Data shows that AAVE and Polygon (MATIC) traders are currently being paid up to 4.3% per week to long future contracts.

In the crypto markets, traders are usually bullish, or at least the majority of retail investors are. This causes an interesting phenomenon as it incentives arbitrage desks and whales to sell futures contracts while simultaneously buying on regular spot exchanges.

Perpetual futures automatically rebalance daily

Unlike regular monthly contracts, perpetual futures prices are very similar to those at regular spot exchanges. This makes retail traders’ lives a lot easier as they no longer need to calculate the futures premium or manually roll over positions near expiry.

The funding rate allows this magic to occur, and it is charged from longs (buyers) when they are demanding more leverage. However, when the situation is inverted and shorts (sellers) are over-leveraged, the funding rate goes negative, and they become the ones paying the fee.

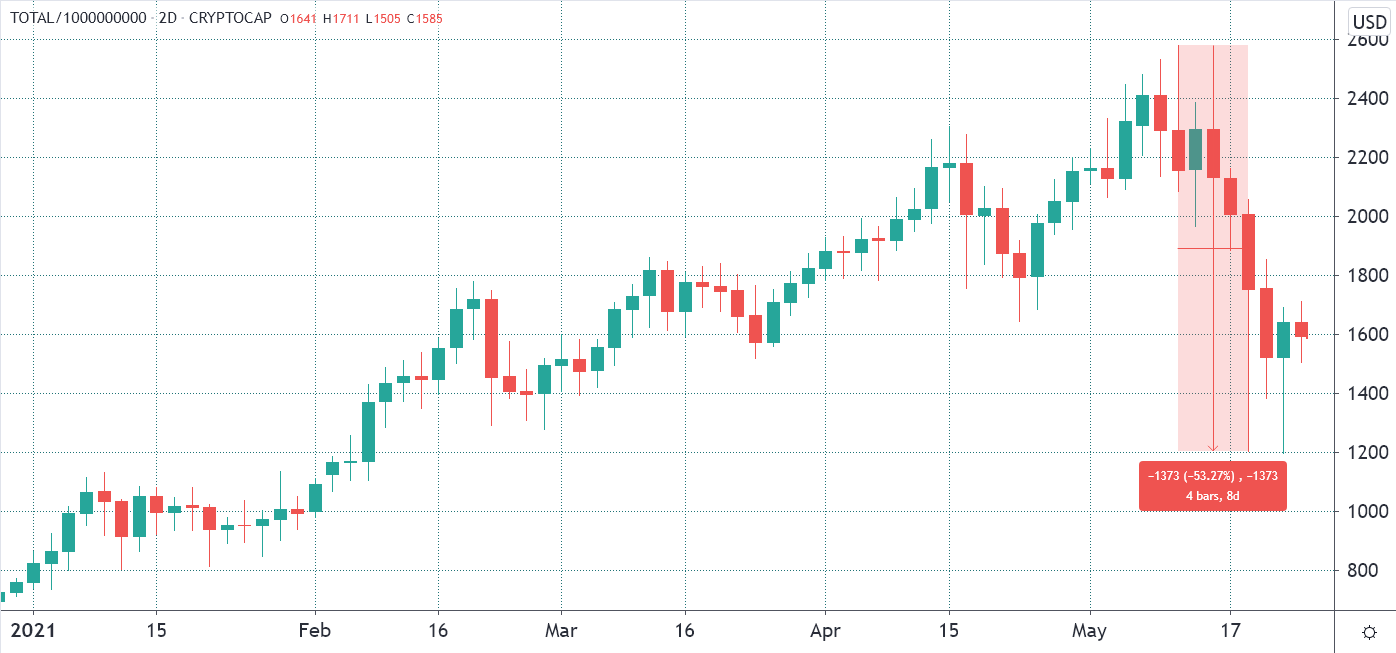

On May 19, as cryptocurrency markets collapsed, AAVE’s futures open interest dropped from $200 to $82 million as longs either closed their positions on stop orders or got forcefully liquidated.

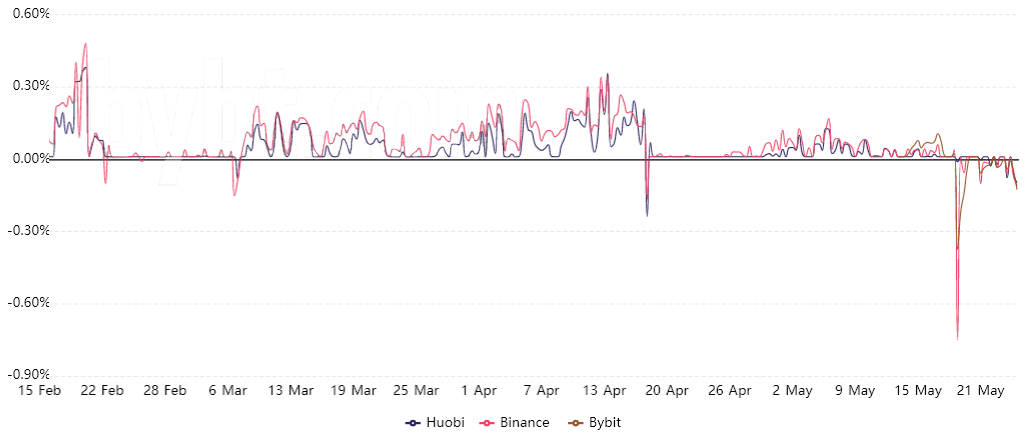

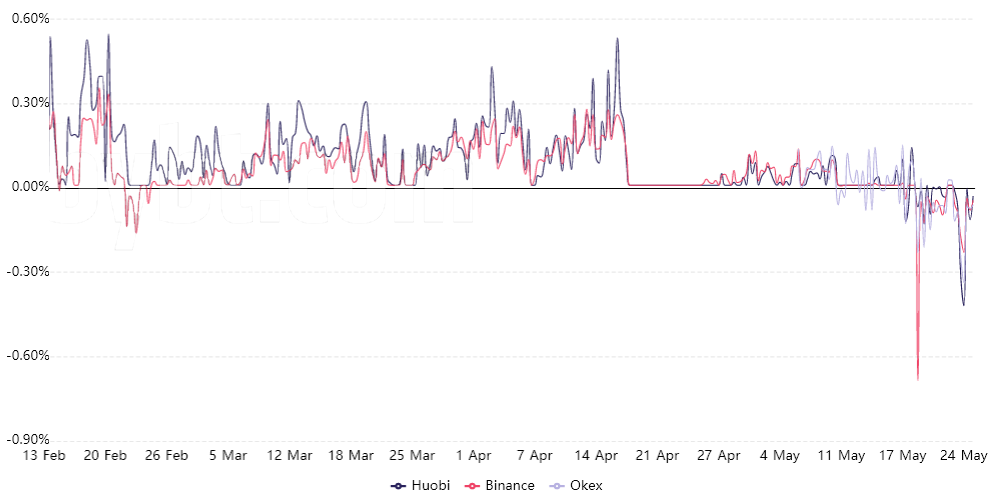

After a couple of days trying to stabilize, the perpetual contracts 8-hour funding rate now stands at negative 0.10%, equivalent to 2.1% per week. In this situation, shorts (sellers) pay the fee, creating an incentive for buyers.

A similar pattern emerged on Polygon (MATIC), which lost 62% on May 19 after marking a $2.70 all-time high on the previous day.

The opportunity is usually short-lived

A negative funding rate creates a safety net for buyers as there are incentives in place to gather strength and try to squeeze the short-sellers.

This is the reason why some analysts refer to the negative funding rate as a buy indicator. However, as soon as shorts close their positions, the situation tends to balance itself, and the funding rate is neutralized.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Leave A Comment