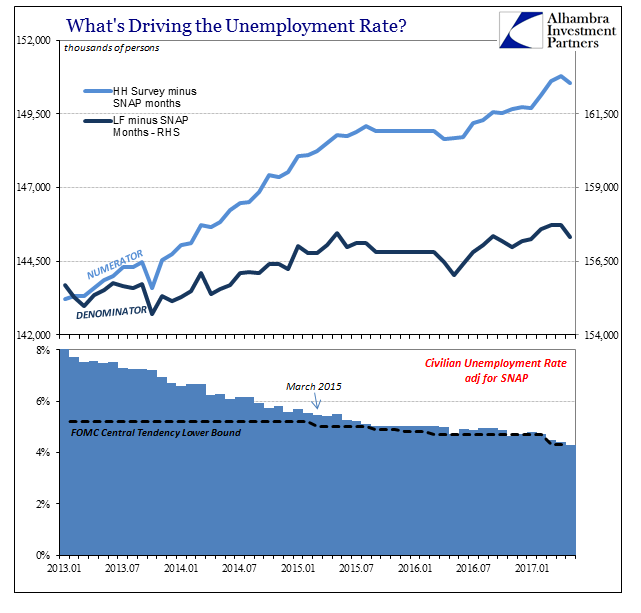

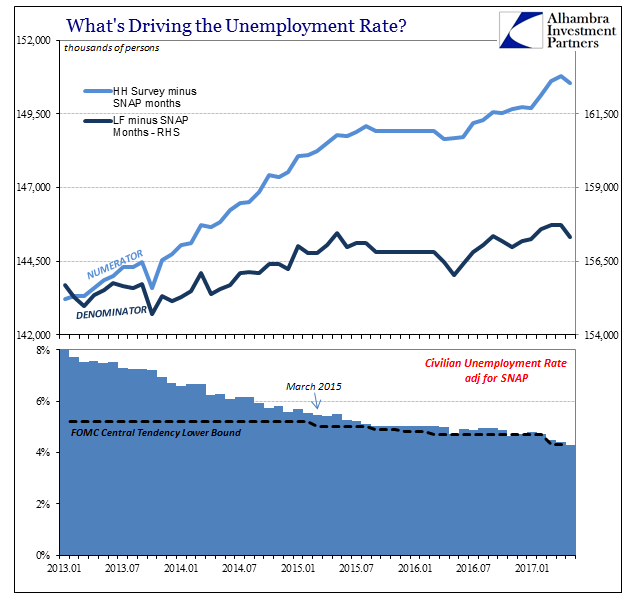

The irony of the unemployment rate for the Federal Reserve is that the lower it gets now the bigger the problem it is for officials. It has been up to this year their sole source of economic comfort. Throughout 2015, the Establishment Survey improperly contributed much the same sympathy, but even it no longer resides on the plus side of the official ledger.

So many people may have exited the labor force in May that the unemployment rate dropped to just 4.3% even though headline payroll gains were once again lackluster. The last time the ratio was this low George W. Bush was just a year into his first term, no one had yet much idea of the housing bubble because at that moment in May 2001 of greater concern was the dot-com bubble and its related recession that had yet to be realized in effect. It was then the last hurrah of the nineties economy.

It is very difficult to compare that 4.3% rate with this one, for the current regime looks nothing at all like that one even though for the past three years economists and policymakers have tried to make it stick. The current Fed estimates claim that “full employment” is almost certain to be at 4.3%, the modeled lower bound for its central tendency. We know what the FOMC will do for its June economic updates. They will move the goalposts yet again, forced to reduce their projections for what qualifies as long run labor potential because by next month the unemployment rate could be even less than the so-called lower bound.

But as we know all too well, and economists try all too hard to ignore, there is a vast difference in an unemployment rate where the labor force is at best static or barely rising and one where participation is as robust as headline payroll growth. A rate of 4.3% might be full employment in some other time, but not this one. Instead, the lower the unemployment rate goes now, the worse it is for policymakers clinging to it as if it was the same as it was sixteen years ago.

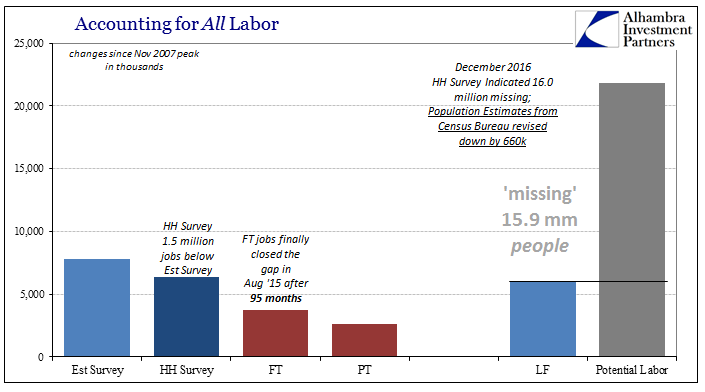

The payroll report overall was a complete washout. There had been even into 2016 several monthly labor updates that were, as I called them, perfect – strong headline for the Establishment Survey, a month where the labor force expanded, and corroboration via the Household Survey. The statistics for May 2017 are all the opposite. Just as a single perfect month did not suggest all that much that was meaningful, a single month entirely disappointing would not, either. However, these “bad” months are becoming more frequent and are now noticeable in sequence for how they are no longer somewhat offset by any “perfect” reports anymore.

Leave A Comment