Through no fault of my own I’ve recently found myself at the heart of the mainstream, short- volatility (VOL), media headlines. Ok, maybe that’s a bit disingenuous and I should take a little bit more ownership of the role I’ve played over the last several years regarding the volatility/VIX trade. I have written several dozen articles, several white papers that were sold to many an institution and hedge fund and participated in the social media realm with respect to trading volatility and VIX derivatives, namely VIX-leveraged ETPs. So when I woke up one morning to an email from a New York Times reporter… well it wasn’t expected or unexpected. The New York Times article was aimed at the short volatility trade, which is assumed to be a crowded trade. The article is titled Day Trading in Wall Street’s Complex ‘Fear Gauge’ Proliferates and well researched by Landon Thomas Jr., the New York Times reporter. Within the New York Times article I acquiesce to the notion that the short-Volatility trade is crowded, but to add a little more granularity to that statement I’d like to offer my statement is with regard to both sentiment and the term “trade” itself.

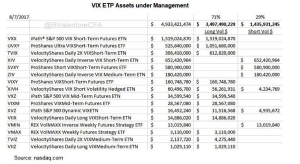

The reality is that on a dollar basis of assets under management VIX ETPs are more than twice as long VIX futures, as they are short for which it is identified most recently via nasdaq.com. And remember this is with respect to assets under management, something critically important to the so-called “crowded short-VOL trade”. For a calamitous unwind of the short-VOL trade that inspires so many naysayers to propose infinite losses and the blowing up of many short-VOL traders it would take a great deal many more assets under management to produce this would-be result and assuming appropriate risk management one needs for any investment.

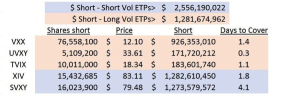

To reiterate, the chart above recognizes assets under management, which is critically important to a short squeeze thesis. There is simply too much liquidity in the likes of VXX, UVXY and TVIX to find validation for a crowded trade much less a short squeeze. This is mainly because the VIX-ETPs tend to be traded and not invested. This is something I understood long ago and to the extent I knew my strategy was contrary and ideal all at the same time. (Insert evil genius’s laugh) All the aforementioned ETPs have less than 2 days-to-cover. Now go take a gander at the likes of Intel (INTC). Eyes wide shut huh? OK, one more chart completely refuting, beyond any plausible contesting, that the short-VOL trade is crowded:

Look at where the greater proliferation of short dollars is presently. Nearly twice the dollars have found their way into shorting the short (inverse) VIX futures ETPs i.e. XIV and SVXY. This basically means there are more dollars dedicated to being long volatility. Giving credit where credit is due for this uncovering of facts goes directly to Valentine Ventures LLC. Having evidenced that the underlying characteristics of a crowded trade are not present in the short-VOL trade it should not go without recognition that it doesn’t have to be a crowded trade for traders and investors to witness significant losses from a faulty trading discipline with these VIX-leveraged ETPs. What I, Seth Golden, do as a trader and investor has never been promoted, but rather explained for its great return on capital invested (ROIC). My strategy/ies are representative of my abilities, dedication and experience and by no means do I desire to see folks jump into a volatility trading strategy just because they’ve seen my name in a headline. In short, my publications over the years have simply offered an opportunity that I already understood to be widely in use, but used with great human error. And as such I’ve offered information regarding the short-VOL trade as well as fundamental disciplines for utilizing VIX-leveraged ETPs.

Leave A Comment