The Chicago Mercantile Exchange (CME) introduced its Bitcoin (BTC) futures contract in December 2017. This was around the same time that BTC had reached an all-time high of $19,800, but by late 2018 the price had dropped to $3,100. Investors in cryptocurrencies quickly learned that CME derivative contracts allowed them to make bullish bets with leverage, but also enabled them to bet against the price, a practice known as shorting.

Historically, the Securities and Exchange Commission (SEC) has rejected Bitcoin exchange-traded fund (ETF) proposals due to concerns about manipulation on unregulated exchanges. The growing significance of CME’s Bitcoin futures market might address this issue and recently, Hashdex has even requested a Bitcoin ETF that relies on Bitcoin’s physical trades within the CME market.

Professional traders often use BTC derivatives to hedge risks. For instance, one can sell futures contracts while simultaneously buying BTC using borrowed stablecoins using margin. Other examples include selling longer-term BTC futures contracts while purchasing perpetual contracts could help benefit from price discrepancies over time.

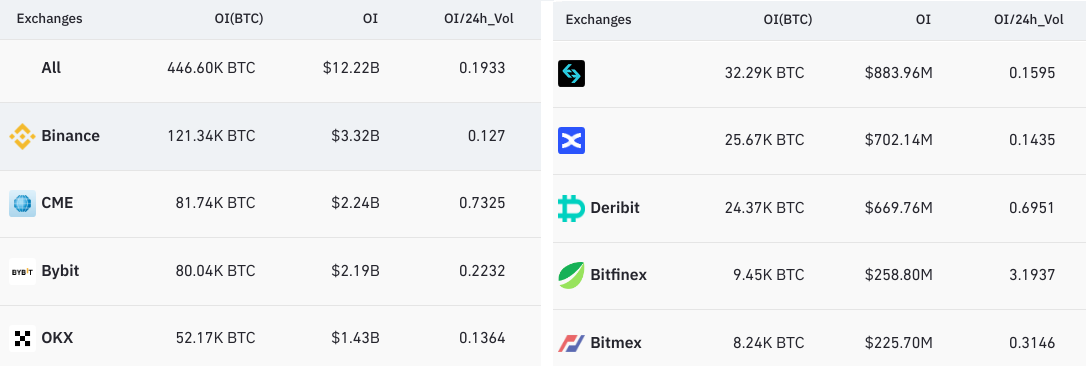

CME overtook Bybit to become the second largest BTC futures market

CME has played a key role in the Bitcoin futures market since 2020, amassing an impressive $5.45 billion open interest by October 2021. However, over the following years, the gap widened as CME’s Bitcoin futures market reached $1.2 billion in January 2023, trailing behind exchanges like Binance, OKX, Bybit and Bitget.

More recently, Bitcoin price dropped by 12.8% between Aug.16 and Aug. 17, leading to a $2.4 billion reduction in the aggregate futures open interest. Notably, CME was the only exchange unaffected in terms of open interest. As a result, CME became the second-largest trading platform on Aug. 17, with a $2.24 billion BTC open interest, according to data from Coinglass.

CME futures show discrepancies relative to crypto exchanges

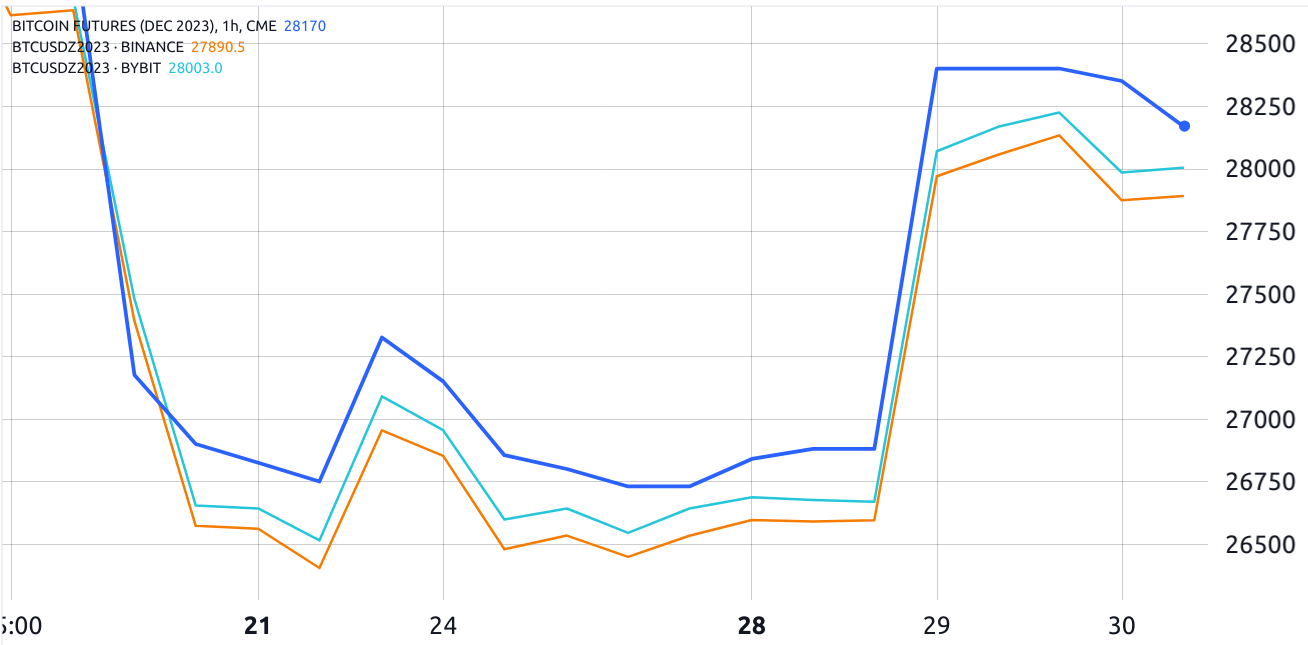

Aside from differences in contract settlement and the absence of perpetual contracts, the trading of Bitcoin futures on CME diverges significantly from most crypto exchanges in terms of both volume and pricing dynamics. The CME records an average daily volume of $1.85 billion, which falls short of its $2.24 billion open interest.

In contrast, Binance’s BTC futures see a daily volume nearing $10 billion, three times greater than its open interest. A comparable pattern is observed at OKX exchange, where daily trading in BTC futures reaches about $4 billion, surpassing its $1.4 billion open interest. This variance can be attributed partially to CME’s higher margin requirement and the fee-free trading environment for market makers on crypto exchanges. Additionally, CME’s trading hours are constrained, with a halt from 4:00 p.m. Central Time to 5:00 p.m., and a full closure on Saturdays.

However, various factors contribute to price distinctions compared to other exchanges. These include shifts in demand for leverage among long and short positions, along with potential disparities in the Bitcoin index price calculation across different providers. Lastly, it’s crucial to consider the solvency risks associated with the tie-up of margin deposits (collateral) until the BTC futures contract settlement.

Related: When will it be too late to invest in Bitcoin?

Given the intricate interplay of variables impacting its pricing and trading dynamics, it fails to provide enhanced price guidance to BTC investors.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Related Posts

China PPI Declines 42nd Consecutive Month; Banks Struggle To Contain Devaluation Fallout; More Capital Controls

China PPI Declines 42nd Consecutive Month; Banks Struggle To Contain Devaluation Fallout; More Capital Controls Tesla Trendline

Tesla Trendline Why The Market Could Soar From Here

Why The Market Could Soar From Here- EC

The Limits Of Monetary Policy In Today’s Fiat Currency World

Half of Asia’s affluent investors have crypto in their portfolio: Report

Half of Asia’s affluent investors have crypto in their portfolio: Report NRG Is Full Of Energy

NRG Is Full Of Energy

Leave A Comment