Shutterstock photo

Years of low interest rates and minimal inflation have resulted in many ETF investors adopting these investments as surrogates for more conservative options. Furthermore, a prolonged period of relatively low volatility may have lulled these same participants into a false sense of security.

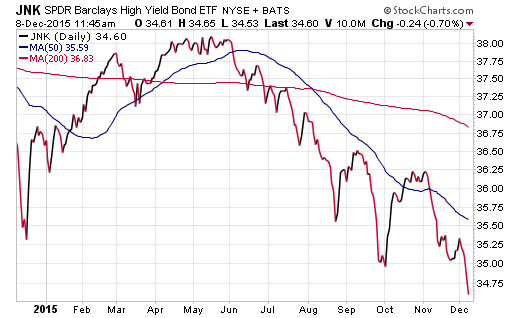

The lesson that many are learning is that a reach for yield also comes with an associated greater risk of volatility in price.That volatility may be finally starting to rear its ugly head, as two heavily owned high yield funds have fallen precipitously in recent months.

Junk Bonds

The SPDR Barclays High Yield Bond ETF (JNK) tracks an index of nearly 800 corporate bonds in the U.S. with below investment grade credit ratings.These fixed-income securities are commonly referred to as “junk bonds” because of the issuers’ relatively precarious financial situation. Investors are then compensated for the additional risk by receiving a much higher coupon payment (or yield) than a Treasury or investment grade corporate bond.

The current 30-day SEC yield on JNK is 7.23% and has been rising steadily as its price has dropped. By contrast, a 10-Year Treasury Note currently yields 2.23%.That puts the spread between a risk-free Treasury bond and the high yield bond index at nearly 5% (or 500 basis points).

Since peaking in May, JNK has fallen more than 9% and continues to illustrate tightening risk behavior in the credit markets.

JNK has $11 billion in total assets and charges an expense ratio of 0.40%. According to data from ETF.com, this fund has actually attracted $2.4 billion in additional net assets this year. This is likely the result of value-conscious income investors taking advantage of depressed prices to increase their portfolio yield.

Nevertheless, as the chart above indicates, this index has yet to see signs that a reliable low has been put in place and the downtrend has been accelerating rapidly in recent months. Much of this misery has been blamed on falling energy prices, which make up a significant portion of the U.S. high yield debt market. A recent Charles Schwab research note opined that weakening commodity prices were to blame for higher volatility and an overall increase in distressed debt.

Leave A Comment