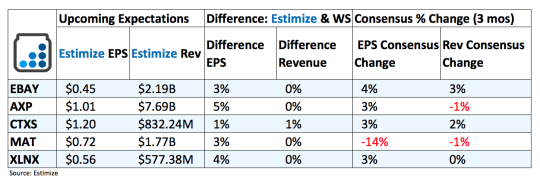

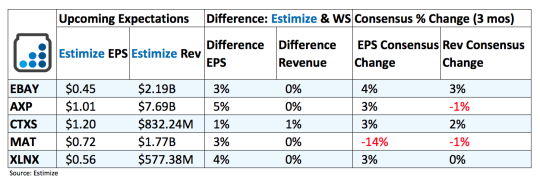

eBay (EBAY): eBay’s dominance in the late 90’s and early 2000’s has largely disappeared thanks to the emergence of Amazon (AMZN) and other online retailers. This had resulted in a string of dismal earnings and a sell off in the stock. Until recently, its prospects appeared limited. Its recent departure from PayPal put a thorn in the side of investors as the online payment platform continued to succeed. Now after a few stronger than expected quarters under its belt, analysts are optimistic that this upcoming report will be strong. The company has taken several initiatives to improve user engagement and thereby revenue. They include using technological applications to more accurately target customers, shifting towards a fixed pricing model, as opposed to its legacy auction business, and revamping policies to reward those who provide quality services. Additionally, the acquisition of Ticketbis will help expand its Stubhub brand beyond North American markets.

American Express (AXP): Shareholders will get their first look at American Express without Costco in the upcoming quarterly report. This marks the first period that the AMEX won’t receive any kickbacks from the Costco partnership after the wholesaler parted ways in favor of Visa. The combination of soft consumer spending and the lost partnership have analysts cautious heading into this report. The Estimize community is calling for an 18% drop on the bottom line and 6% on the top. This is a significant blemish on its track record which included flat revenue and robust EPS growth.

Citrix Systems (CTXS): Its impressive product portfolio of desktop virtualization, networking and cloud computing technologies have driven robust growth in recent quarters. In fact, the company has consecutively beat on the top and bottom line in each of the past 4 quarters. Analysts are optimistic that tomorrow’s report can continue this winning streak, but it won’t be that simple. Despite consistently beating estimates, growth has seen a marked deceleration over the last 4 quarters, which has also translated to the stock. When compared to some of its competitors, the stock’s 12.5% gains this year look unimpressive. Meanwhile, increasing competition and ongoing pressure from foreign exchange volatility could drag growth down even further.

Leave A Comment