The Federal Reserve’s unwinding program started in October. What does it mean for the gold market?

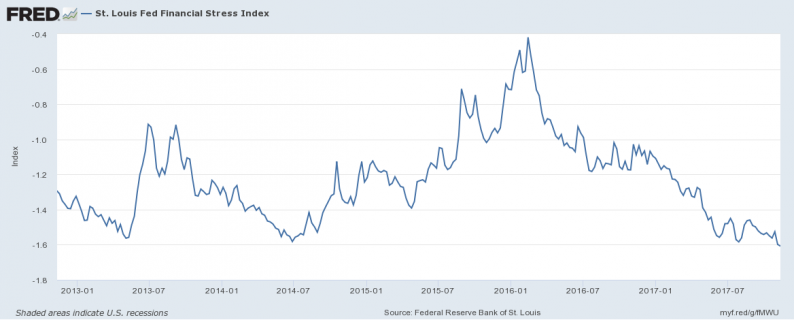

Last month, the U.S. central bank began reducing its massive balance sheet. Many analysts and investors worried that the so-called reverse quantitative easing would disrupt financial markets. The logic behind these concerns was simple: as quantitative easing supported asset prices, its reversal would upset the markets. However, we have not seen any signs of significant turmoil. Surely, the VIX and credit spreads increased somewhat in the first half of November, but financial stress in the markets hit another record low, as one can see in the chart below. Generally speaking, the Fed is tightening its monetary policy, but financial conditions do not follow.

Chart 1: St. Louis Fed Financial Stress Index over the last five years.

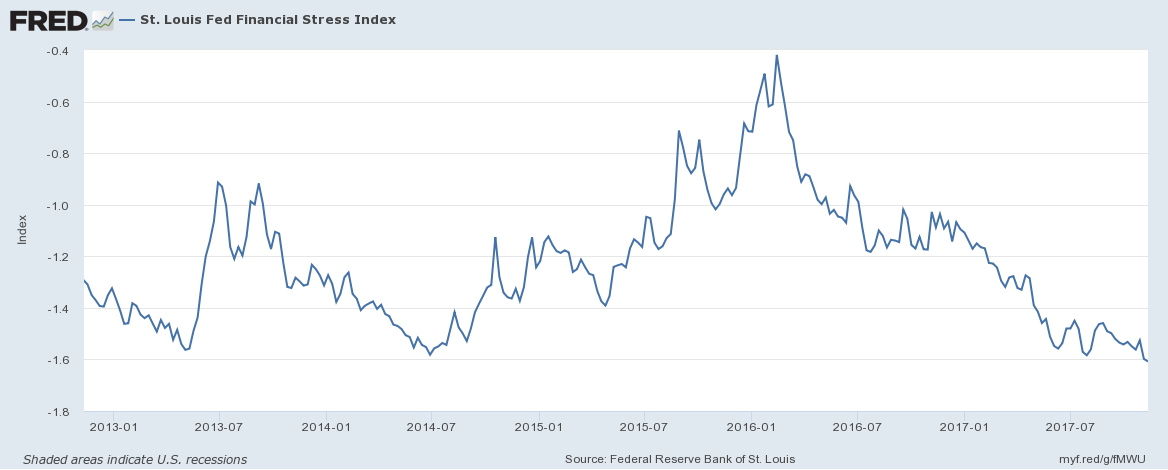

Why have financial markets and gold shrugged off the Fed’s unwinding of its balance sheet? We will analyze this issue in detail in the December edition of the Market Overview. Here, we would like to point out an interesting thing. As the next chart shows, the U.S. central bank’s assets practically did not change at all in October! And there was an increase in the first half of the month, actually!

Chart 2: Fed’s balance sheet from January to November 2017.

Hence, it is now understandable that neither the stock market nor the precious metals market experienced turbulences – the unwinding has not yet started at all! Will that change in the future? In December we will thoroughly discuss why gold bulls should not count on the Fed’s unwind as a potentially bullish factor. If there is any significant impact – and we are skeptical about that – it will rather be bearish.

Related Posts

Gold Prices Rise On News Of Russia – North Korea Defense Deal

Gold Prices Rise On News Of Russia – North Korea Defense Deal Sony predicts $3.2bn loss

Sony predicts $3.2bn loss PMs Join The Party – Silver Spikes As Gold Jumps Above $1100

PMs Join The Party – Silver Spikes As Gold Jumps Above $1100 Aerovironment, Inc. Shares Shoot Up On Better Than Expected Earnings

Aerovironment, Inc. Shares Shoot Up On Better Than Expected Earnings HARTi and Mitsui Sumitomo roll out NFT insurance coverage for claims

HARTi and Mitsui Sumitomo roll out NFT insurance coverage for claims Chart Of The Day: PowerShares QQQ Trust

Chart Of The Day: PowerShares QQQ Trust

Leave A Comment