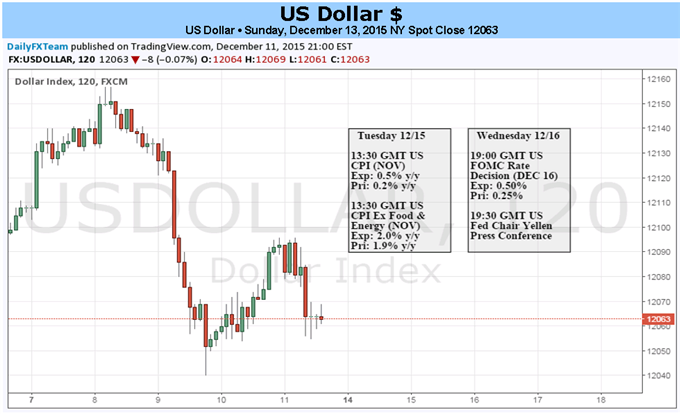

This week is when the rubber meets the road after months – years, even – of qualified remarks, convoluted press conferences, and opaque policy statements: the Federal Reserve will finally get on with it and raise its benchmark interest for the first time in nearly a decade. Historically, the Fed finds itself raising rates at a time when the labor market/inflation dynamic is just supportive enough to allow for policy tightening. Yet conditions today are relatively weaker than when the Fed raised rates last in June 2006:

Chart 1: The US Phillips Curve: October 1995 to October 2015

When the Fed raised rates last in June 2006, the Unemployment Rate was 4.6% and Core CPI was +2.6% y/y. The most recent Core CPI (+1.9% y/y) and Unemployment Rate (5.0%) readings suggest that this is a softer environment to hike rates in that in past cycles. The recognition of this reality is the cornerstone of our belief that, despite the US Dollar having been supported by higher US yields and thus rising rate expectations in 2015, the path is anything but clear going forward after the Fed’s meeting on December 16.

Much like the European Central Bank’s decision to cut its deposit rate on December which subsequently produced a Euro rally, it’s more than likely that the upcoming Fed rate hike has been priced into the US Dollar, leaving open the possibility of disappointment. In fact, the process of the rate hike being priced into markets has been the backbone of the US Dollar rally over the past three months:

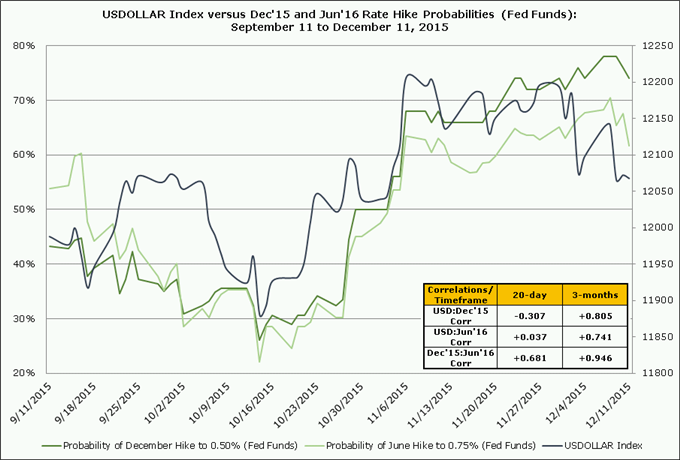

Chart 2: USDOLLAR Index vs December 2015 and June 2016 Rate Hike Probabilities

There are two material takeaways from the above chart. First, there has been a statistically significant +0.805 correlation between the USDOLLAR Index and the implied probability of a 25-bps Fed rate hike in December (per the Fed funds futures contract) over the past three months. Over the same timeframe, there has been a statistically significant +0.741 correlation between the USDOLLAR Index and the implied probability of a 25-bps rate hike in June 2016 – the next hike, from 0.50% to 0.75%. So, with the December 2015 hike priced in, markets have started to shift their focus on what the Fed’s next move is. If forward guidance will shape market expectations for when the Fed moves next in 2016, then there may be little support here for the US Dollar.

Related Posts

Construction Spending Details: Diving Into The Plusses And Minuses

Construction Spending Details: Diving Into The Plusses And Minuses BTCUSD Critical Levels Into The FOMC

BTCUSD Critical Levels Into The FOMC- U.S. Retail Stocks Slump, Oil Futures Surge

- E

China’s November Economic Data On A Strong Footing

- Yellen’s Last Testimony Before Congress And Gold

- MCW Energy: Innovative Oil Sands Extraction Technology Could Propel Stock Higher

Leave A Comment