Our capital market assumptions for returns over the next 5 years forecast lower returns ahead, given moderate economic growth and stretched valuations. Take a look.

Written by: Richard Turnill (BlackRock.com)

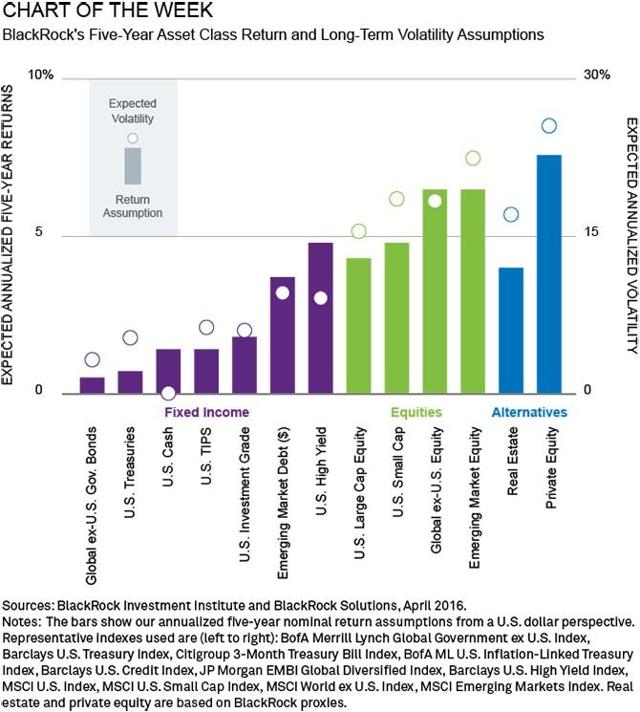

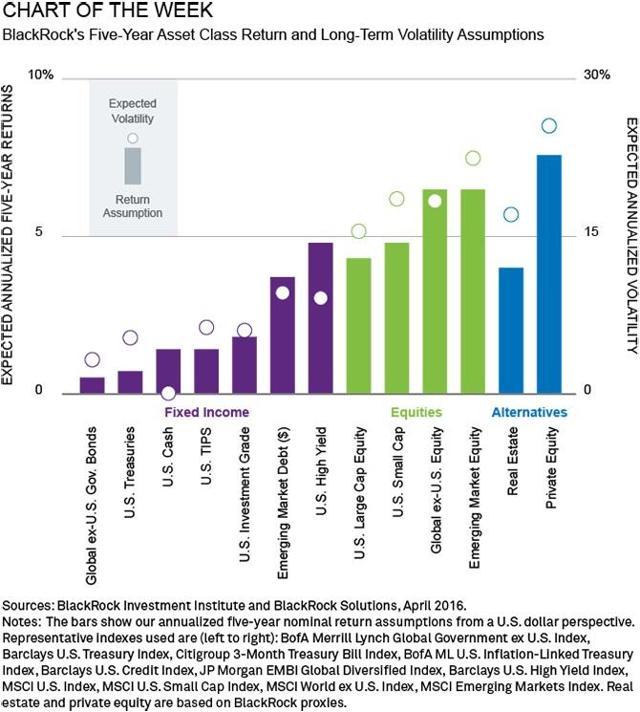

The bars in the chart below show our return assumptions for selected asset classes, while the dots show expected volatility. Higher returns generally come with more volatility.

Many of our return assumptions are now at or near post-crisis lows, with many expected returns below historical averages. These assumptions reflect high current valuations and lower global growth over the next five years, in line with a long, flat U.S. recovery.

No free lunch

We see portfolios made up of 60% equities and 40% fixed income producing annual returns:

Negative returns may also be more widespread, given that many benchmark rates hover around 0%. We now anticipate:

We see a wider gap between the prospective returns for safe-haven and risk assets, reflected in higher expected returns for equities versus bonds and for non-U.S. equities versus U.S. equities. Our international equity return estimates are now above the long-term average, thanks to improved valuations outside the U.S.

Alternatives come with higher volatility and illiquidity, but we believe real assets can offer portfolio diversification benefits.

The bottom line:

Generating higher returns over the longer term involves more volatility.

Related Posts

AUDUSD Daily Analysis – Monday, Nov. 20

AUDUSD Daily Analysis – Monday, Nov. 20 Amazon Crashes 10% – Blows Through Critical Support

Amazon Crashes 10% – Blows Through Critical Support- Weekly Economic & Political Timeline – Sept. 3

Turn Around Tuesday Sees Firmer Dollar, Rates, And Equities

Turn Around Tuesday Sees Firmer Dollar, Rates, And Equities Goldman Can’t Quite Figure Out What Happened To Tech Stocks On Friday

Goldman Can’t Quite Figure Out What Happened To Tech Stocks On Friday Gold Vs Cryptocurrencies: A New Inverse Trend To Forecast Both Markets In 2018?

Gold Vs Cryptocurrencies: A New Inverse Trend To Forecast Both Markets In 2018?

Leave A Comment