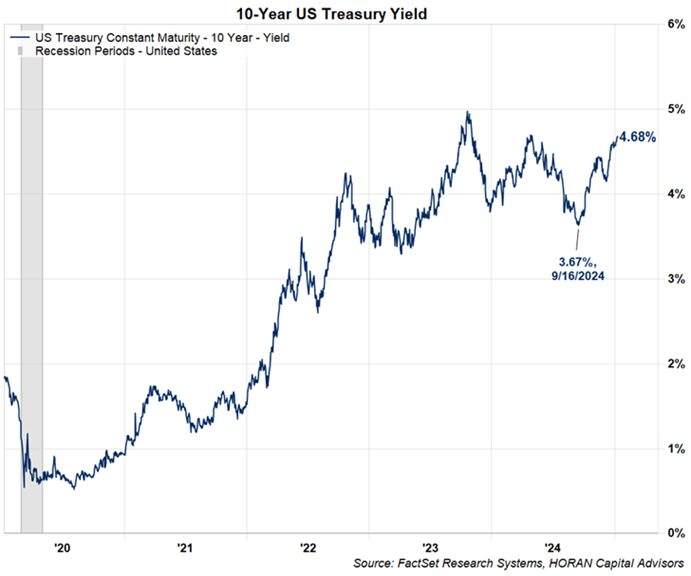

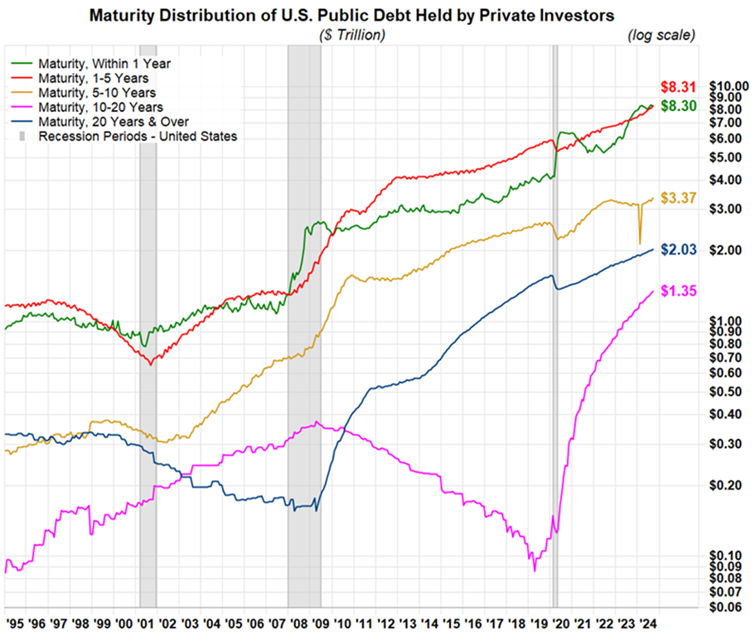

Just as the Fed began reducing the Fed Funds rate in September last year, longer term interest rates as measured by the 10-Year U.S. Treasury began moving higher. In mid-September the 10-year U.S. treasury yield equaled 3.61% and has now reached 4.68%. Commensurate with an increase in yields bond prices fall since a bond’s price moves in the opposite direction of the move in interest rates.  Higher bond rates impact the attractiveness of other asset classes and tend to be a headwind for stocks for a number of reasons. With higher interest rates bond investments become more attractive to investors thus leading to bonds becoming competition for stocks. Also, interest rates are used in some methods of valuing stocks with the interest rate used in discounting a company’s future earnings to a present value. Higher rates result in the present value of earnings being lower compared to using a lower interest rate to discount the earnings; thus, pushing a company’s valuation multiple. i.e., price to earnings ratio, higher. So, what is behind the move higher in longer term interest rates?One cause cited for the rise in longer term interest rates is the return of the so-called ‘bond vigilantes.’ A recent PIMCO article describes these vigilantes as,“Investors who discipline excessive government spending by demanding higher sovereign debt yields. Since the 1980s, when strategist Ed Yardeni coined the term, episodes of fiscal excess regularly give rise to questions about when these vigilantes might turn up.Predicting sudden market responses to long-term trends is difficult. There is no organized group of vigilantes poised to act at a specific debt threshold; shifts in investor behavior typically occur at the margin and over time. Therefore, if you’re seeking clues about the potential for bond vigilantism, you might start by asking the largest fixed income investors – who theoretically hold the most market sway – what they’re doing.At PIMCO, we are already making incremental adjustments in response to rising U.S. deficits. Specifically, we’re less inclined to lend to the U.S. government at the long end of the yield curve, favoring opportunities elsewhere.With the bond vigilantes focus on excessive spending by governments, it is safe to say the U.S. government’s large deficit spending of nearly $2 trillion makes it a focus of the bond vigilantes. This deficit must be financed by bond investors and the recent rate rise may be an indication large bond investors do not want to lock up investment funds in long term bonds. Also at play is the fact the U.S. government has nearly 70% of its bonds maturing in five years or less as seen with the red and green lines on the below chart. Certainly, maturing bond investors can rollover their investments into the newly issued bonds, but the interest rate on the new bonds is likely to be higher leading to the need to issue even more government bonds.

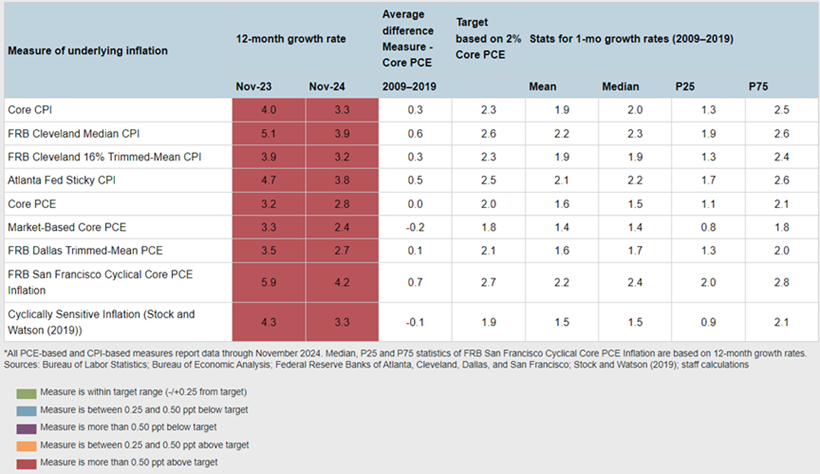

Higher bond rates impact the attractiveness of other asset classes and tend to be a headwind for stocks for a number of reasons. With higher interest rates bond investments become more attractive to investors thus leading to bonds becoming competition for stocks. Also, interest rates are used in some methods of valuing stocks with the interest rate used in discounting a company’s future earnings to a present value. Higher rates result in the present value of earnings being lower compared to using a lower interest rate to discount the earnings; thus, pushing a company’s valuation multiple. i.e., price to earnings ratio, higher. So, what is behind the move higher in longer term interest rates?One cause cited for the rise in longer term interest rates is the return of the so-called ‘bond vigilantes.’ A recent PIMCO article describes these vigilantes as,“Investors who discipline excessive government spending by demanding higher sovereign debt yields. Since the 1980s, when strategist Ed Yardeni coined the term, episodes of fiscal excess regularly give rise to questions about when these vigilantes might turn up.Predicting sudden market responses to long-term trends is difficult. There is no organized group of vigilantes poised to act at a specific debt threshold; shifts in investor behavior typically occur at the margin and over time. Therefore, if you’re seeking clues about the potential for bond vigilantism, you might start by asking the largest fixed income investors – who theoretically hold the most market sway – what they’re doing.At PIMCO, we are already making incremental adjustments in response to rising U.S. deficits. Specifically, we’re less inclined to lend to the U.S. government at the long end of the yield curve, favoring opportunities elsewhere.With the bond vigilantes focus on excessive spending by governments, it is safe to say the U.S. government’s large deficit spending of nearly $2 trillion makes it a focus of the bond vigilantes. This deficit must be financed by bond investors and the recent rate rise may be an indication large bond investors do not want to lock up investment funds in long term bonds. Also at play is the fact the U.S. government has nearly 70% of its bonds maturing in five years or less as seen with the red and green lines on the below chart. Certainly, maturing bond investors can rollover their investments into the newly issued bonds, but the interest rate on the new bonds is likely to be higher leading to the need to issue even more government bonds. Another variable impacting bond yields is the fact inflation is not entirely under control or may not be under control. In the release of the Fed’s minutes from its December meeting several Fed members noted there seemed to be “momentum” in economic data that might put upward pressure on inflation. Also, the committee cited potential inflation concerns around policies put forth by the incoming administration in Washington.The Atlanta Fed released Personal Consumption Expenditures inflation data in December and noted, “while there is a broad-based slowing among some of the near-term measures of underlying PCE inflation, all the year-over-year measures…are still elevated relative to the FOMC’s price stability mandate.” Included with the commentary was the below table showing all the measures in the table that are evaluated by the Fed are more than 50 basis points above their target.

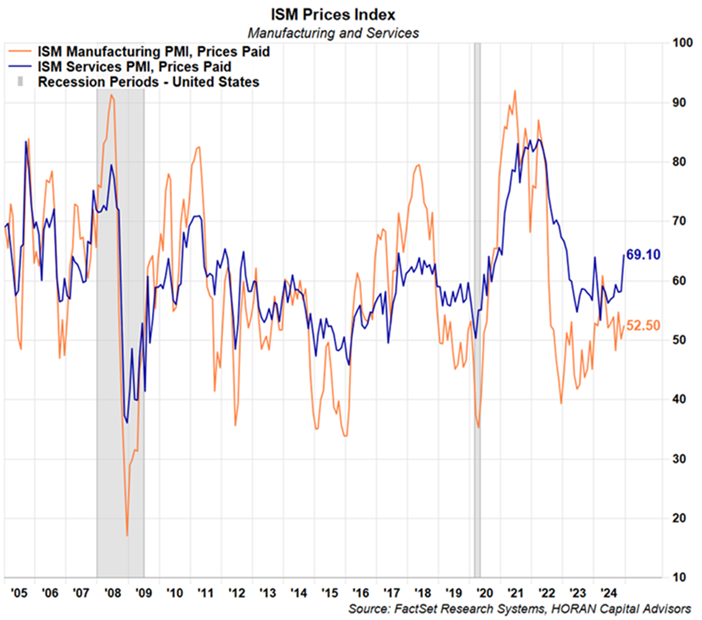

Another variable impacting bond yields is the fact inflation is not entirely under control or may not be under control. In the release of the Fed’s minutes from its December meeting several Fed members noted there seemed to be “momentum” in economic data that might put upward pressure on inflation. Also, the committee cited potential inflation concerns around policies put forth by the incoming administration in Washington.The Atlanta Fed released Personal Consumption Expenditures inflation data in December and noted, “while there is a broad-based slowing among some of the near-term measures of underlying PCE inflation, all the year-over-year measures…are still elevated relative to the FOMC’s price stability mandate.” Included with the commentary was the below table showing all the measures in the table that are evaluated by the Fed are more than 50 basis points above their target. And lastly, in evaluating prices at the manufacturing and service level of the economy, purchasing managers that are surveyed by the Institute for Supply Management (ISM) are indicating they are seeing a trend in higher prices paid on their inputs as seen in the below chart. These higher prices ultimately are passed onto the consumer, leading to potentially higher inflation.

And lastly, in evaluating prices at the manufacturing and service level of the economy, purchasing managers that are surveyed by the Institute for Supply Management (ISM) are indicating they are seeing a trend in higher prices paid on their inputs as seen in the below chart. These higher prices ultimately are passed onto the consumer, leading to potentially higher inflation. In conclusion, the Friday (1/10/25) report on nonfarm payrolls will provide insight into the health of the labor market. Wednesday’s data on jobless claims, initial claims and the ADP Employment Survey provided mixed information but leaned somewhat healthy with a below consensus level of initial claims filed. By a small amount, the economic data is coming in better than expected so possibly the higher bond rates are more to do with a strengthening economy than the so-called bond vigilantes. Nonetheless, near term data that impacts bond prices will have investors’ attention as bond volatility can lead to equity market volatility as well.More By This Author:Not A Year For The 2024 Dogs Of The Dow

In conclusion, the Friday (1/10/25) report on nonfarm payrolls will provide insight into the health of the labor market. Wednesday’s data on jobless claims, initial claims and the ADP Employment Survey provided mixed information but leaned somewhat healthy with a below consensus level of initial claims filed. By a small amount, the economic data is coming in better than expected so possibly the higher bond rates are more to do with a strengthening economy than the so-called bond vigilantes. Nonetheless, near term data that impacts bond prices will have investors’ attention as bond volatility can lead to equity market volatility as well.More By This Author:Not A Year For The 2024 Dogs Of The Dow

A Bullish Narrative For Stocks

Bullish Investor Sentiment Might Be Bearish For Stocks

Related Posts

EUR/GBP Forecast: Testing Support

EUR/GBP Forecast: Testing Support Dollar Drops And Stocks Surge As Yellen Echoes The ’Fed Put’

Dollar Drops And Stocks Surge As Yellen Echoes The ’Fed Put’ September Gas Expires With A Bang

September Gas Expires With A Bang- Weekly Fundamental Forecast: The Week Ends With Raised Trade War Threats Fom Trump, ECB And BoE Rate Decisions Ahead

Think Ahead: US Inflation And CEE Data In Focus

Think Ahead: US Inflation And CEE Data In Focus Gold At The Verge Of A Breakdown As 2018 Kicks Off

Gold At The Verge Of A Breakdown As 2018 Kicks Off

Leave A Comment