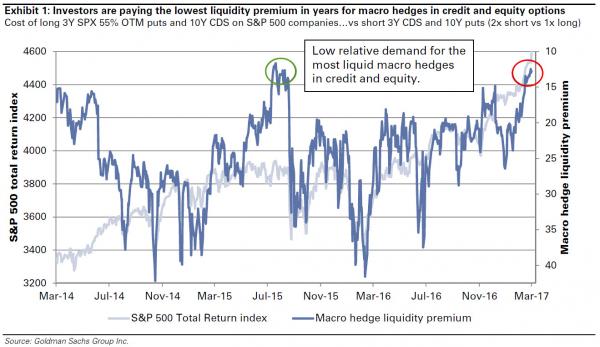

In early March, Goldman’s John Marshall looked at the firm’s proprietary macro hedging indicator and found something peculiar: investors were buying stocks and discarding protection. As Marshall said at the time, this was a reflection of “How Trump Changed the Market”, and said added that “the cost of liquid long-dated hedges in equity and credit has collectively reached its lowest level in six years following the decline this week. The last time macro hedge costs were near this level across assets was in July 2015.”

He then warned that “while not likely the cause of the pullback in August of 2015 (the mini-flash crash), the lack of hedges in investor portfolios likely exacerbated the sell-off.”

Fast forward to today, when the most read piece of research on Goldman’s portal is the follow up piece from Marshall. Clearly, while the market has failed to sell off even modestly let along in a rerun of August 2015, Goldman has found a particularly “compelling” short-term divergence between credit and equity which it believes could lead to a quick and profitable convergence trade.

As Marhsall explains, credit has significantly outperformed equity over the past month on a risk-adjusted basis. More specifically, CDX IG 5Y has outperformed its corresponding equities by 1.8, 1.0, 1.3 and 2.0 standard deviations over the past 1, 2, 3 and 4 months, respectively. Marshall views this as an attractive entry point for relative value trades, i.e. a compression trade:

“For investors looking for a macro hedge, credit offers more attractive hedging opportunities. For investors adding to bullish positions, equity offers more attractive buying opportunities.”

The divergence in question:

And even more gaping divergence: between CDX HY and corresponding stocks:

Meanwhile, an example of where the trade does not show the above divergences, is in Europe where ITRAXX and equities have traded in line.

Related Posts

Adjusting Debt Levels Based On Interest Rates

Adjusting Debt Levels Based On Interest Rates Durable Goods Orders Plunge 2.8%; Will A Falling Dollar Soon Help?

Durable Goods Orders Plunge 2.8%; Will A Falling Dollar Soon Help? Now What?

Now What? ‘Hawkish’ Fed Minutes Crush Yield Curve To Flattest Since Start Of Last Recession

‘Hawkish’ Fed Minutes Crush Yield Curve To Flattest Since Start Of Last Recession JPMorgan Lists Six “Red Flags” Why It Is Starting To Sell Stocks

JPMorgan Lists Six “Red Flags” Why It Is Starting To Sell Stocks Five Decades Of Middle-Class Wages: January 2017 Update

Five Decades Of Middle-Class Wages: January 2017 Update

Leave A Comment