This morning the National Association of Realtors released the February data for their Pending Home Sales Index. Here is an excerpt from the latest press release:

Lawrence Yun, NAR chief economist, says the housing market has gotten off to an uneven start so far in 2018. “Contract signings rebounded in most areas in February, but the gains were not large enough to keep up with last February’s level, which was the second highest in over a decade (112.1)1,” he said. “The expanding economy and healthy job market are generating sizeable homebuyer demand, but the miniscule number of listings on the market and its adverse effect on affordability are squeezing buyers and suppressing overall activity.”

Added Yun, “Expect ongoing volatility in the Northeast region at least through March. Although pending sales there bounced back in February following January’s cold weather-related decline, the multiple winter storms over these last few weeks likely put a chill on contract signings once again this month.” (more here).

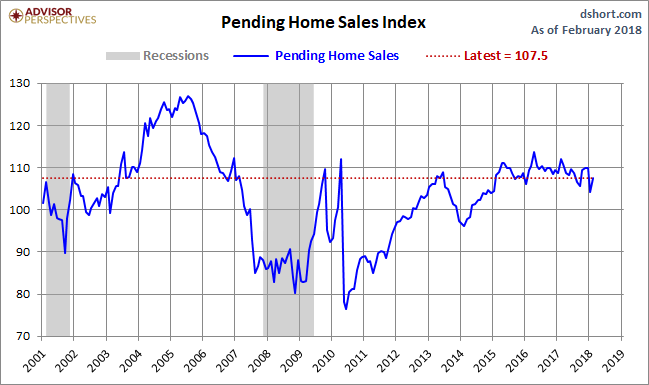

The chart below gives us a snapshot of the index since 2001. The MoM came in at 3.1%, up from a 5.0% decline last month. Investing.com had a forecast of 2.1%.

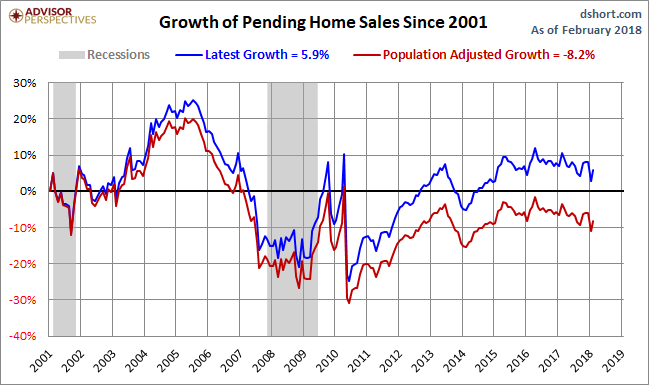

Over this time frame, the US population has grown by 15.3%. For a better look at the underlying trend, here is an overlay with the nominal index and the population-adjusted variant. The focus is pending home sales growth since 2001.

The index for the most recent month is 15% below its all-time high in 2005. The population-adjusted index is 24% off its 2005 high.

Pending versus Existing Home Sales

The NAR explains that “because a home goes under contract a month or two before it is sold, the Pending Home Sales Index generally leads Existing Home Sales by a month or two.” Here is a growth overlay of the two series. The general correlation, as expected, is close. And a close look at the numbers supports the NAR’s assessment that their pending sales series is a leading index.

Related Posts

MicroStrategy purchases $82M in Bitcoin, now holds 122,478 coins

MicroStrategy purchases $82M in Bitcoin, now holds 122,478 coins- Indonesian regulator takes cue from Islamic NGOs, bars crypto sales for institutions

Equity And Investing Trading Strategies (Equity Trading Strategies)

Equity And Investing Trading Strategies (Equity Trading Strategies) Corporate Repackaging

Corporate Repackaging- Economic Data And Forecasts For The Weeks Of July 10 And July 17

- How Quickly Should You Invest The Money You Inherit?

Leave A Comment