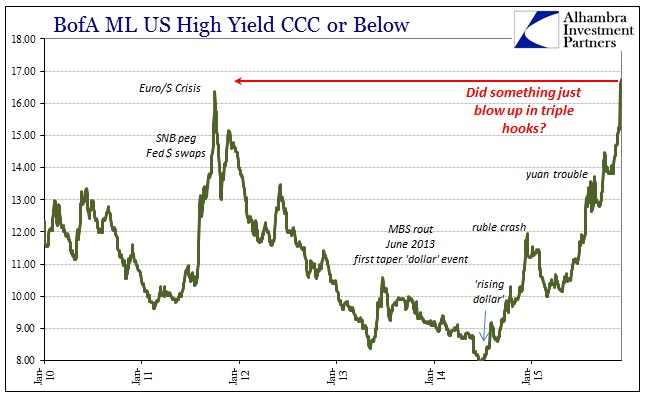

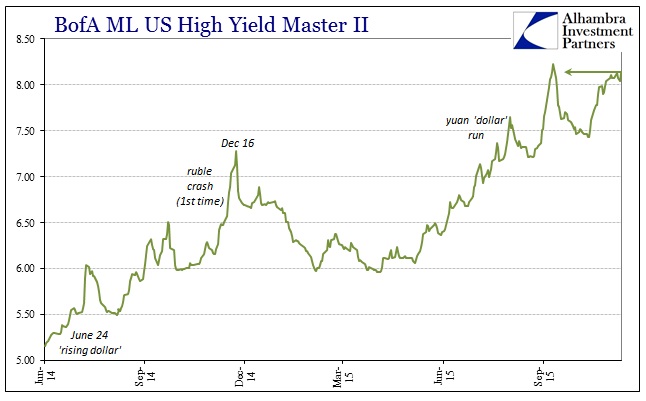

If the junk bond bubble was this week’s most visible inducement toward illiquidity, there have been more than enough indications that might corroborate and explain. With a few more days trading, the huge jump in BofAML’s CCC junk index rate has been confirmed – with another albeit smaller surge again yesterday. At now 16.74%, that is significantly above the prior “cycle” peak from early October 2011. Other junk price and yield indices still aren’t displaying any of the same desperation or urgency, but continue to be whittled down (in price) at an alarmingly steady rate.

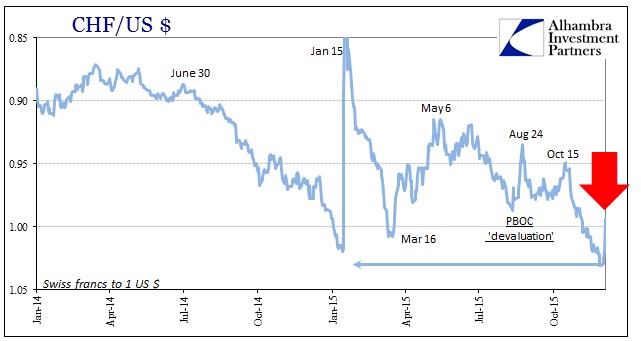

There are a few places in the “dollar” funding world that stand out as far as some kind of shift into December. First and foremost is the Swiss franc, which had devalued all the way past 1.03 at the end of last week. Starting this week, however, the franc has been hugely bid against the “dollar” tide, perhaps suggesting a huge layoff of risk based on (or part of) the ongoing events in junk (especially CCC). Whether or not that would be a dealer problem isn’t clear, but that would be the (mild) suggestion.

The last time the franc reversed this hard this fast, suddenly shifting from with the “dollar” run to against it, was that nearly two week period between the PBOC’s breaking its attempted CNY peg and the global liquidations that followed on August 24 and into the 25th.

The franc being exposed like this as a potential “flight to safety” (really a “flight” to risk reductions and funding backup) makes a compelling case for interpreting the potential junk problem as more than the usual that we have come to expect in this slower-motion collapse. As in August, there are innumerable Asian clues to further color any analysis and interpretation.

That starts with an enormous spike in offshore HIBOR rates that began only two trading days before our CCC explosion. The O/N rate in HIBOR (Hong Kong yuan liquidity) went from 2.913% on Friday, November 27 to 4.823% Monday (and then topping yesterday at an undoubtedly disruptive 8.328%, the highest since the last few days in September and that “dollar” and RMB breakout that was interrupted by the Golden Week). The yield on BofAML’s CCC index was similarly affected on Monday; 15.18% in published yield last Friday, November 27 and then whatever broke Monday to push it to 16.61%, and now 16.74%.

Related Posts

China Posts Largest-Ever Annual Trade Surplus With US: What’s It Mean?

China Posts Largest-Ever Annual Trade Surplus With US: What’s It Mean? Sensex Trades On A Dull Note; Realty Stocks Top Gainers

Sensex Trades On A Dull Note; Realty Stocks Top Gainers The Neoconservatives Are Back And World War III Edges Closer As Trump Appoints Hawk John Bolton

The Neoconservatives Are Back And World War III Edges Closer As Trump Appoints Hawk John Bolton Miners Take A Beating

Miners Take A Beating US PPI Beats Expectations – USD Ticks Up

US PPI Beats Expectations – USD Ticks Up Monday Brings Another Record Low Vol. Moment

Monday Brings Another Record Low Vol. Moment

Leave A Comment