US trade statistics for February improved in both exports and imports, but there are questions as to the reason for the reverse and whether it is actually meaningful. After abysmal performance in every segment and category in January, there was some give back in February including positive numbers in some places. That suggests that January’s trade activity might have been suppressed (financing issues?) and shifted somewhat into the following month (and then the 29th day may have added something further).

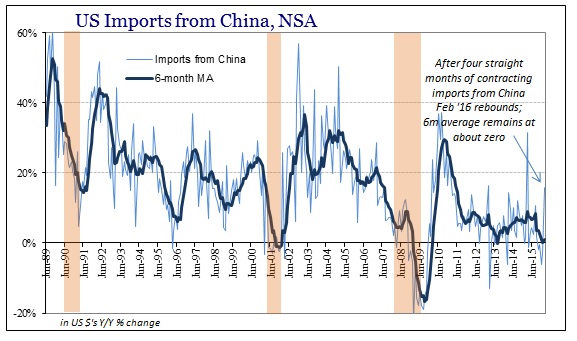

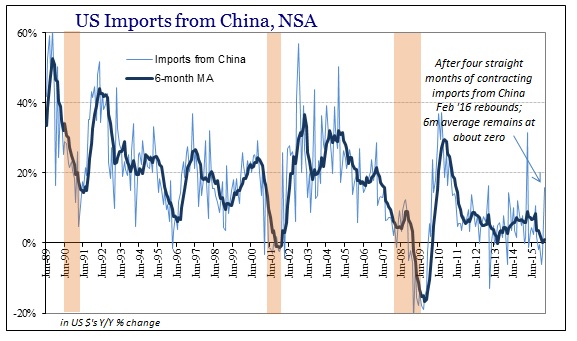

US imports from China, for example, rose 15.8% in February year-over-year after contracting for the four months prior. This variation, with sudden surges out of nowhere spread between very low or contracting months, has been the dominant feature of the past year and a half. Despite what seems like a very good number for February, the 6-month average remains barely positive at +1.1% because that +15.8% only replaces +10.8% from August (the last time there was a similar “good” month) in the moving average. The net result is the usual mainstream proclamations that the corner has been turned while Chinese industry is still stuck between capacity built for sustained +25% to +30% US import growth and the actual import level that remains at or even below zero if highly irregular in achieving it.

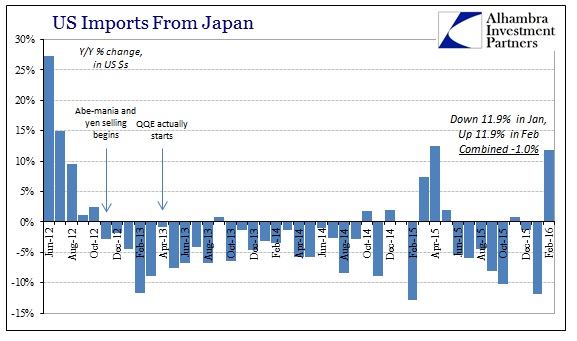

We see this two-month pattern replicated all over the data. Japanese imports to the US fell 11.9% in January, which was the second worst month since 2009. In February, however, imports rebounded by the same 11.9%. Combining both January and February, US imports from Japan fell 1% from January and February 2015 where import activity was already 6.3% less than the same two months in 2014. In other words, the slowdown continues at the same uneven pace which makes this whatever economic condition unlike anything we have seen before.

US imports from the European Union fell an enormous 7.3% in January, which was the worst month since October 2009. In February, imports from Europe rose 2.7%, leaving the combined totals for the two months 2.3% lower than the same two months in 2015. That is slightly worse mathematically than the 6-month average of +0.9%; in reality it again suggests the same zero or lower growth of the slowdown/recession despite the large variation month to month.

Related Posts

Holiday Spending Season Begins With Decline At Brick-And-Mortar Outlets Offset By Jump In Online Purchases

Holiday Spending Season Begins With Decline At Brick-And-Mortar Outlets Offset By Jump In Online Purchases Silver Found Intraday Buyers At The Equal Legs Area

Silver Found Intraday Buyers At The Equal Legs Area Kraken secures money license registrations in Spain and Ireland

Kraken secures money license registrations in Spain and Ireland- Missing DeFi security layer found in a new company release

- Ukraine-based blockchain firm reports company ‘stronger’ one year into war

Rates Spark: Supply Test Ahead

Rates Spark: Supply Test Ahead

Leave A Comment