Public opinion about the government is pretty darn bad.

The president’s approval rating is at 39%. Congress has an even lower approval rating of just 15%. I think the stomach flu has a higher approval rating than Congress does these days.

And after years of listening to Republicans complain about the Democrats’ spendthrift ways and Democrats pretending that the federal debt is no big deal, the roles have reversed. Republicans passed a tax package that will add $1 trillion in debt and suddenly the Democrats care about how much money is being spent.

What a bunch of hypocrites!

The federal government is a hot mess. So I wasn’t surprised to see that a government-related real estate investment trust (REIT) was having more difficulty than it has had in the past.

Government Properties Income Trust (Nasdaq: GOV) owns 108 properties in 30 states (including Washington, D.C.) that are primarily leased to the government.

It pays a fat 12.5% yield, which is why it’s so attractive to income investors.

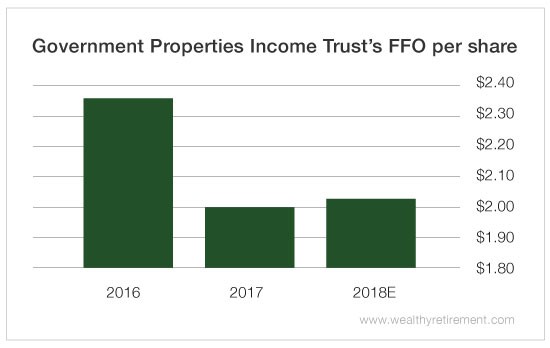

Where’s the Growth?

In 2017, Government Properties Income Trust generated $2 per share in funds from operations (FFO), a measure of cash flow used by REITs.

It paid out $1.72 per share in dividends.

However, last year’s $2 was significantly lower than 2016’s FFO total of $2.35 per share.

This year, FFO is forecast to inch higher by only 1% to $2.02.

The company has paid a dividend since 2009 with no cuts. The quarterly dividend has been $0.43 per share since October 2012.

However, declining FFO is a concern. Even though it currently covers the dividend, should it continue to slide, the dividend could be in jeopardy.

That’s the situation we’re currently in with Government Properties Income Trust. It can cover the dividend for now, but unless FFO turns around, it may not be able to in the future.

Like our federal government, Government Properties Income Trust is headed the wrong way.

Related Posts

PPI Unexpectedly Declines Second Month; Another Big Decline Likely Next Month

PPI Unexpectedly Declines Second Month; Another Big Decline Likely Next Month Target Chart Is Right On The Mark

Target Chart Is Right On The Mark ECB January Meeting Minutes: A Turnaround From December

ECB January Meeting Minutes: A Turnaround From December China Unleashes New Crypto Crackdown After Discovering Sneaky Hobbitses Still Trading

China Unleashes New Crypto Crackdown After Discovering Sneaky Hobbitses Still Trading Treasury Yields Fall In The New Year, Reflecting Macro Worry

Treasury Yields Fall In The New Year, Reflecting Macro Worry Rail Week Ending 10 October 2015: Recession In Rail Continues

Rail Week Ending 10 October 2015: Recession In Rail Continues

Leave A Comment