Update On ECB Bond Buying

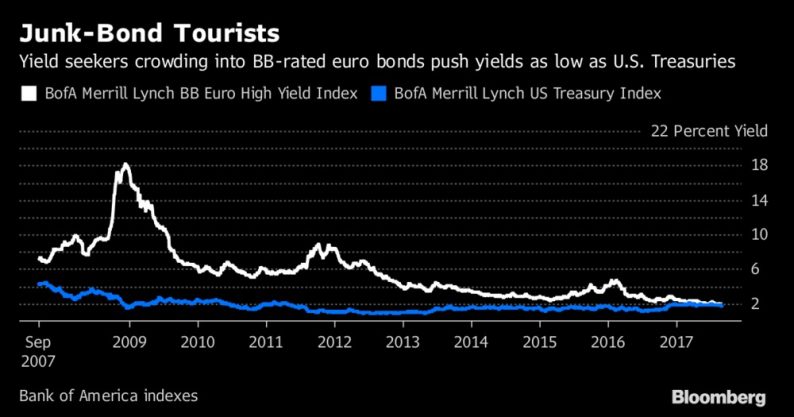

A new milestone is about to be reached in the ECB’s bond buying program. There have now been 998 bonds bought by the ECB. You can see the effects in the chart below. The BB rated euro high yield bond index is now at almost the same yield as the U.S. treasuries. That means there is no risk premium for junk debt. The unthinkable could happen in the next few weeks which would be junk bonds going below treasuries. Normally, investors would assign risk to lower grade bonds because they have default risk. We’re in a situation where defaults are low which shrinks the risk premium. The ECB’s buying puts it over the edge. This buying also keeps a lid on U.S. treasuries as investors are surprisingly seeking yield in what is considered to be the least risky bonds in the world.

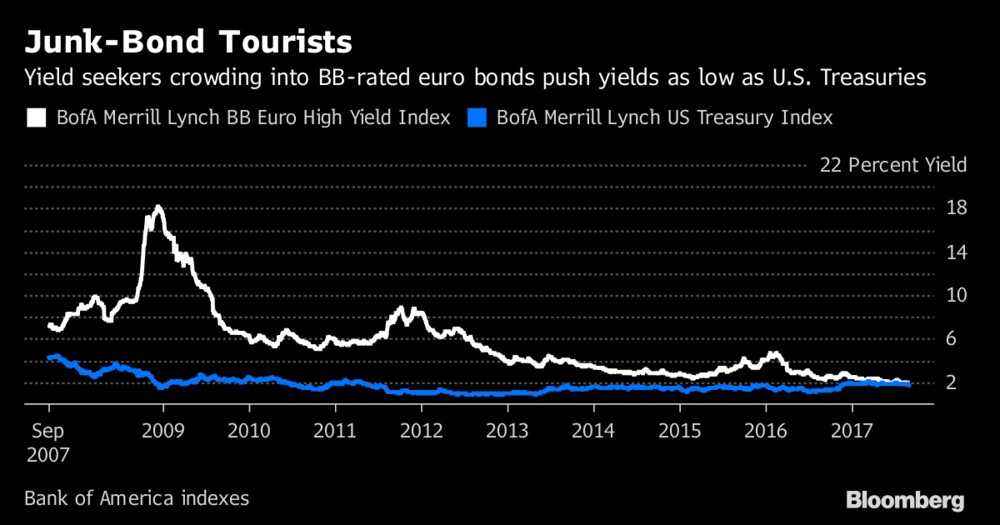

The chart below gives a close in look at the effect the ECB bond buying has had on the spread between high yield and high grade debt. It’s not surprising that $10s of billions of bond buying has lowered junk yields. The spread has fallen by about 1.5% in the past 12 months. If this pace were to keep up in the next 12 months, there would be no spread at all.

Earnings Looking Vulnerable

Now let’s look at the S&P 500 earnings to get a better picture on how stocks will do in 2018. The chart below shows the EBIT, revenues, net income, and EBITDA excluding energy and financials on a year over year basis. It makes the 2015-2016 earnings recession look less bad when you exclude energy since energy was responsible for the weakness because oil prices cratered. The latest decline might be muted in this chart because it excludes financials which will be seeing weakness and have been seeing some weakness already because of the flattening of the yield curve. Even though the big 5 technology firms don’t have an above average influence on the indices, they still have a huge impact on these earnings growth results. Technology is also one of the cheapest sectors compared to its historical levels. Excluding technology, the stock market is near the most overvalued level ever. Looking at technology alone, the sector is near the historical average value. Therefore, the big tech names may not have an unusual impact on the market, but they have an unusual impact on valuations.

Related Posts

E

UK Readers: Last Chance For A Guaranteed Inflation-Beating Investment

E

UK Readers: Last Chance For A Guaranteed Inflation-Beating Investment- Dollar Surges, But Recent Gains Seem Exaggerated

- EUR/USD Begins Test Of Key Resistance, USD Bounces From Monthly Lows

Some Caveats On The Retail Recession

Some Caveats On The Retail Recession Global Stocks Mixed, Futures Rise As Oil Stumbles After OPEC Fails To Agree On Supply Cuts

Global Stocks Mixed, Futures Rise As Oil Stumbles After OPEC Fails To Agree On Supply Cuts- GOLD Sees Second Week Of Declines

Leave A Comment