On Oct. 10, the development team for gaming project FinSoul carried out an alleged exit scam, siphoning away $1.6 million from investors through market manipulation, according to a recent report from blockchain security platform CertiK shared with Cointelegraph.

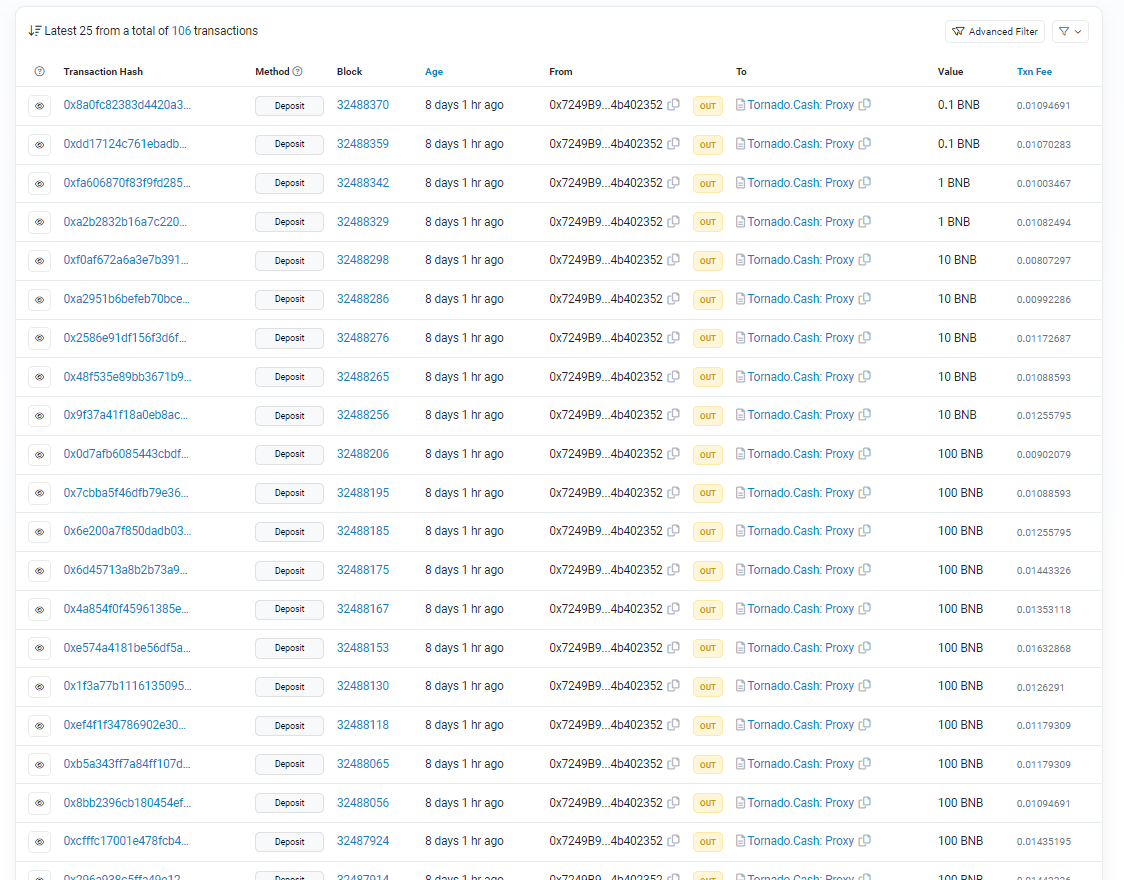

The FinSoul team allegedly hired paid actors to pretend to be its executives, then raised funds for the sole purpose of developing a gaming platform. However, instead of actually creating the platform, the FinSoul team allegedly transferred $1.6 million in bridged Tether (USDT) from investors to itself. Blockchain data indicates developers then laundered the funds through cryptocurrency mixer Tornado Cash. Surprisingly, this was not the first allegation of misconduct against FinSoul’s developers.

On May 23, decentralized finance (DeFi) project Fintoch published a press release claiming it had adopted “advanced technology to develop the FinSoul U.S.-based metaverse platform” and had gone “live.” The announcement stated that the company was using “advanced technologies such as Unreal Engine 5 and Cocos 2D” to develop “sandbox worlds, multiplayer sports, leisure experiences, player socializing, MMORPG” and other types of gaming content.

The same day, on-chain sleuth ZachXBT reported that the original Fintoch DeFi project had performed an exit scam. The team had seemingly stolen $31.6 million and bridged it to Tron blockchain in an attempt to launder the funds, ZachXBT claimed.

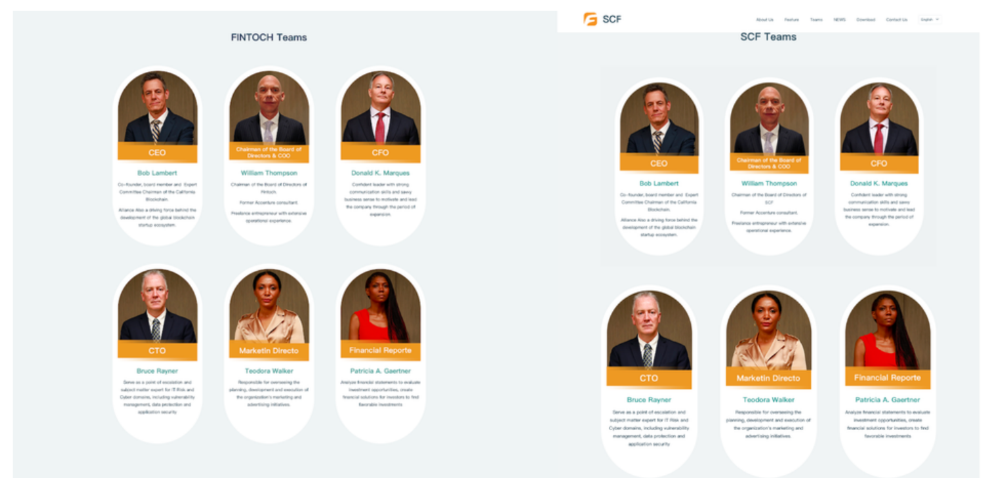

In response, CertiK claims that the team “rebranded” in August, changing its name and social channels. “Fintoch” became “Standard Cross Finance (SCF).” CertiK produced an image showing the key executives of both Fintoch and Standard Cross Finance, who appear to be identical.

The rebranded “Standard Cross Finance” team continued to promote FinSoul on YouTube and Telegram, the report states. Its marketing efforts included a video depicting an alleged “R&D Headquarters,” later revealed to be an office building on East Hamilton Avenue in Campbell, California. It also produced a video of an alleged promotional event in Vietnam.

The team page on the Fintoch website names “Bobby Lambert” as the CEO when in reality he does not exist and is a paid actor.

Previously both the Singapore Government and Morgan Stanley issued warnings about this investment scheme. pic.twitter.com/SLxvOCPj1s

— ZachXBT (@zachxbt) May 23, 2023

According to blockchain data, the project deployed its token contract to the BNB Smart Chain network on Oct. 10. At the time of deployment, 100 million FinSoul (FSL) tokens were minted and transferred into the deployer account. The deployer then sent 3 million FSL to other accounts through multiple transactions, leaving 97 million remaining in its possession. One of the transfers was for 210,000 FSL to an address that subsequently used the tokens to create a liquidity pool for FSL on PancakeSwap. From that point on, this pool was used by traders to buy and sell FSL.

Related: Cardano stablecoin project gambled away investors’ money before rug: Report

Data from DEX Screener shows that the price of FSL was initially set at $0.3911 per token on Oct. 10 at 6:30 am UTC. Over the next few hours, it rose to $17.5774, then retreated from this peak and came to stabilize at around $5 for the next few hours. Then, between 4:30 pm and 5:00 pm UTC, the price suddenly collapsed, falling from approximately $5 to near zero.

The story of FinSoul serves as a cautionary reminder that crypto investors should investigate new projects before committing funds to them. If CertiK’s report is to be believed, it implies that a scam team was able to trick investors, not just once, but twice, and is currently attempting a third fraud. Investors should remember to exercise due diligence before investing in projects that do not have a functioning blockchain project.

Related: Pond0x DEX claims $100M in trading volume as critics allege it’s a scam

“Rug pulls,” or exit scams, have posed a continuing problem in the world of decentralized finance. Arbitrum-based protocol Xirtam allegedly stole over $3 million from investors using a token sale over the summer. In this instance, Binance managed to freeze the funds and return them to users via a smart contract beginning on Sept. 6.

However, most rug-pull victims are not so lucky. In June, DeFi project Chibi Finance removed over $1 million of its users’ funds through a “panic” function, and these funds have yet to be recovered. In 2021, the PopcornSwap exit scam resulted in over $11 million in losses to investors and led to criticism of the BNB Chain development team that still continues to this day.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

Leave A Comment