We evaluated 18 different companies this week to determine whether they are suitable for Defensive Investors, those unwilling to do substantial research, or Enterprising Investors, those who are willing to do such research. We also put each company through the ModernGraham valuation model based on Benjamin Graham’s value investing formulas in order to determine an intrinsic value for each. Out of those 18 companies, only 9 were found to be undervalued or fairly valued and suitable for either Defensive or Enterprising Investors.

The Elite

The following companies were found to be suitable for either the Defensive Investor or Enterprising Investor and undervalued:

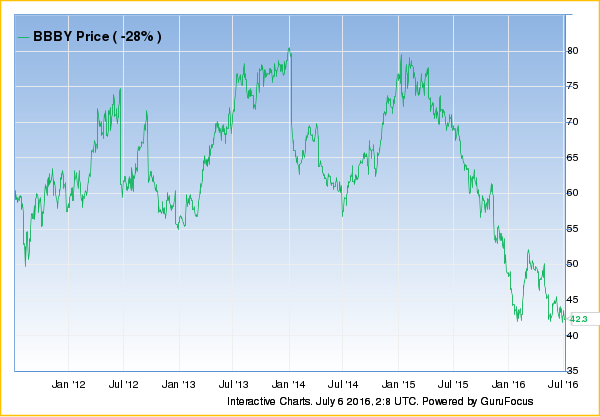

Bed Bath & Beyond Inc. (BBBY)

Bed Bath & Beyond Inc. qualifies for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the low current ratio and lack of dividends. The Enterprising Investor is only initially concerned by the lack of dividends. As a result, all Enterprising Investors following the ModernGraham approach based on Benjamin Graham’s methods should feel comfortable proceeding with further research into the company.

As for a valuation, the company appears to be undervalued after growing its EPSmg (normalized earnings) from $2.99 in 2012 to an estimated $4.88 for 2015. This level of demonstrated earnings growth outpaces the market’s implied estimate of 1.29% annual earnings growth over the next 7-10 years.As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price.

KeyCorp (KEY)

KeyCorp qualifies for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability over the last ten years. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach based on Benjamin Graham’s methods should feel comfortable proceeding with further research into the company.

As for a valuation, the company appears to be undervalued after growing its EPSmg (normalized earnings) from a loss of $0.35 in 2011 to an estimated gain of $0.98 for 2015. This level of demonstrated earnings growth outpaces the market’s implied estimate of 2.43% annual earnings growth over the next 7-10 years.As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price.

Related Posts

GBP/USD Analysis: Focus Shifts Cautiously To US Data

GBP/USD Analysis: Focus Shifts Cautiously To US Data Why The “Sound Money” Components Of Popular Economic Freedom Indexes Should Be Used With Caution

Why The “Sound Money” Components Of Popular Economic Freedom Indexes Should Be Used With Caution- EU Bullet Report – Gold Posts 1 Year High, NFP Day Is Here

Dividend Income Update April 2017

Dividend Income Update April 2017 Friday Charts: Apple’s Death Curse, Tax Reform And Twitter Woes

Friday Charts: Apple’s Death Curse, Tax Reform And Twitter Woes Creating a budget for your startup

Creating a budget for your startup

Leave A Comment