Oil price is recoiling this month after ending a five-month streak of gains in February. This is especially true, as some positive sentiments have again started to build up in the oil market, which were under pressure from growing U.S. crude production.

In fact, oil price climbed more than 2% in the last trading session buoyed by tensions in the Middle East and the possibility of further falls in Venezuelan output. A meeting between the Saudi crown prince Mohammed bin Salman and U.S. President Donald Trump early this week has raised speculation that the United States could re-impose sanctions on Iran following renewed criticism of the 2015 nuclear deal. The energy consultancy FGE expects the move to likely result in 250,000-500,000 barrels per day drop in its exports by this yearend.

Falling production in Venezuela, where output has been halved since 2005 to below 2 million barrels per day due to an economic crisis, will continue to support to oil price. Additionally, a weak dollar has made dollar-denominated crude cheap for foreign investors, potentially spurring demand.

Further, the historic output cut deal, wherein OPEC, Russia and other producers have agreed to curb production is now paying off with the global oil market on its way toward balancing. Moreover, the oil market is currently in a state of backwardation, where later-dated contracts are cheaper than near-term contracts, for months. This signals that the oil market is tightening and demand is robust, paving the way for an oil rally. This trend is likely to persist at least in the near term, acting as the biggest catalyst for the commodity.

However, surging U.S. crude production, which has risen by more than a fifth since mid-2016, to 10.38 million barrels per day, has been disrupting the oil demand/supply imbalance. While global demand is expected to pick up quickly this year, supply is also growing at a faster pace leading to a rise in inventories in the first quarter of 2018, per the International Energy Agency (IEA).

Related Posts

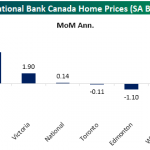

Canadian Home Prices Get Used To A Slower Roll

Canadian Home Prices Get Used To A Slower Roll What’s Making Stocks Great Again?

What’s Making Stocks Great Again? JPMorgan Sees $24 As Ceiling Not Floor For GE Shares

JPMorgan Sees $24 As Ceiling Not Floor For GE Shares Expect some crypto companies to fail in the wake of Bitcoin’s halving

Expect some crypto companies to fail in the wake of Bitcoin’s halving Ripple’s Explosive Surge Accelerates; Market Cap Crosses Half Of Bitcoin’s

Ripple’s Explosive Surge Accelerates; Market Cap Crosses Half Of Bitcoin’s Norwegian billionaire ditches skepticism, invests in local crypto exchange

Norwegian billionaire ditches skepticism, invests in local crypto exchange

Leave A Comment