Tuesday, May 17

Wednesday, May 18

Thursday, May 19

Friday, May 20

Home Depot (HD)

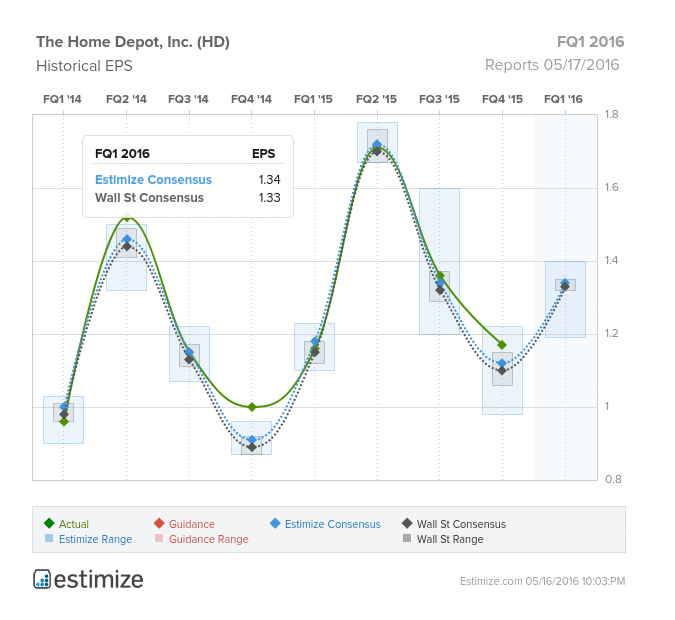

Consumer Discretionary – Specialty Retail | Reports May 17, before the open.

The Estimize consensus is calling for earnings per share of $1.34 on $22.14 billion in revenue, 1 cent higher than Wall Street on the bottom line and $54 million on the top. Compared to a year earlier, this reflects a 16% increase in earnings while sales could climb as much as 6%. Typically the stock does well during earnings season which is icing on the cake for shareholders that have seen shares increase 20% in the past 12 months.

What to Watch: Home Depot is on an upward trajectory as of late and after strong fourth quarter earnings, expectations are high coming into Q1 results. The company issued strong guidance for 2016 with sales expected to be up as much as 6% and comp sales increasing approximately 4.5%, leading to an uptrend in estimates. Home Depot’s increased focus on omni channel capabilities and merchandise tools coupled with a persistent housing recovery has started to pay off. The company has implemented significant changes in its store operations to make them simpler and more customer friendly. Furthermore, Home Depot has expanded its omnichannel capabilities in response to the evolving retail environment. Online sales last quarter grew 23% to nearly $1.25 billion. Nearly 40% of online orders are picked up from stores which creates store sales. To top it all off, Home Depot maintains a strong balance sheet, allowing them to issue generous dividend payments.

Salesforce (CRM)

Information Technology – Software | Reports May 18, after the close.

The Estimize consensus is calling for a profit of 24 cents per share on $1.9 billion in revenue, 1 cent higher than Wall Street on the bottom line and $4 million on the top. Compared to a year earlier this reflects 49% growth in profits and 25% in sales. This is a name that is seeing upward revisions into its report, with EPS expectations increasing 9% since the Q4 report. In this rapidly changing tech environment, strong earnings are simply not enough to push share prices. Despite a 22% gain in the past 3 months, the stock is still slightly down year to date.

What to watch: By any measure, Salesforce is firing on all cylinders heading into its first quarter report. The leader in CRM software has continually reported double digit gains in both revenue and profit. Strong growth has been fueled by key partnerships with big tech names such as Microsoft, organic sales growth in its cloud based services, and the acquisition of smaller competitors which have been successfully integrated into their own suite. Higher demand for marketing and analytics tools, part of its new lightning platform, presents a new opportunity to sustain rapidly expanding growth rates.

Leave A Comment