Written by Bryan Perry

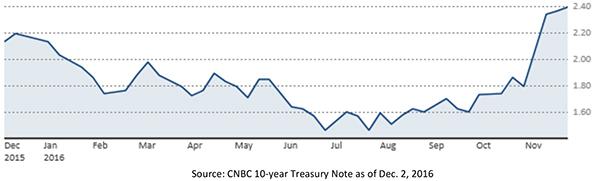

…Some very high-profile market gurus – namely DoubleLine’s Jeff Gundlach and legendary value hedge fund manager Stanley Druckenmiller – are predicting 10-year Treasury yields will rise to 6% by 2018 and GDP growth will reach the same 6% rate by 2019. Anticipation of those numbers could take the 10-year Treasury Note yield above 3% fairly soon, in anticipation of further Fed tightening.

Investors are having to rapidly adjust to this incredible turn of events in an almost overnight fashion that is very unsettling for those holding tight to their long-dated bond holdings. The only solace is that all bonds mature at par value – if you elect to hold on to long-dated maturities. Either way, the great bond rally of the past eight years is officially over – at least until the next recession comes around.

It would seem that both Gundlach and Druckenmiller are getting some early tailwinds for their forecasts. U.S. Treasuries took their cue from the economic calendar as positive news translates to a downhill slope for bond prices.

The hits keep on coming:

Related Posts

AskSlim Market Week – Friday, February 3

AskSlim Market Week – Friday, February 3 Dollar May Prove Resilient If It Is Turn Around Tuesday

Dollar May Prove Resilient If It Is Turn Around Tuesday BIS Points Finger At Yellen, Draghi: Warns About “Unthinkably” Low Interest Rates, Bond Market “Dislocations”

BIS Points Finger At Yellen, Draghi: Warns About “Unthinkably” Low Interest Rates, Bond Market “Dislocations”- 5 Dividend Stocks That Warrant Growth Amid Volatility

- E

Does Donald Trump Want A Financial Depression?

Great Graphic: Gas And Oil

Great Graphic: Gas And Oil

Leave A Comment