Following years of acrimony between OPEC and the hedge fund community, which the cartel dismissed simply as “speculators”, things suddenly changed in 2016 when the two groups got so close, there were outright reports of collusion between the two on various occasions. We documented this last month in “Why OPEC Is Colluding With Hedge Funds.” However, as Reuters’ energy analyst John Kemp pointed out on twitter this morning, that relationship may be ending as hedge funds start to lose confidence in OPEC.

Taking us to the beginning, Kemp notes that OPEC and some of the most important hedge funds active in commodities reached an understanding on oil market rebalancing during informal briefings held in the second half of 2016. OPEC committed to implement credible production cuts and reduce global crude stocks while hedge funds responded by establishing bullish long positions in both flat prices and calendar spreads.

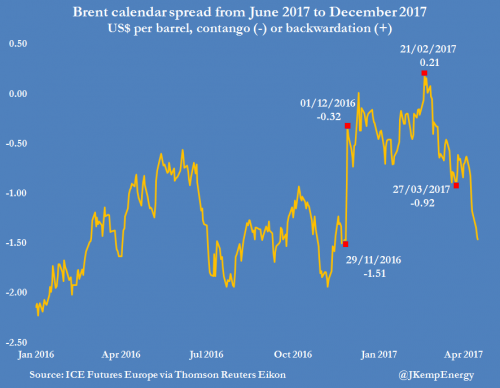

OPEC effectively underwrote the fund managers’ bullish positions by providing the oil market with detail about output levels and public messaging about high levels of compliance. In return, the funds delivered an early payoff for OPEC through higher oil prices and a shift from contango to backwardation that should have helped drain excess crude stocks.

The Reuters analyst then notes that the understanding was initially successful between December 2016 and February 2017, with reports of strong compliance from OPEC, spot prices rising $10 per barrel and calendar spreads moving from contango to flat or, albeit briefly, backwardation.

But the understanding started to unravel with the calendar spreads collapsing after Feb. 21 and flat prices dropping from March 8.

The sharp reversal in both spreads and flat prices inflicted substantial losses on many bullish hedge funds in February and March. The correction came amid growing doubts about whether OPEC was really cutting oil supplies to the market by as much as anticipated.

Leave A Comment