Microsoft (MSFT) is a company legendary for making many investors very wealthy over the decades.

In fact, Bill Gates’ dividend stock portfolio would not exist if it weren’t for Microsoft’s incredible growth story.

Over the past 14 years the company has become a favorite among many dividend investors, thanks to its dividend achiever status and 15% annual payout growth rate over the last decade.

Let’s take a closer look at Microsoft’s business, including the important ways that management is pivoting the company to take advantage of the disruptive technology of the future.

Most importantly, learn if Microsoft’s strategy is likely to make it a solid long-term core holding for diversified dividend growth portfolios, such as our Top 20 Dividend Stocks portfolio.

Business Overview

Founded in 1975 in Redmond, Washington, Microsoft is most famous for its Windows operating system, which runs approximately 87% of the world’s computers.

However, in recent decades the company has vastly diversified its operations to become a software and hardware powerhouse, operating in over 190 countries around the globe.

Microsoft now operates three distinct business segments:

Productivity and Business Processes: Office 365 commercial and consumer product suites, which include Office, Exchange, Outlook.com, Skype, and OneDrive cloud solutions for businesses and individuals.

Intelligent Cloud Services: Server and cloud based solutions, including its fast-growing Azure business cloud platform.

Personal Computing: Traditional Windows business on PCs, as well as Xbox gaming platform, and Bing search engine.

As you can see below, Microsoft’s legacy personal computing business remained the dominant revenue driver in 2016.

However, the company’s faster-growing business productivity and intelligent cloud businesses were the big cash cows when it came to operating profits.

These segments earn higher margins because they are less commoditized and provide higher value. They will be the most important dividend growth for the company going forward.

Source: 2016 Annual Report

Business Analysis

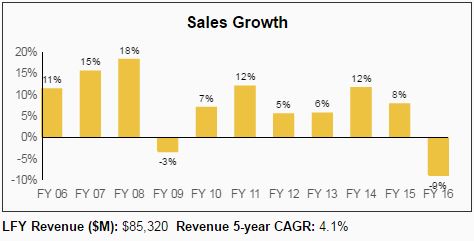

In recent years, Microsoft has struggled with declining sales and stagnant free cash flow.

Source: Simply Safe Dividends

Worse yet, margins and returns on shareholder capital have also deteriorated over the last five years.

So then why is Microsoft’s stock trading at all-time highs?

The answer is that new CEO (since February 2014) Satya Nadella’s “mobile first, cloud first” turnaround is finally starting to bear fruit, with gross margins rising strongly across all of its business units in the past quarter.

Equally important, sales growth has turned positive after declining for five consecutive quarters from late 2015 through 2016.

The company’s improvement is due to two main factors. First, Microsoft has been incredibly successful in winning market share for its Azure cloud services business.

In fact, Azure’s revenues have been about doubling year-over-year in recent quarters.

Meanwhile, Azure Premium recently recorded its 10th consecutive quarter of triple digit (100+%) growth.

Analysts think that Microsoft will be able to achieve massive economies of scale in cloud computing that will eventually allow operating margins to hit at least 30% from this fast-growing cash flow stream.

In fact, on an annualized basis Azure is now bringing in $14 billion per year in recurring, high margin revenue.

Management expects Azure’s recurring revenue to hit $20 billion by 2018 (19.5% annualized growth), which when combined with Microsoft’s other recent successes, should make for solid growth on the company’s top and bottom lines.

Microsoft’s business model is also undergoing a shift from one-time software license sales, such as software preloaded onto PCs, towards a subscription-based revenue stream where users continuously pay on a monthly or annual basis.

While this reduces the initial amount of revenue Microsoft can recognize, the company will likely enjoy a higher customer lifetime value and more stable cash flow as it gains more subscribers.

Since the marginal cost of these products is zero, continued growth in the subscriber base should drive continued improvement in Microsoft’s margins.

Office 365 subscribers (consumer and commercial versions) are growing between 20% and 40% annually in recent quarters, indicating that the future remains bright for this business.

Even Microsoft’s PC-dependent Windows operating system business, which suffers from a secular decline in PCs as the world transitions to mobile computing platforms, is doing relatively well.

For example, in the past year PC OEM sales have stabilized and started growing again at a moderate pace.

Leave A Comment