Photo Credit: Ivan Walsh

Oracle (ORCL) Information Technology – Software | Reports December 16, After Market Close

Key Takeaways

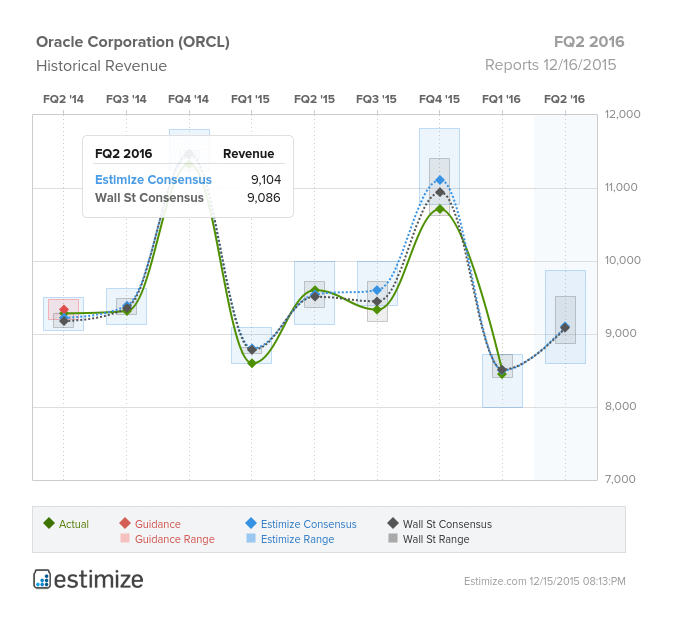

Coming into their FQ2 2016 earnings report, leading enterprise software company, Oracle (ORCL), is expected to fall short of estimates. What was once the preeminent enterprise provider, Oracle finds itself at a crossroads with the emergence of cloud infrastructure and services. The company’s efforts to transition from license to cloud based subscriptions has come at the expense of shareholders. In fact, revenue estimates have fallen short 5 of the past 6 quarters with similar expectations going into December 16. For the second fiscal quarter 2016, the Estimize consensus calls for revenue of $9.106 billion and EPS of $0.61, slightly higher than Wall Street’s estimates. Compared to FQ2 2015, this represents a year over year decline in revenue and EPS of5% and 11%, respectively. Moving forward, the company’s ongoing transition coupled with a strengthened U.S dollar will continue to hamper operations and growth.

A large portion of Oracle’s anemic revenue growth comes amid efforts to transition from license to cloud based subscriptions. At the moment, cloud computing consists of three major components, software as a service (Saas), platform as a service (Paas), and infrastructure as a service (IaaS). By rapidly strengthening their offerings in each service, Oracle faces stiff competition from the likes of Amazon Web Services, Google, and Microsoft; each of which represent a large portion of cloud computing. Even though Oracle’s cloud services are growing, its ongoing attempt to catch up will continue to drive down margins and revenue in the near-term.

Leave A Comment