The threat of a global trade war is a risk factor for the global economic outlook, warned the managing director of the International Monetary Fund on Thursday. But in the weeks since President Trump rolled out tariffs on Chinese imports – and China responded in kind – nothing much has changed in the hard data as it relates to the US macro trend.

The probability that a new recession is near for the US remains virtually nil. That could change, of course, if trade restrictions expand beyond the relatively minimal tariffs announced so far. At the moment, however, a downturn triggered by a trade war appears to be a low-probability event, based on the numbers published to date.

By contrast, headwinds tied to growth may be a bigger threat in the months ahead. With the US economic expansion in its ninth year, the Federal Reserve remains on track to push interest rates higher. It remains to be seen if a tighter monetary policy will choke off growth, but the case is still solid for expecting output to rise in the foreseeable future.

Next week’s preliminary estimate of first-quarter GDP growth, however, is set to decelerate to 2.1%, according to this month’s survey of economists via The Wall Street Journal. That’s well below the 2.9% gain in the previous quarter.

Growth may be on track to downshift, but the projections published to date are still strong enough to keep the economy from falling off the business-cycle cliff. Meanwhile, the Capital Spectator’s estimate of recession risk for the US equates with a near-zero chance that a new downturn started last month, based on a diversified set of economic indicators. (For a more comprehensive review of the macro trend on a weekly basis, see The US Business Cycle Risk Report.)

The upbeat profile implies that Monday’s release of the Chicago Fed National Activity Index for March will confirm that recession risk remained low last month.

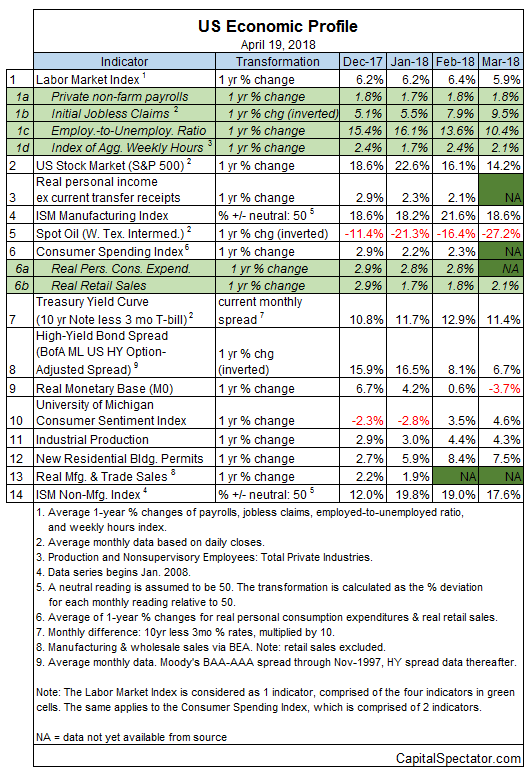

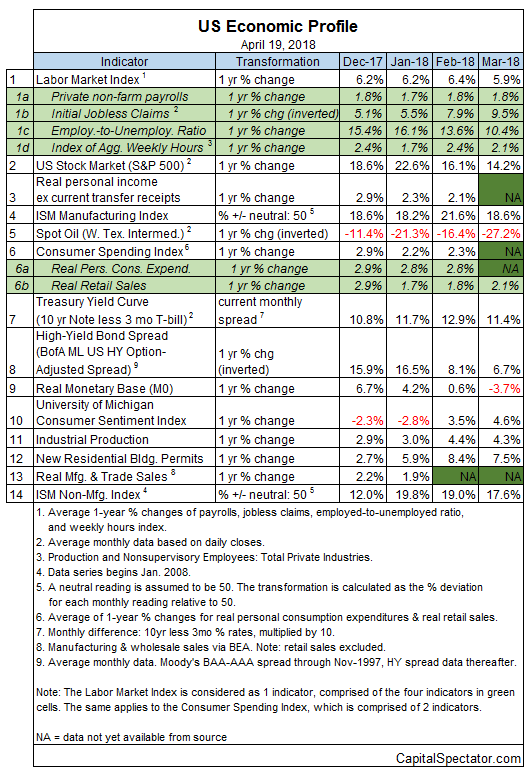

Aggregating the data in the table above translates into a strong positive trend overall. The Economic Trend and Momentum indices (ETI and EMI, respectively) remain well above their respective danger zones (50% for ETI and 0% for EMI). When/if the indexes fall below those tipping points, the declines will mark clear warning signs that recession risk is elevated and a new downturn is imminent. The analysis is based on a methodology that’s profiled in my book on monitoring the business cycle.

Leave A Comment