This is getting just plain nuts. Here is what Janet Yellen said today about the possibility of negative interest rates:

In light of the experience of European countries and others that have gone to negative rates, we’re taking a look at them again because we would want to be prepared in the event that we needed to add accommodation.“

The operative words here are “European countries” and “add accommodation”. Yet even a brief reflection on those items demonstrates that Janet is a delusional Simpleton. To adopt Jim Kunstler’s felicitous phrase about Senator Rubio’s 4-Peat incantation during the last GOP debate, our financial system is being led by a monetary android with a broken flash drive.

She says the same damn stupid thing over and over, endlessly.

Someone should tell Janet and her posse of Keynesian money printers that there is no such economic ether as “accommodation”. That’s Fed groupspeak for their utterly erroneous conceit that the US economy is everywhere and always sinking towards collapse unless it is countermanded, stimulated, supported and propped up by central bank policy intervention.

No it isn’t. Janet may prefer a dutch boy hair cut, but she’s not got her finger in the dike, nor is she warding off any other catastrophe. The deluge that is coming is actually the handiwork of the Fed and its bubble ridden Wall Street casino, not the capitalist hinterlands of main street.

There are only two tangible transmission channels through which the Fed can impact our $18 trillion main street economy, as opposed to merely subsidizing Wall Street speculators to artificially bid up the price of existing financial assets.

It can inject central bank credit conjured from thin air into the bond market in order to raise prices and lower yields. And it can falsify money market interest rates and the yield curve. Both of these effects are aimed at inducing businesses and households to borrow more than they would otherwise, and to then spend more than they produce.

That’s the old Keynesian parlor trick and, yes, it worked 50 years ago when Janet’s Keynesian professors first had their way with America’s virgin balance sheets. But now those household and business balance sheets are all used up because we are at Peak Debt, along with most of the rest of the world.

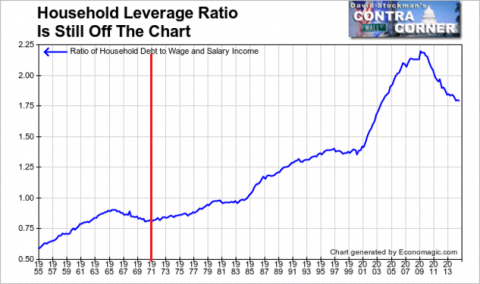

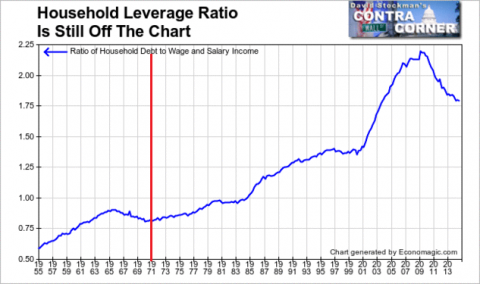

Indeed, in the case of the US household sector the massive leveraging up of wage and salary income betweenthe late 1960s and 2008 has now begun to slowly reverse.The credit string that the Fed is pushing on is evident in the chart below. But apparently Janet is still in a time warp obeying the injunctions of James Tobin’s ghost wafting up from the earlier side of the red horizontal.

Accordingly, the stimulative effect of low and ultra-low interest rates never really leaves the canyons of Wall Street. And when it does, it trickles its way into credit extensions to the weakest borrowers left in the land. That is, students and subprime auto borrowers.

Outside of those dubious precincts – where the next wave of defaults or government bailouts will surely occur – there has actually been negative growth in household debt since the financial crisis.Notwithstanding 86 months of ZIRP and its current equivalent, total household debt is still $400 billion below it pre-crisis peak, and mortgage and credit card debt are down by more than $1 trillion.

Likewise, the $2 trillion rise in total business debt outstanding has not gone into productive assets such as tangible plant, equipment and technology. It has been short-circuited into financial engineering by the false financial bubble fostered by Fed policies. That is, massive stock buybacks and M&A deal volumes have simply used the agency of the stock options obsessed C-suite to recycle newly issued business debt right back into the canyons of Wall Street.

So if 86 months of ZIRP has already proved that the old Keynesian parlor trick—–which is the say, the household and business credit channel of monetary policy transmission—-is a dead letter, why in the world would Janet think that a few more basis points through the negative side of 0.0% would make any difference?

Related Posts

Capitulation: Yen Plunges, Nikkei Soars After BOJ’s Uchida Says “Will Not Raise Rates When Markets Are Unstable”

Capitulation: Yen Plunges, Nikkei Soars After BOJ’s Uchida Says “Will Not Raise Rates When Markets Are Unstable” Money Flows After The Elections

Money Flows After The Elections The Ultimate Must Have Investment

The Ultimate Must Have Investment Is Oil Going To $70 Or $20? The Answer Might Surprise You . . .

Is Oil Going To $70 Or $20? The Answer Might Surprise You . . . S&P 500: At Death’s Door

S&P 500: At Death’s Door Starbucks Enables Use Of Reusable Cups For Drive-Thru And Mobile Orders

Starbucks Enables Use Of Reusable Cups For Drive-Thru And Mobile Orders

Leave A Comment