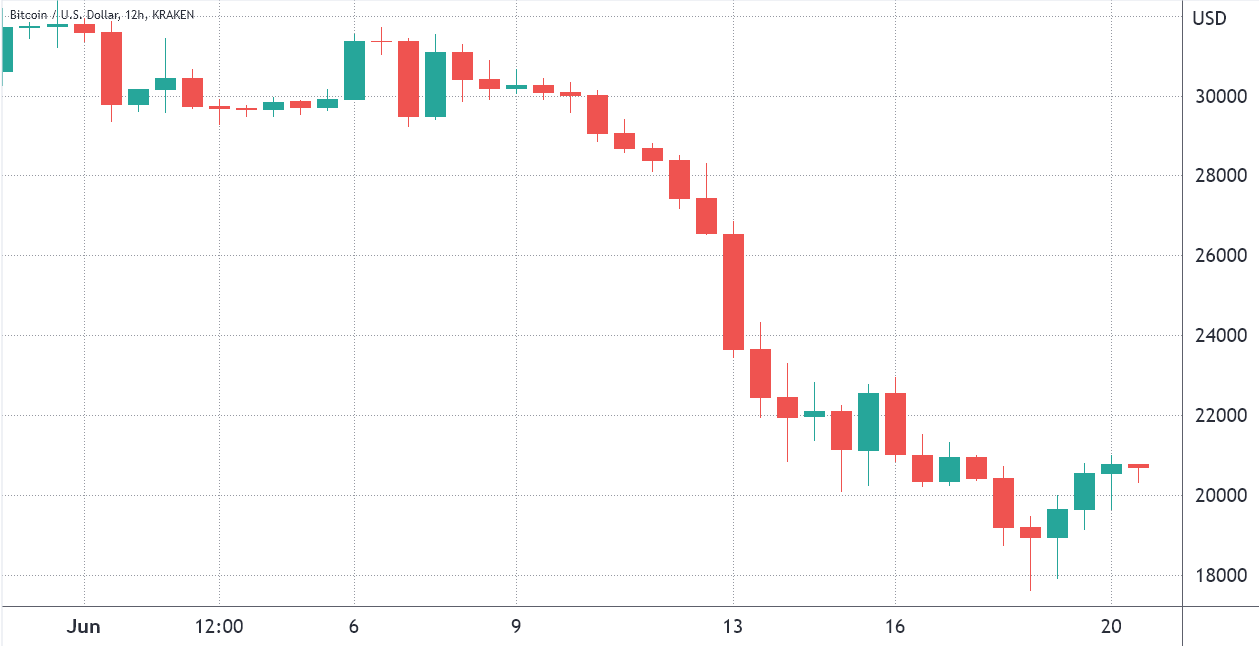

Bitcoin’s (BTC) month-to-date chart is very bearish, and the sub-$18,000 level seen over the weekend was the lowest price seen since December 2020. Bulls’ current hope depends on turning $20,000 to support, but derivatives metrics tell a completely different story as professional traders are still extremely skeptical.

The U.S. Federal Open Market Committee raised its benchmark interest rate by 75 basis points on June 15, and Federal Reserve Chairman Jerome Powell hinted that more aggressive tightening could be in store as the monetary authority continues to struggle to curb inflation. However, investors and analysts fear this move will increase the recession risk. According to a Bank of America note to clients issued on June 17:

“Our worst fears around the Fed have been confirmed: they fell way behind the curve and are now playing a dangerous game of catch up.”

Furthermore, according to analysts at global investment bank JPMorgan Chase, the record-high total stablecoin market share within crypto is “pointing to oversold conditions and significant upside for crypto markets from here.” According to the analysts, the lower percentage of stablecoins in the total crypto market capitalization is associated with a limited crypto potential.

Currently, crypto investors face mixed sentiment between recession fears and optimism toward the $20,000 support gaining strength, as stablecoins could eventually flow into Bitcoin and other cryptocurrencies. For this reason, analysis of derivatives data is valuable in understanding whether investors are pricing higher odds of a downturn.

The Bitcoin futures premium turns negative for the first time in a year

Retail traders usually avoid quarterly futures due to their price difference from spot markets, but they are professional traders’ preferred instruments because they avoid the perpetual fluctuation of contracts’ funding rate.

These fixed-month contracts usually trade at a slight premium to spot markets because investors demand more money to withhold the settlement. This situation is not exclusive to crypto markets. Consequently, futures should trade at a 5%-to-12% annualized premium in healthy markets.

To exclude externalities specific to the futures instrument, traders must also analyze the Bitcoin options markets. For example, the 25% delta skew shows when Bitcoin market makers and arbitrage desks are overcharging for upside or downside protection.

In bullish markets, options investors give higher odds for a price pump, causing the skew indicator to fall below -12%. On the other hand, a market’s generalized panic induces a 12% or higher positive skew.

Analysts expect “maximum damage” ahead

Some metrics suggest that Bitcoin may have bottomed on June 18, especially since the $20,000 support has gained strength. On the other hand, market analyst Mike Alfred made it clear that, in his opinion, “Bitcoin is not done liquidating large players. They will take it down to a level that will cause the maximum damage to the most overexposed players like Celsius.”

Until traders have a better view of the contagion risk from the Terra ecosystem implosion, the possible insolvency of Celsius and the liquidity issues being faced by Three Arrows Capital, the odds of another Bitcoin price crash are high.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Related Posts

Peeking At The Future: Using CoT To Assess Hedge Fund, Noncommercial Positions

Peeking At The Future: Using CoT To Assess Hedge Fund, Noncommercial Positions 3 ‘Strong Buy’ Tech Stocks To Watch Closely

3 ‘Strong Buy’ Tech Stocks To Watch Closely The Passive Indexing Trap

The Passive Indexing Trap Will Your Portfolio Survive The Apocalypse?

Will Your Portfolio Survive The Apocalypse? August 2018 Beige Book: Reading Between The Lines – Rate Of Economic Expansion Improved

August 2018 Beige Book: Reading Between The Lines – Rate Of Economic Expansion Improved Weekly Economic & Political Timeline – 4/3/2016

Weekly Economic & Political Timeline – 4/3/2016

Leave A Comment