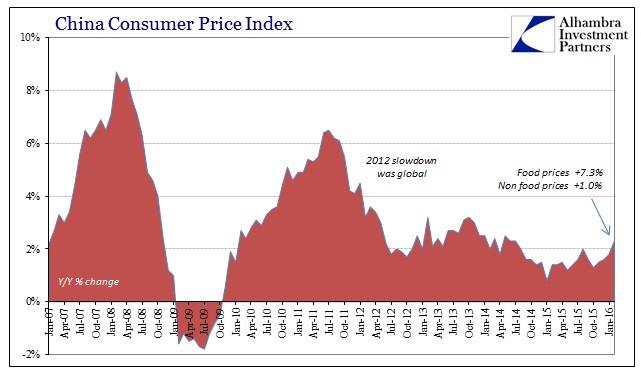

Europe is not the only location seeking out more “inflation”, as almost any central bank around the world except Banco do Brasil would do anything to find it. The ECB provided more emphasis in their panicked escalation today. In China, by contrast, consumer prices moved to +2.3% in February, which was the highest rate since July 2014. Unfortunately, that rise was more so non-economic factors than the expected byproduct of successful monetary integration, as food prices surged 7.3% while non-food “inflation” actually sunk to just +1.0%.

Even the usual sunny disposition from the mainstream was lacking for this CPI report, as surely economists recognize that food inflation appearing now at this weak economic point only increases the negative economic pressure.

China’s consumer inflation accelerated faster-than-expected in February due to rising food prices but another fall in upstream prices is likely to add to concerns about growing deflationary pressures, which could trigger further policy easing.

And:

Economists say the upward trend in CPI is unlikely to sustain. HSBC Chief China Economist Qu Hongbin “attributed the easing contraction to stabilizing commodity prices during the period.” Qu further emphasized that temporary factors and downward pressure (on non-food prices) have predominantly caused the rise in inflation, and their influence remains heavily.

From that there was scant improvement in producer prices which continue to contract at more than 4%. The Chinese PPI was estimated at -4.9% in February, the 13th straight month worse than -4%. The wider, parallel Purchasing Price Index for Industrial Producers was -5.8% in the latest estimate, the 14th consecutive month less than -5%. It isn’t coincidence that negative producer and industrial prices accompany, usually, global recession.

The results leave economists perplexed as to why there isn’t any more “stimulus” forthcoming. The difference between what China is “supposed” to do and what it has done is the same as what has been in place since “reform” was first identified in late 2013/early 2014. In other words, where economists believe that any authority should do anything in its perceived power to boost growth, the Chinese have shown a different understanding about that “growth” as China, and its overcapacity, fit into the global system. As their trade numbers amply confirmed, there is no growth at all, leaving only indications that as bad as it has been there might yet be much worse.

Related Posts

Will Ebay Do More Than Improving Its Look And Feel?

Will Ebay Do More Than Improving Its Look And Feel? Morning Call For Tuesday, March 20

Morning Call For Tuesday, March 20 Russia Moves Toward Increasing Economic Freedom

Russia Moves Toward Increasing Economic Freedom SP 500 And NDX Futures Daily Charts – Goldman Says ‘No Fear’ And Market Listens

SP 500 And NDX Futures Daily Charts – Goldman Says ‘No Fear’ And Market Listens Toll Brothers: Strong Financials, Buybacks…And Housing Jitters

Toll Brothers: Strong Financials, Buybacks…And Housing Jitters Trader puts faith in crypto despite the failed first investment

Trader puts faith in crypto despite the failed first investment

Leave A Comment