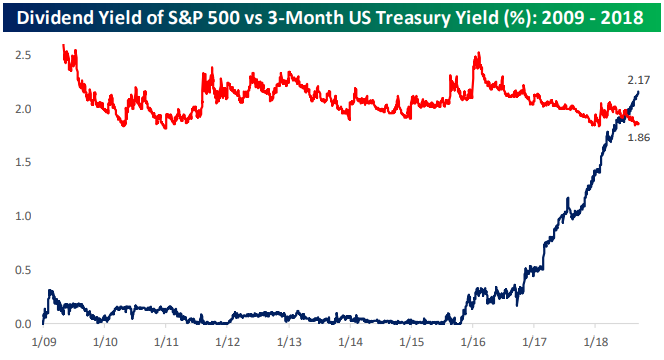

As interest rates have risen in the last year, we have seen a number of charts similar to the one below comparing the yield on the 3-Month US Treasury (UST) to the dividend yield of the S&P 500. For the vast majority of the current bull market (up until only a couple months ago) short-term interest rates have been below the dividend yield of the S&P 500. Since the FOMC began hiking rates over two years ago, short-term UST rates have risen. This year, they rose above the S&P 500 dividend yield; a key inflection point creating a talk that the higher yield on cash makes UST more attractive than equities.

Relative to the current bull market, this may seem impressive. On a longer time horizon, though, this is not the case. Prior to 2009, instances, where short-term Treasuries yielded less than the S&P 500, were few and far between. This cross in yields is by no means a red flag for equities, rather, it is a return to what has been historically normal.

Related Posts

Churchill Downs Incorporated Announces Proposed Offering Of $300 Million Of Senior Notes Due 2028

Churchill Downs Incorporated Announces Proposed Offering Of $300 Million Of Senior Notes Due 2028 Employment: It’s The Trend That Matters

Employment: It’s The Trend That Matters E

Managing VIX-Leveraged ETPs Through Earnings Season, Political Strife And A Frothy Market

E

Managing VIX-Leveraged ETPs Through Earnings Season, Political Strife And A Frothy Market Bitcoin’s Lightning Network is growing, but there are still three major challenges

Bitcoin’s Lightning Network is growing, but there are still three major challenges Qualcomm’s War With Apple Has Been Costly

Qualcomm’s War With Apple Has Been Costly Has Apple Begun A Technical Breakdown?

Has Apple Begun A Technical Breakdown?

Leave A Comment