The regulatory scrutiny of blockchains and cryptocurrencies is increasing. From the cryptocurrency mining ban in China to President Joe Biden’s Working Group on Financial Markets, convened by Treasury Secretary Janet Yellen, the economic activities that support and are enabled by blockchains have become a significant concern for policymakers. Most recently, a provision in the proposed 2021 infrastructure bill amends the definition of a broker to expressly include “any person who […] is responsible for regularly providing any service effectuating transfers of digital assets on behalf of another person.”

The stated goal of this “miner-as-broker” policy change is to improve the collection of tax revenues on cryptocurrency capital gains by enhancing the ability of tax collectors to observe cryptocurrency trades. Since cryptocurrency miners regularly validate transactions that transfer digital assets, such as cryptocurrencies, on behalf of cryptocurrency holders, these miners would appear to satisfy this definition of a broker. Unsurprisingly, many in the cryptocurrency industry have raised concerns.

One key feature of blockchain technology is competitive decentralized record-keeping. The pros and cons of this new form of record-keeping relative to traditional centralized financial databases are an active debate. But the new regulation might produce a premature end to this debate.

Related: Authorities are looking to close the gap on unhosted wallets

What are the direct consequences of defining miners as brokers?

First, miners — at least those located in the United States — would be subject to significantly enhanced requirements for reporting to the Internal Revenue Service. The cost to miners of complying with such requirements is likely to be large and largely fixed. Miners would need to bear these costs, regardless of how much mining power they have and before they mine a single block. This will deter entry and likely cause more centralized control or concentration of mining power.

Second, these broker-miners would be responsible for satisfying Know Your Customer regulations. Given the pseudo-anonymous nature of most cryptocurrencies, such a policy would limit the types of transactions broker-miners would be able to process to non-anonymous transactions. How would this work? Presumably, I would register with a miner (linking my driver’s license with a Bitcoin address, say), and miners would only validate transactions on behalf of their registered users. But if that miner happens to be small (have small mining power), then my transactions are less likely to be processed on the Bitcoin (BTC) network. Perhaps, it would be better if I (and you) register with a larger miner. Or perhaps, we should all just use Coinbase and allow a miner to handle transactions on behalf of Coinbase. Again, the impact here is a greater concentration of mining power.

Combined, this policy is likely to increase the concentration in U.S. cryptocurrency mining while raising the costs of mining and possibly reducing the overall amount of mining that takes place; that is, the policy would shift mining within the U.S. away from the “shadowy faceless groups of super-coders” recently described by Sen. Elizabeth Warren, but perhaps increase the reliance of users on such faceless super-coders outside of the United States.

What are the global consequences of defining miners as brokers?

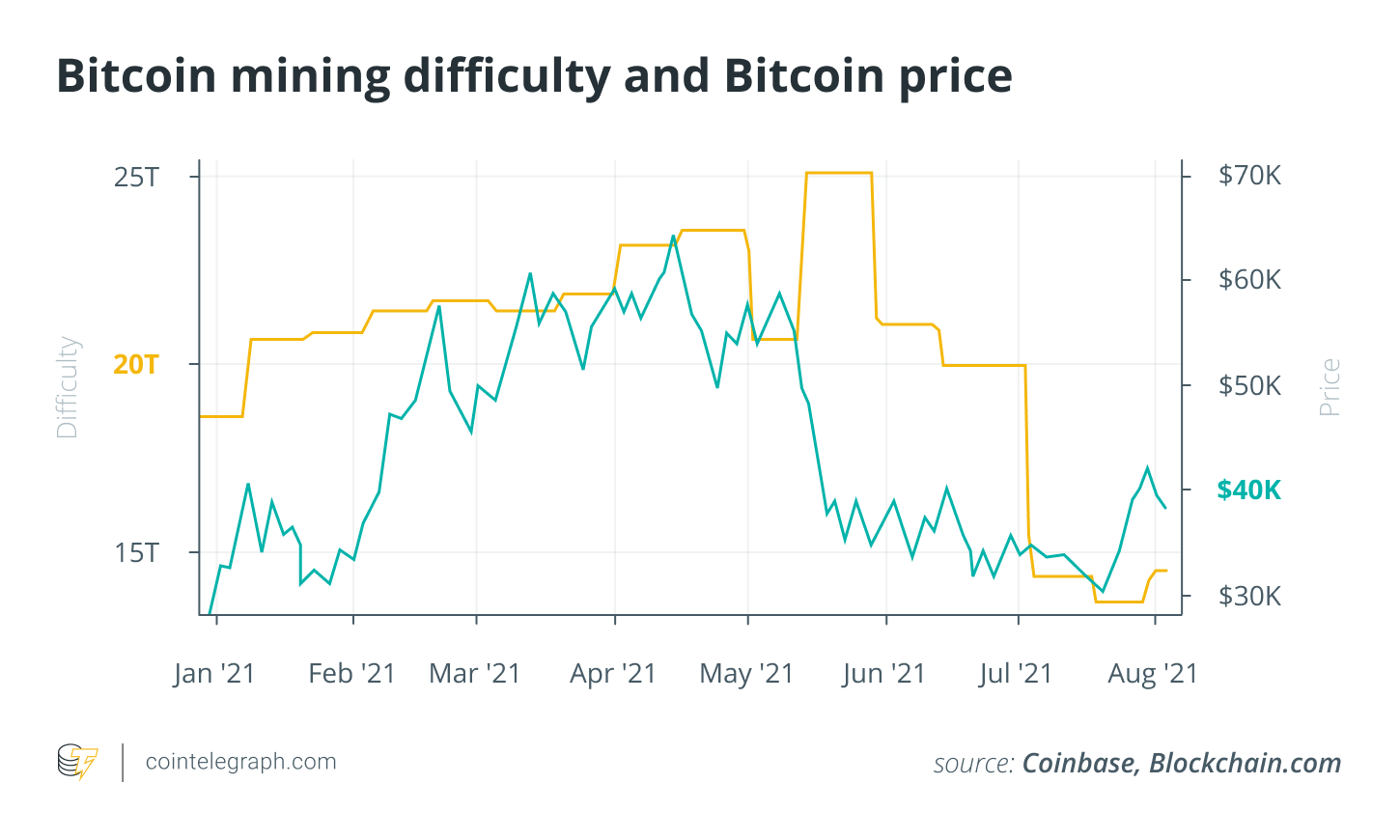

Part of the global impact of the proposed provisions in the infrastructure bill depends on the relative importance of U.S. cryptocurrency mining operations with the context of mining worldwide. Recent history provides some perspective. In June, China stepped up enforcement of its Bitcoin mining ban. The result was far fewer miners. We can see this in the drop in mining difficulty observed at the beginning of July. The mining difficulty governs the rate at which transactions are processed (about 1 block per 10 minutes on Bitcoin). With few miners, the difficulty falls to keep the transaction rate constant.

The lower level of mining difficulty requires less electricity to mine a block. The block reward is constant. The price of Bitcoin did not fall with the decreased difficulty in July. Here are three things to note:

The lower level of mining difficulty requires less electricity to mine a block. The block reward is constant. The price of Bitcoin did not fall with the decreased difficulty in July. Here are three things to note:

These features are likely to lead to a consolidation or concentration of mining power. If the new regulation — particularly the broker designation of miners — goes ahead, we can probably expect a similar impact.

Related: If you have a Bitcoin miner, turn it on

Is higher concentration inherently bad news?

Much of the security thesis of blockchain technology is rooted in decentralization. No person has incentives to exclude transactions or past blocks. When one miner has substantial mining power — a high likelihood of solving multiple blocks in a row — they may be able to alter part of the blockchain’s history. This situation is called a 51% attack and raises concerns about the immutability of the blockchain.

There are two related consequences of the proposed policy. First, higher concentration, by definition, puts miners closer to the mark where they can effectively alter the blockchain ledger. Second, and perhaps more subtle, the profitability of an attack is higher when the cost of mining falls — it is just cheaper to attack.

As my co-authors and I argue in ongoing research, however, such security concerns stem entirely from Bitcoin’s mining protocol, which recommends miners add new transactions to the longest chain in the blockchain. We argue that the potential success of 51% attacks derives entirely from this recommendation for coordinating miners on the longest chain. We show how alternative coordination devices may enhance a blockchain’s security and limit the security consequences of increased mining concentration.

No competition, no blockchain

Whether the current provisions concerning digital assets in the 2021 U.S. infrastructure bill pass or not, policymakers appear ready to enhance regulation and the reporting of cryptocurrency trades. While the debate has mostly focused on the tradeoffs of an enhanced monitoring of cryptocurrency trading by the U.S. government and the potential harm to U.S. innovation in blockchain, it is critical for both policymakers and innovators to consider the likely impact of such policies on competition within cryptocurrency mining, as this competition plays a critical role in securing blockchains.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph, nor Carnegie Mellon University or its affiliates.

Leave A Comment