Greetings,

“All is well” again in the global markets, with risk appetite returning as quickly as it dissipated late last year.

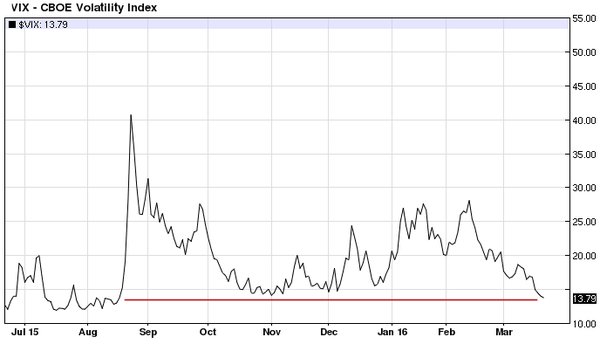

VIX is now at the lows we haven’t seen since the summer.

Source: barchart

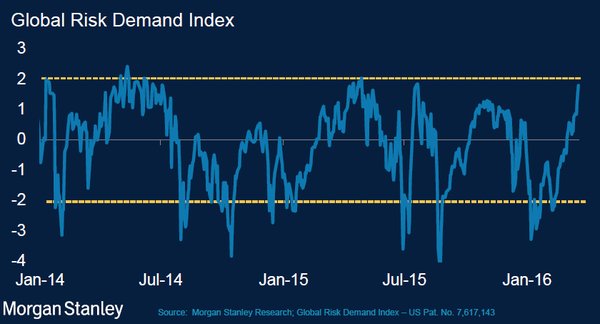

Here is the Morgan Stanley’s Risk Demand Index.

Source: Morgan Stanley

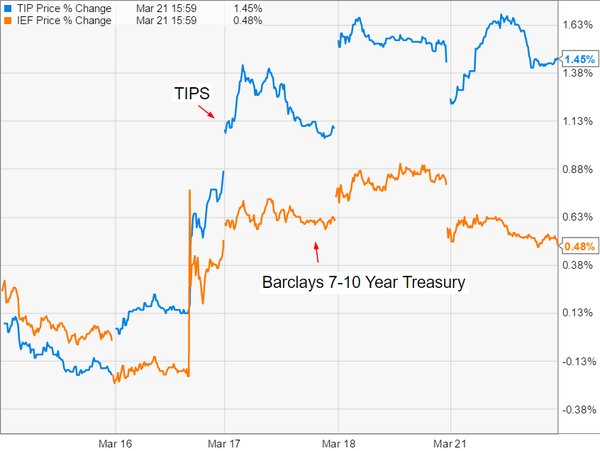

Inflation expectations turned higher as the dollar rally stalled. Below we see TIPS (inflation-linked treasuries) outperforming regular treasuries since the FOMC announcement last week.

Source: Ycharts.com

Higher inflation expectations in theory result in easier monetary conditions by lowering real rates. The next chart shows the 5yr TIPS yield (effectively the 5-year real rate) moving lower.

A weaker trade-weighted US dollar correlates well (recently) with higher inflation expectations.

However, Morgan Stanley suggests that the easier financial conditions in the US are not likely to last and the dollar will soon resume its rally.

Source: Morgan Stanley

Here is how the risk appetite party could end.

Source: Reuters (3/21)

Let’s switch to the Eurozone where we have a few observations to cover.

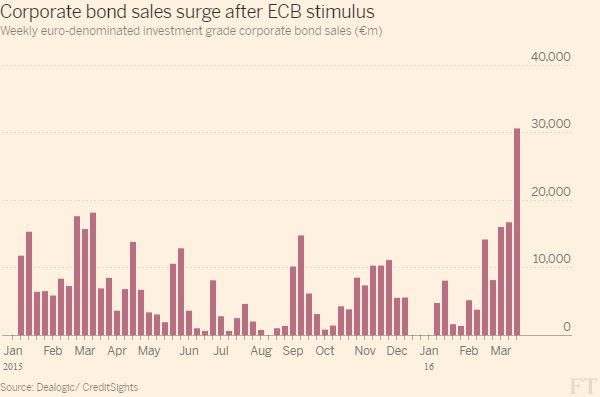

1. Corporate debt sales in the area spike to record levels as demand for ECB-eligible paper rises.

Source: @fastFT

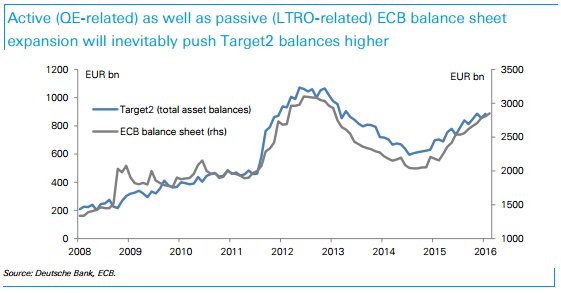

2. Rising Eurosystem balance sheet is likely to expand the so-called “Target2 imbalances” in which periphery national central banks owe money to the Eurosystem. On a consolidated basis, these cancel out because one of the largest assets on Bundesbank’s balance sheet is the loan to the Eurosystem. More on this later.

Source: ??@Fmirw

3. The German refugee crisis is proving expensive as the government works to absorb a couple of million people.

Source: @vexmark, @business

4. Speaking of government expenditures, here is the cost of pensions by country,

Source: ?@jsblokland, @business

5. There are signs that the Eurozone economic growth has been improving. Industrial production has risen (first chart below) and the Eurozone GDP tracker shows higher growth in Q1 (second chart below) .

Related Posts

E

AMD: Round 2, Buy Again

E

AMD: Round 2, Buy Again Starbucks Stock Soars Amid Starboard Value Stake – But Did Investors Celebrate Too Early?

Starbucks Stock Soars Amid Starboard Value Stake – But Did Investors Celebrate Too Early? Black Friday Deals Deja Vu: Some Of 2014’s Deals Are Back

Black Friday Deals Deja Vu: Some Of 2014’s Deals Are Back Continued Backing Up Of US Rates Extend The Greenback’s Gains

Continued Backing Up Of US Rates Extend The Greenback’s Gains EUR/USD: Buyers Retreating To The Trend Line

EUR/USD: Buyers Retreating To The Trend Line Market In-Review: Markets Exhibit Solid Optimism

Market In-Review: Markets Exhibit Solid Optimism

Leave A Comment