Over the past year we have regularly contended that a far greater threat to the global economy than either corporate earnings, currency devaluations, rate cuts (or hikes), reserve outflow, or even the stock market, is the sudden, global trade crunch which has been deteriorating rapidly since late 2014 and has seen an even more dramatic drop off as 2015 is winding down. Actually, that is incorrect: global trade is merely a manifestation of the true state of the above listed items.

First, there was ships.

Back in March, we reported that “Global Trade Volume Tumbles Most Since 2011; Biggest Value Plunge Since Lehman.”

Then in August when we first pointed out a dramatic slowdown in the Baltic Dry index which had peaked just a few weeks earlier and we said that “should the dead cat bounce in shipping rates indeed be over, and if the accelerate slide continues at the current pace, not only will shippers mothball key transit lanes, but the biggest concern for global economy, the unprecedented slowdown in world trade volumes, which we flagged a week ago, will be not only confirmed but is likely to unleash yet another global recession.”

Three weeks later, when we first pointed that the BDIY has indeed become a lagging indicator to actual demand, when Reuters reported in its latest weekly update using data from the Shanghai Containerized Freight Index, that key shipping freight rates for transporting containers from ports in Asia to Northern Europe fell by 26.7 percent to $469 per 20-foot container (TEU) in the week ended on Friday.The collapse in rates is nothing short of a bloodbath: “it was the third consecutive week of falling freight rates on the world’s busiest route and rates are now nearly 60 percent lower than three weeks ago.

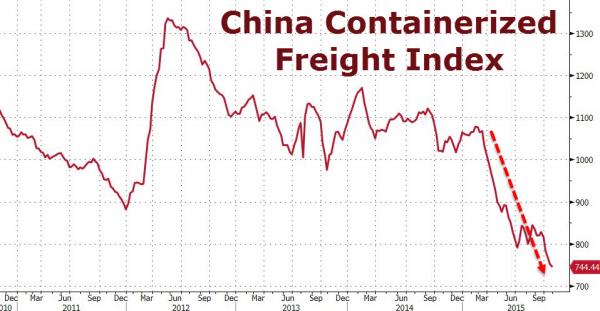

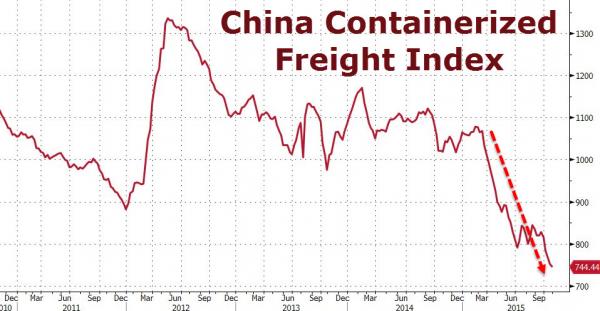

Fast forward to the latest update from the China Containerized Freight Index which as of October 30 has fallen about as far as it ever has in history: at 744.44 it was the lowest on record which suggests that beyond the headline propaganda of some nascent recovery, global trade has literally fallen of a cliff.

And while one could try the usual excuse and blame an excess supply of ships, while ignoring the fact that a third of all containers shipped out of the ports of LA and Long Beach port are now empty…

![]()

… apparently a supply which was “not there” earlier this year when the Index was more than 50% higher, that excuse won’t hold when looking at what is going on inside the US itself.

Related Posts

Business Cycle Indicators As Of End-May

Business Cycle Indicators As Of End-May Broad Market Calibrations: Nowhere Near Good

Broad Market Calibrations: Nowhere Near Good Banks Issue Last Minute Warning About Risks Of Bitcoin Futures, Ask Regulator For Review

Banks Issue Last Minute Warning About Risks Of Bitcoin Futures, Ask Regulator For Review Rolls Royce Plunges On Bombshell Profit Warning, Dividend Review; Faces “Near Death Experience”

Rolls Royce Plunges On Bombshell Profit Warning, Dividend Review; Faces “Near Death Experience”- Wall Street’s Week Ahead: Apple Inc., Facebook, Inc., McDonald’s Corp., Celgene Corporation

Global Outlook Continues Improving

Global Outlook Continues Improving

Leave A Comment