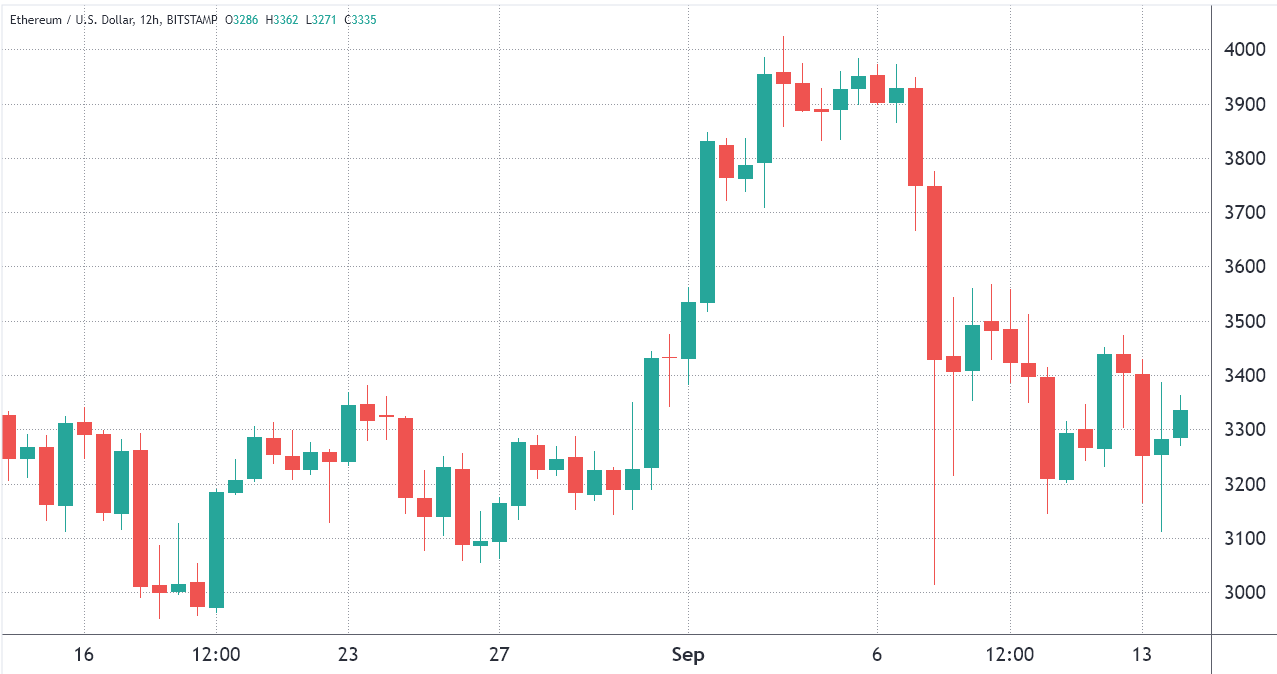

According to derivatives markets, Ether (ETH) traders are still confident that there is the chance formore upside even though the 23% correction on Sept. 7 took a hit on prices.

Ethereum network congestion also peaked on Sept. 7 when the average transaction fee reached $60, and since then it has remained above $17. As a result of the lingering challenges experienced by the network, investors have shifted into Ethereum competitors with bridge and layer-two capabilities. For example, Polkadot’s DOT rose by 29% over the past week and Algorand’s ALGO spiked 67%.

Undoubtedly, there’s a quest for interoperability and layer-two scaling solutions, aiming to quickly meet the explosive demand for nonfungible tokens (NFTs) and decentralized finance (DeFi) applications.

Whether the Ethereum network will sustain its absolute leadership position seems irrelevant right now, as the industry’s net value locked (adjusted total value locked) in smart contracts has risen from $13.6 billion in December 2020 to its current $82 billion.

Regulatory fear coming from the United States is likely curbing investors’ optimism in cryptocurrencies. According to a document released by a House committee on Sept. 13, lawmakers aim to close a loophole that previously allowed investors to claim capital gains deductions. The Internal Revenue Service currently considers cryptocurrencies as property in “wash sales,” and as a result, they are exempted from 30-day repurchase rules.

ETH futures data shows bulls are still “bullish”

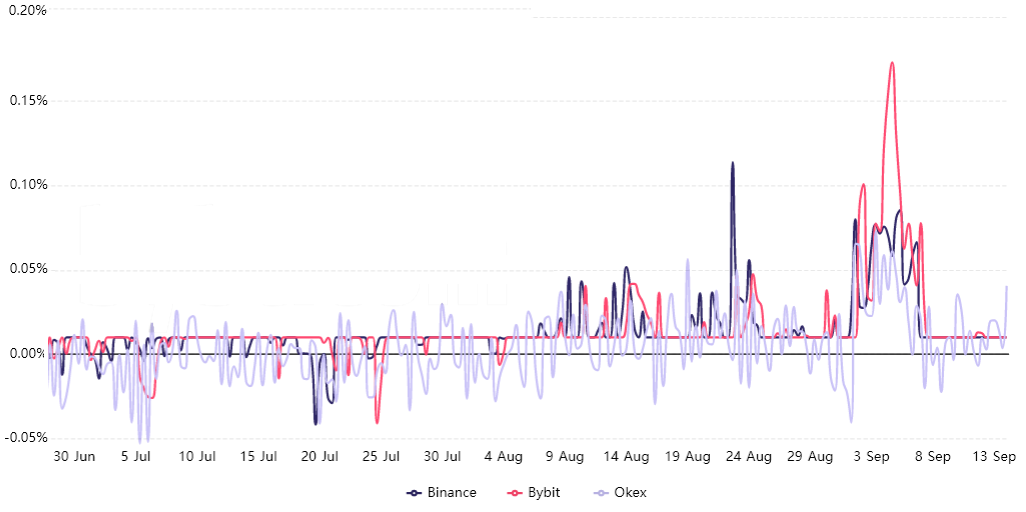

Ether’s quarterly futures are the preferred instruments of whales and arbitrage desks. Due to their settlement date and the price difference from spot markets, they might seem complicated for retail traders. However, their most notable advantage is the lack of a fluctuating funding rate.

These fixed-month contracts usually trade at a slight premium to spot markets, indicating that sellers request more money to withhold settlement longer. Consequently, futures should trade at a 5% to 15% annualized premium on healthy markets. This situation is known as “contango” and is not exclusive to crypto markets.

To understand whether this movement was exclusive to those instruments, one should also analyze perpetual contracts futures data. Even though longs (buyers) and shorts (sellers) are matched at all times in any futures contract, their leverage varies.

Consequently, exchanges will charge a funding rate to whichever side is using more leverage to balance their risk, and this fee is paid to the opposing side.

At the moment, there are no signs of weakness from Ether derivatives markets, and this could be interpreted as a bullish indicator. Investors’ attention remains focused on developments in regulation and Ethereum 2.0, which everyone assumes should settle the scalability problem for good.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Related Posts

Retailers Are Going Nuts (To The BLS)

Retailers Are Going Nuts (To The BLS) Crypto donations amplify speed and global reach during crisis

Crypto donations amplify speed and global reach during crisis E

Is High Yield Signaling An All Clear?

E

Is High Yield Signaling An All Clear? Housing: A Big Miss In Permits With Important Ramifications

Housing: A Big Miss In Permits With Important Ramifications Hess Corporation Misses On Q4 Earnings, Revenues

Hess Corporation Misses On Q4 Earnings, Revenues- Billion Dollar Unicorns: Splunk Outpaces Market Expectations

Leave A Comment