I’ve written a fair amount about bond market risk appetites over the past year or so. Today, I’m watching the leveraged loan market even more closely because it’s moving in the opposite direction of the stock market across a variety of time frames.

Typically, risk appetites for leveraged loans (as measured by prices relative to same duration treasuries) and stock prices, especially small caps, are very highly correlated. Because leveraged loans are many times a key component of mergers and acquisitions, it makes perfect sense that waning demand for this type of credit investment could make for waning corporate demand for equities (not to mention buybacks). And this is exactly what’s happening right now.

“Where we are seeing it impact behaviors is at the smaller and middle size end of the market so the mid market. Deals are getting to be more expensive. The flex terms in financings have gone up significantly. And our pipeline in private credit so mezzanine, direct lending, and special situations opportunity are up significant as a result of some of the dislocation we’re starting to see…. What has become interesting more recently is what’s happening within the liquid part of the leverage credit markets. So the bank loan, leverage loan market the high yield market…there is a significant reduction in liquidity…if you see a screen price, it doesn’t necessarily mean that that’s achievable on any volume whatsoever and that is creating quite a bit of interesting tension in the markets.” -KKR Head of Global Capital & Asset Management, Scott Nutgall (via Avondale)

That reduction in liquidity is showing in the market right now as the Leveraged Loans ETF tests multi-year lows amid a modicum of selling pressure.

What I find striking is that even as risk appetites for leveraged loans (blue line in the chart below) have deteriorated, stocks have rallied this week:

Related Posts

Wells Fargo Expands Class-Action Settlement For Retail Sales Practices To $142M

Wells Fargo Expands Class-Action Settlement For Retail Sales Practices To $142M Fed’s Liftoff: A Shift In Sentiment

Fed’s Liftoff: A Shift In Sentiment FV

Have The QQQ’s Wrecked The Bull Market?

FV

Have The QQQ’s Wrecked The Bull Market? E

Solar Stocks Recover As Some Investors See Silver Linings Of JKS Results

E

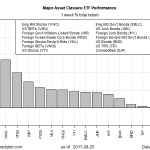

Solar Stocks Recover As Some Investors See Silver Linings Of JKS Results Across-The-Board Gains For Major Asset Classes Last Week

Across-The-Board Gains For Major Asset Classes Last Week- USD/CAD Daily Analysis – Wednesday, Nov. 8

Leave A Comment