There’s been a lot of fretting and sweating over oil prices lately. Concern about the petroleum sector heightened even more as Hurricane Harvey bore down on oil rigs and refineries in the Gulf Coast region.

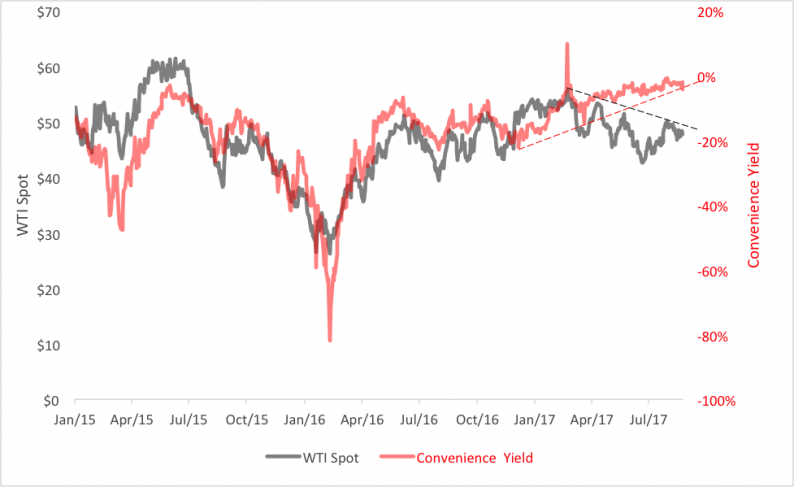

The spot price for a barrel of West Texas Intermediate (WTI) crude has been fibrillating in the $47 – $49 range this month following a dip below $43 in the early summer. Despite the gain, oil has more work to do to regain its previous bullish momentum. Below you can see spot oil’s history over the last two years. WTI is the black line. The red line, which has pretty much tracked oil’s price through March, is crude’s three-month annualized convenience yield.

What’s a convenience yield? It’s the benefit – or cost – of holding physical oil versus owning a derivative like oil futures.

Holding oil as inventory is “convenient” for a refiner when doing so ensures the continuity of distillate (e.g., gasoline and fuel oil) production. When oil is plentiful, refiners can buy oil at will to meet their production needs. Having oil on hand – in storage – pays off when demand for oil heightens and spot prices rise. The convenience yield represents the gross return implied for carrying an oil inventory – essentially, the profit that could be obtained by selling excess crude at market prices.

As you can see in the chart above, crude oil’s convenience yield has been mostly negative since 2015, reflecting a glut in the market. But look at this year’s trend. It’s been upward. The yield is now very close to zero (at last look, it was -4.16 percent). The yield’s still negative, though far less so than at the beginning of the year.

Look again at the chart and you’ll note that oil’s price trend has been diverging from that of the convenience yield. The yield hasn’t been closely tracking oil’s cost as it has in the past. In other words, the convenience yield is behaving as if oil’s supply is tightening.

Leave A Comment