Image Source: PexelsEnd-of-cycle periods come and go, and they all tend to resemble each other. Inflation that exceeds central bank targets legitimises increases in short rates, leading to long rates rising in anticipation. This opens the door to the prospect of different kinds of ‘steepenings’. In this weekly instalment of Simply put, we investigate the current outlook for the yield curve.Need to know:

Image Source: PexelsEnd-of-cycle periods come and go, and they all tend to resemble each other. Inflation that exceeds central bank targets legitimises increases in short rates, leading to long rates rising in anticipation. This opens the door to the prospect of different kinds of ‘steepenings’. In this weekly instalment of Simply put, we investigate the current outlook for the yield curve.Need to know:

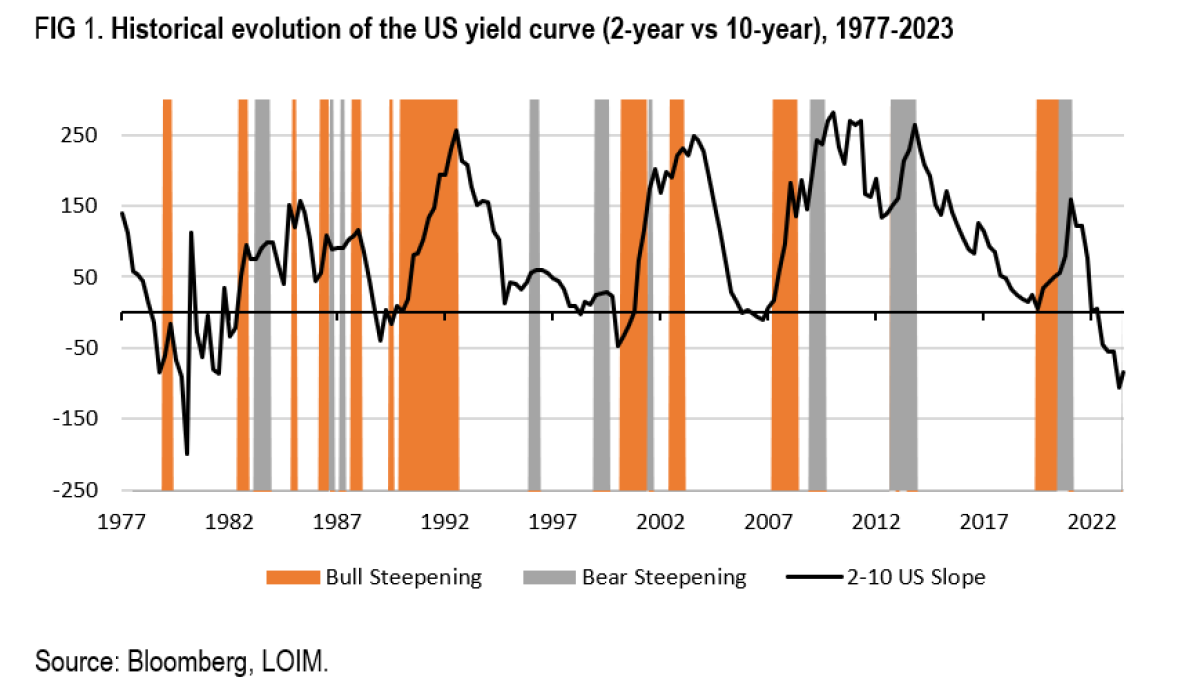

The slope of the curveOnce central-bank rate hikes start to accelerate, the slope of the yield curve turns downward in what is dubbed ‘bear flattening’, as short rates rise faster than long rates. As the cycle peaks, the economy weakens and markets anticipate rate cuts, the curve continues to flatten and invert, entering a period of ‘bull flattening’. Several months into the slowdown, central banks cut rates, surprising the markets and generating a period of ‘bull steepening’. This is a textbook sequence known by bond managers, and history shows it is generally predictable. But not this time.Federal Reserve chair Jerome Powell’s recent Jackson Hole speech made clear that the uncertainty surrounding the economic situation in the United States is pervasive, and the path of the yield curve, and more generally the financial markets, depends on it. Currently, we are witnessing one of the strongest inversions of the curve in 50 years. How will this situation normalise? While we are convinced that a steepening phase is likely to occur, it is important to question its nature – are we looking at a potential ‘bull’ or ‘bear’ steepening? The answer will heavily influence financial assets in the coming months.Bull vs bear: two very different situations.Figure 1 shows the evolution of the US yield curve through the proxy of the spread between 10-year and 2-year rates. When the curve rises, it is steepening. There are two ways this transpires:

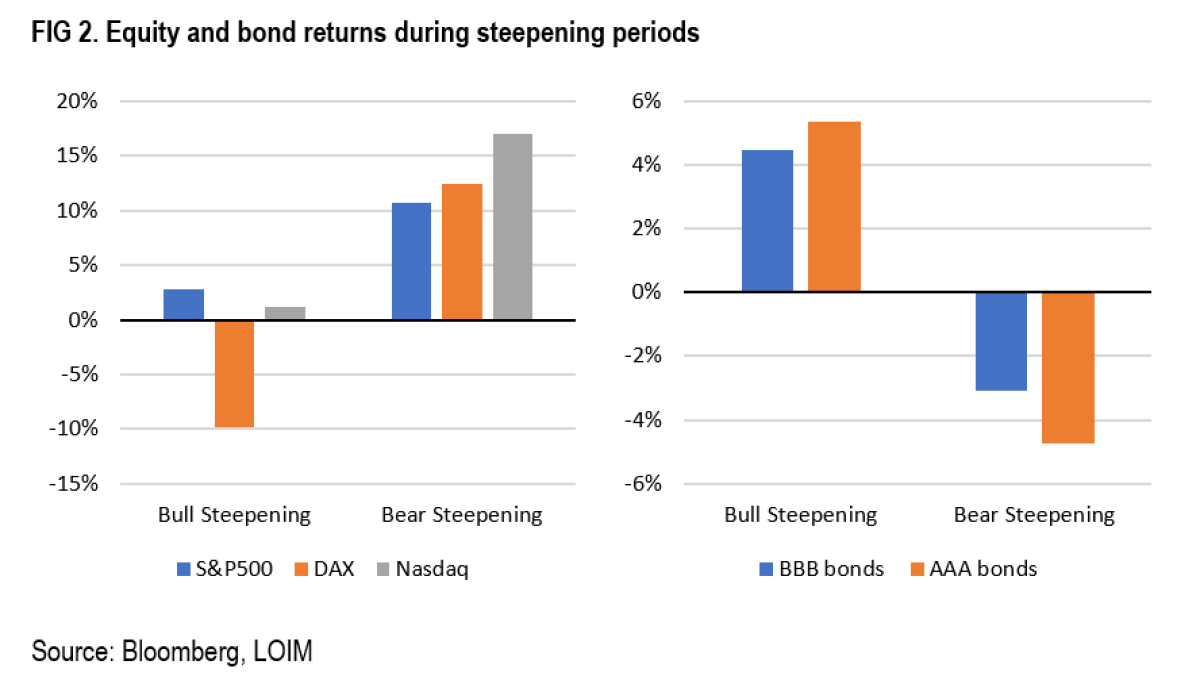

As can be seen from the chart, bull-steepening periods are more common than bear-steepening episodes. The former has occurred 27% of the time in the last 45 years, while the latter took up 22%. Typical bull-steepening periods were: 1990-1992, 2001, 2003, 2008 and 2020, and all were recessionary periods. The bear-steepening stretches were: 1984, 1987, 1996, 1999, 2010, 2013, 2016 and 2021, and, by and large, were marked by unexpected inflation. Notably, the last case of bear steepening was in the post-covid world. Excess stimulus (fiscal and monetary, likely) in reaction to the pandemic was the main driver but also the realization that inflation will be more entrenched going forward. This has all led to a steepening in long-term rates. Equities and bonds: contrasting outlooksAsset-class prospects during each of these periods are also very different, reflecting the underlying economic situation.As shown in Figure 2, periods of bull steepening tend to correspond to periods of economic contraction and, consequently, lower corporate earnings. Equities typically do not fare well during this type of regime, and their performance during these times clearly lags the overall historical average. Historical market performance is uneven and is at best close to 0% (in the case of US equities), if not negative (in the case of European equities, as shown by the DAX index).AAA bonds, on the other hand, generate positive performance in excess of their long-term trend as risk aversion rises. Unsurprisingly, AAA bonds outperform riskier BBB bonds during such periods.Periods of bear steepening, however, are accompanied by stronger equity-market performance, while bond markets lag. Credit spreads tend to contract during such periods and BBB bonds outperform AAA instruments. Such periods are usually characterised by growth in tandem with unexpectedly higher inflation – similar to the situation we currently find ourselves in.So, not all steepening periods are alike, whether in economic or market terms.

Equities and bonds: contrasting outlooksAsset-class prospects during each of these periods are also very different, reflecting the underlying economic situation.As shown in Figure 2, periods of bull steepening tend to correspond to periods of economic contraction and, consequently, lower corporate earnings. Equities typically do not fare well during this type of regime, and their performance during these times clearly lags the overall historical average. Historical market performance is uneven and is at best close to 0% (in the case of US equities), if not negative (in the case of European equities, as shown by the DAX index).AAA bonds, on the other hand, generate positive performance in excess of their long-term trend as risk aversion rises. Unsurprisingly, AAA bonds outperform riskier BBB bonds during such periods.Periods of bear steepening, however, are accompanied by stronger equity-market performance, while bond markets lag. Credit spreads tend to contract during such periods and BBB bonds outperform AAA instruments. Such periods are usually characterised by growth in tandem with unexpectedly higher inflation – similar to the situation we currently find ourselves in.So, not all steepening periods are alike, whether in economic or market terms. Two potentially different bear-steepening scenariosAs bond investors, it seems clear to us that in the current environment, this inversion of the yield curve cannot be sustainable – both from a market and macro perspective. An inverted curve plays against the progression of capital expenditures. A period of recession or, conversely, a period of higher-than-expected inflationary growth will suffice to normalise this situation, presenting an almost win-win situation for steepening buyers. Bust as equity investors, however, it seems appropriate to split the bear-steepening scenario into two sub-scenarios, due to the different forecasts from equity and bond markets on the macro outlook:

Two potentially different bear-steepening scenariosAs bond investors, it seems clear to us that in the current environment, this inversion of the yield curve cannot be sustainable – both from a market and macro perspective. An inverted curve plays against the progression of capital expenditures. A period of recession or, conversely, a period of higher-than-expected inflationary growth will suffice to normalise this situation, presenting an almost win-win situation for steepening buyers. Bust as equity investors, however, it seems appropriate to split the bear-steepening scenario into two sub-scenarios, due to the different forecasts from equity and bond markets on the macro outlook:

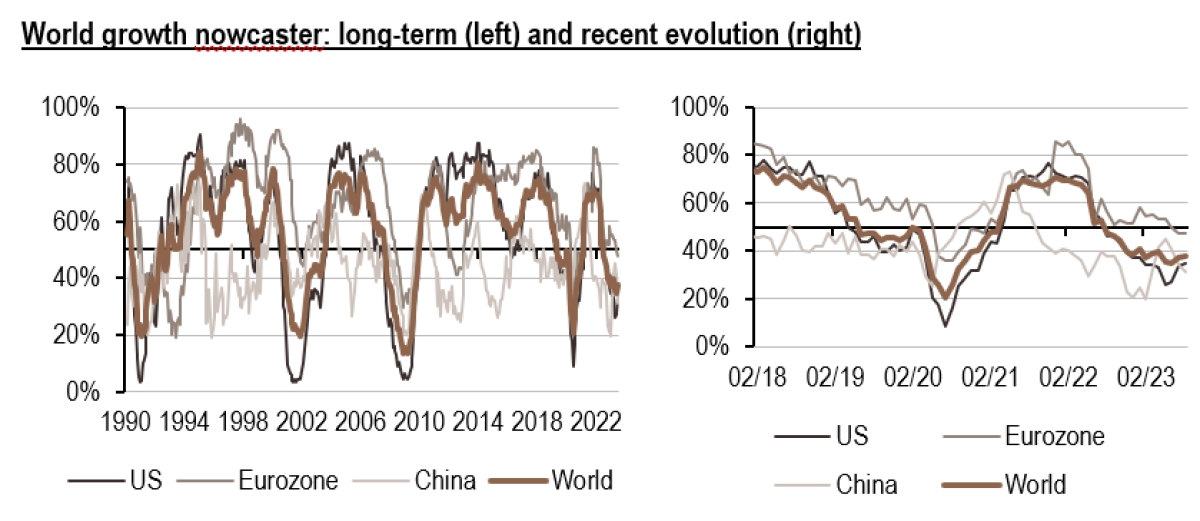

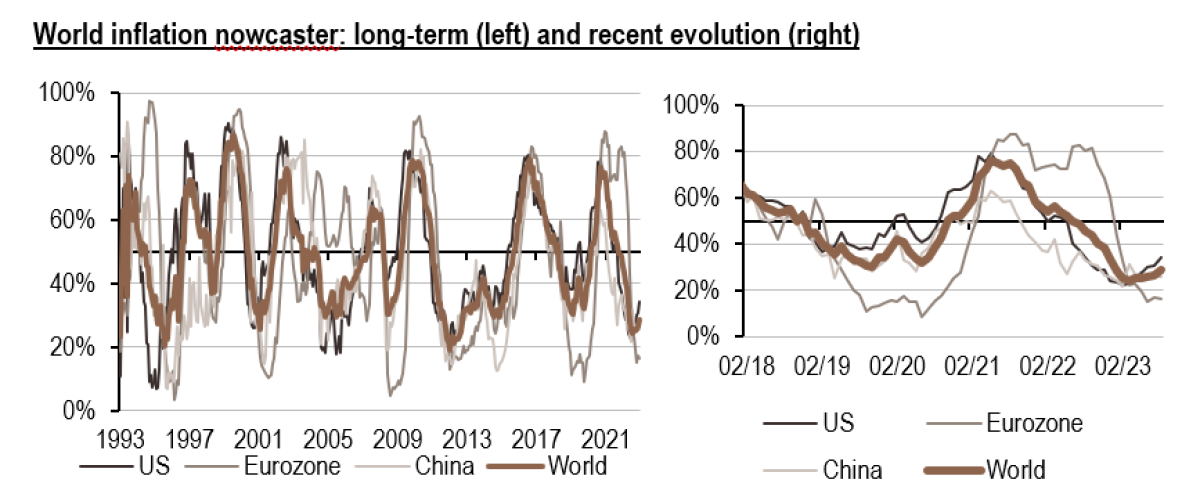

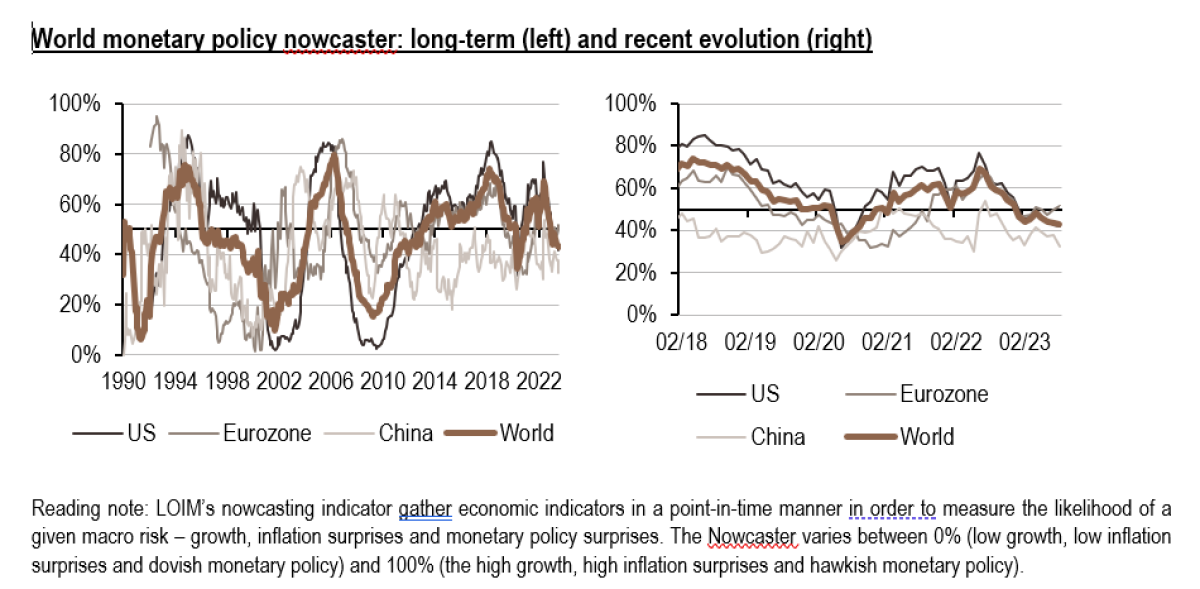

As Powell pointed out, short-term uncertainty dominates here, and that’s the problem. While the steepening of the yield curve seems to us to have largely gained prominence, its modus operandi could make all the difference in terms of the performance of the major asset classes. However, even in the case of a bear-steepening scenario, it’s not certain that equities are destined to rise. Markets need an upturn in earnings prospects if they are to continue to advance.Simply put, the current inversion of the yield curve is unsustainable. What happens next has radically different prospects for equity and bond markets.Nowcasting cornerThis section gathers the most recent evolution of our proprietary nowcasting indicators for world growth, world inflation surprises and world monetary policy surprises. These indicators keep track of the most recent macro evolutions that make markets tick.Our nowcasting indicators currently point to:

About the Authors:Florian Ielpo, PhD, Head of Macro, Multi-Asset Florian is Head of Macro in LOIM’s Multi-Asset Group, where he drives the use of macroeconomic inputs in the group’s investment solutions. He re-joined LOIM in August 2021 after a stint as Head of Macro Research and multi-asset PM at Unigestion. From 2013 to 2015 he was fixed income portfolio manager at LOIM and prior to that at BCV from 2011-2013. From 2008-2010 he was an econometrician within the global bonds team at Pictet AM. He started his career as an economist at Dexia in 2005. Florian is a graduate from ENS and ENSAE in Paris. He holds a PhD in empirical finance from Sorbonne University. Florian publishes regularly scientific articles and books and teaches empirical finance and quantitative portfolio management techniques at HEC Lausanne, Dauphine University, and EM Lyon.

About the Authors:Florian Ielpo, PhD, Head of Macro, Multi-Asset Florian is Head of Macro in LOIM’s Multi-Asset Group, where he drives the use of macroeconomic inputs in the group’s investment solutions. He re-joined LOIM in August 2021 after a stint as Head of Macro Research and multi-asset PM at Unigestion. From 2013 to 2015 he was fixed income portfolio manager at LOIM and prior to that at BCV from 2011-2013. From 2008-2010 he was an econometrician within the global bonds team at Pictet AM. He started his career as an economist at Dexia in 2005. Florian is a graduate from ENS and ENSAE in Paris. He holds a PhD in empirical finance from Sorbonne University. Florian publishes regularly scientific articles and books and teaches empirical finance and quantitative portfolio management techniques at HEC Lausanne, Dauphine University, and EM Lyon. Pascal Menges, Head of Investment process and Equities Research and Client Portfolio Manager for Global Equities (High Conviction and Systematic Strategies)Pascal Menges is head of Investment process and Equities research at Lombard Odier Investment Managers (LOIM). Pascal is also client portfolio manager in Global Equities within LOIM and was successively head of industrial research, hedge fund manager and long-only fund manager. Before joining in May 2006, Pascal was a sell-side analyst at Exane BNP Paribas, covering the European energy sector having held the same position at Oddo Pinatton. He began his career at Elf Aquitaine/ Total. Pascal earned a master’s degree in management from Neoma Business School in France and benefitted from the MBA’s exchange program with the Queensland University of Technology in Australia. He holds the certified international investment analyst (CIIA) designation.

Pascal Menges, Head of Investment process and Equities Research and Client Portfolio Manager for Global Equities (High Conviction and Systematic Strategies)Pascal Menges is head of Investment process and Equities research at Lombard Odier Investment Managers (LOIM). Pascal is also client portfolio manager in Global Equities within LOIM and was successively head of industrial research, hedge fund manager and long-only fund manager. Before joining in May 2006, Pascal was a sell-side analyst at Exane BNP Paribas, covering the European energy sector having held the same position at Oddo Pinatton. He began his career at Elf Aquitaine/ Total. Pascal earned a master’s degree in management from Neoma Business School in France and benefitted from the MBA’s exchange program with the Queensland University of Technology in Australia. He holds the certified international investment analyst (CIIA) designation. Philipp Burckhardt, Credit Analyst / Portfolio Manager, Fixed IncomePhilipp Burckhardt is a credit analyst and portfolio manager within LOIM’s Fixed Income team. He joined in September 2010 within the 2-year graduate program and subsequently stayed within the Fixed Income team. Since 2016 he covers banks and today, additionally, Fixed Income strategy. Philipp earned a master’s degree in quantitative economics and finance (MiQE/F) from the University of St. Gallen (HSG) in 2011. He also holds a bachelor’s degree in economics from the same alma mater. He is a CFA charterholder.

Philipp Burckhardt, Credit Analyst / Portfolio Manager, Fixed IncomePhilipp Burckhardt is a credit analyst and portfolio manager within LOIM’s Fixed Income team. He joined in September 2010 within the 2-year graduate program and subsequently stayed within the Fixed Income team. Since 2016 he covers banks and today, additionally, Fixed Income strategy. Philipp earned a master’s degree in quantitative economics and finance (MiQE/F) from the University of St. Gallen (HSG) in 2011. He also holds a bachelor’s degree in economics from the same alma mater. He is a CFA charterholder. More By This Author:Hedged Equity As A Fixed Income Replacement Was 60/40 A Big Head Fake?The Short On Shorting Bonds

More By This Author:Hedged Equity As A Fixed Income Replacement Was 60/40 A Big Head Fake?The Short On Shorting Bonds

Related Posts

Hot Options Report For End Of Day – Wednesday, Dec. 6

Hot Options Report For End Of Day – Wednesday, Dec. 6 Galaxy Digital terminates BitGo acquisition, citing breach of contract

Galaxy Digital terminates BitGo acquisition, citing breach of contract Inflation Risk Spooks Equity Markets

Inflation Risk Spooks Equity Markets- Urban Outfitters Stock Falling Over 7% On Q3 Sales Miss

Global Blood Therapeutics Announces Proposed Public Offering Of Common Stock

Global Blood Therapeutics Announces Proposed Public Offering Of Common Stock- 3 Best Franklin Templeton Mutual Funds To Buy Now

Leave A Comment