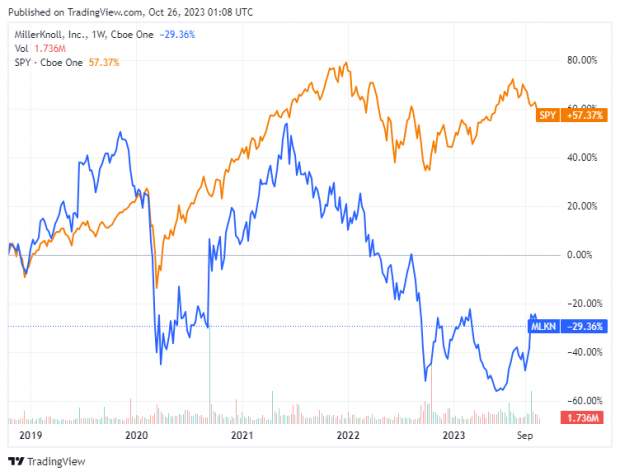

MillerKnoll, Inc. (MLKN) is not expecting a recession in North America as its business improves. This Zacks Rank #1 (Strong Buy) is forecast to grow fiscal 2024 earnings by the double digits.MillerKnoll owns iconic brands in both office and residential furniture including Herman Miller, Knoll, Colebrook Bosson Saunders, Design Within Reach, Edelman, HAY, Maharam, Muuto, NaughtOne, and many others.On the residential furniture side, it operates retail stores globally and sells online. A Big Beat in Fiscal Q1On Sep 26, MillerKnoll reported its fiscal first quarter 2024 results and beat the Zacks Consensus by $0.16, or 76.2%. Earnings were $0.37 versus the consensus of $0.21. It was the third beat in a row.Sales declined 14.9% on a reported basis and 6.9% organically, to $917.7 million. Orders in the quarter were 9.8% lower on a reported basis and 1.3% lower on an organic basis to $913.7 million. The relative decline in organic orders was an improvement compared to the 7.8% year-over-year organic decline posted in the fourth quarter of fiscal 2023.Gross margin improved, however, by 450 basis points year-over-year to 39%. It was mainly driven by the realization of price optimization strategies, moderating input costs and benefit from our ongoing integration efforts.In the Americas Contract segment, net sales were down 8.7% year-over-year on a reported basis and down 1.7% organically to $490.4 million. While new orders were down 4.7% year-over-year on a reported basis and up 2.1% organically to $487.3 million.The growth in organic orders was also a sequential improvement when compared to the prior quarter, which was the fourth quarter of fiscal 2023. MillerKnoll said that month-to-month trends aren’t consistent, but the general trend over the past three quarters has been positive.It remains confident of the improving macro-economic conditions. Additionally, companies continue to shift back to return-to-office practices.The residential side of the business remains challenged, however, due to the weak housing market. Global retail sales were down 26% on a reported basis to $199 million, and down 13.6% organically.”While the specter of economic recession in North America appears to be fading, the housing market remains under pressure,” said Andi Owen, CEO.”Additionally, we are facing difficult macroeconomic conditions in both China and Europe,” she added. Raised Full Year EPS GuidanceThe trend is MillerKnoll’s friend. It raised full year earnings guidance to a range of $1.85 to $2.15. That was above the Zacks Consensus.Not surprisingly, the Zacks Consensus has jumped to $2.07 from $1.80 in the last 30 days. That is earnings growth of 11.9% as the company made $1.85 in fiscal 2023. It is also on the higher end of the new guidance. Shares Turn AroundShares of MillerKnoll have been on quite the ride the last 5 years as they got hit in the pandemic due to work-from-home, rallied on the reopening, and then sold off into 2023.  Image Source: Zacks Investment ResearchBut over the last 6 months, share are up 31.3%.Shares are still cheap, however, on a P/E basis, trading at just 11.1x forward earnings.Given the growth expected, it has a PEG ratio of just 0.9. A PEG under 1.0 usually indicates a company has both growth and value. That’s a rare combination.MillerKnoll generated $130.9 million in free cash flow in the quarter. It repaid $66 million of debt and also repurchased 1.7 million shares for $31.7 million.It also pays a dividend, currently yielding 3.3%.For investors looking for a company that is seeing brighter days ahead for its business, MillerKnoll should be on your short list.More By This Author:Bear of the Day – Winnebago5 Must See Earnings ChartsWatch These 5 Homebuilder Earnings Charts This Week

Image Source: Zacks Investment ResearchBut over the last 6 months, share are up 31.3%.Shares are still cheap, however, on a P/E basis, trading at just 11.1x forward earnings.Given the growth expected, it has a PEG ratio of just 0.9. A PEG under 1.0 usually indicates a company has both growth and value. That’s a rare combination.MillerKnoll generated $130.9 million in free cash flow in the quarter. It repaid $66 million of debt and also repurchased 1.7 million shares for $31.7 million.It also pays a dividend, currently yielding 3.3%.For investors looking for a company that is seeing brighter days ahead for its business, MillerKnoll should be on your short list.More By This Author:Bear of the Day – Winnebago5 Must See Earnings ChartsWatch These 5 Homebuilder Earnings Charts This Week

Related Posts

London Bond Exchange: Bonds Gain Prominence as Premier Investment Option Amid Economic Turmoil

London Bond Exchange: Bonds Gain Prominence as Premier Investment Option Amid Economic Turmoil Pending Home Sales Slump For 5th Straight Month

Pending Home Sales Slump For 5th Straight Month Ahead, Not Behind

Ahead, Not Behind Stocks And Precious Metals Charts – Room At The Top Of The World

Stocks And Precious Metals Charts – Room At The Top Of The World How Nike’s Fundamentals Are Compelling Even In Today’s Bear Markets

How Nike’s Fundamentals Are Compelling Even In Today’s Bear Markets AUDJPY – Double Bottom At 81.00?

AUDJPY – Double Bottom At 81.00?

Leave A Comment