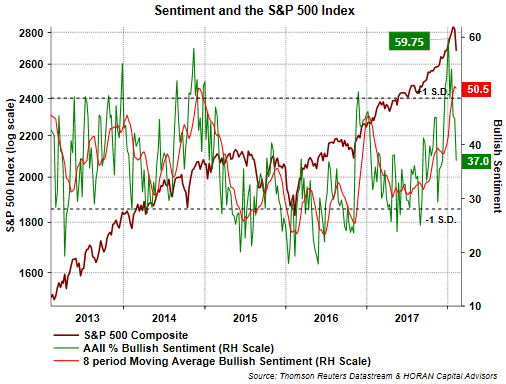

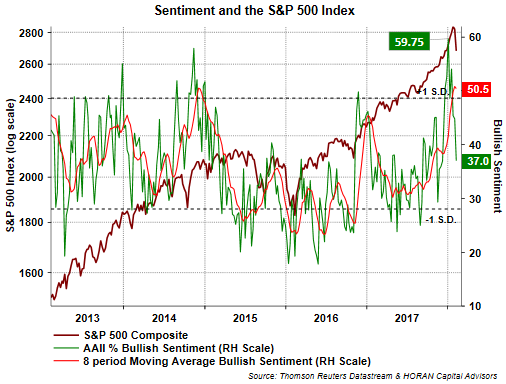

I have often written that sentiment measures are most valuable at their extremes. Also, they tend to be most representative of potential market turning points when the extreme is at the bearish end of the spectrum. However, in hindsight, it appears recent excessive bullishness for individual investors and institutional investors indicated a cautionary equity market outlook would have been profitable.

The first chart below represents individual investors’ bullish sentiment responses as reported weekly by The American Association of Individual Investors. On January 4 of this year bullish sentiment spiked to near 60% and represents a high level for this reading. About a month later, the 8-period moving average reached near 51%, also a high level for the 8-period average, although the average has exceed 60% in the past.

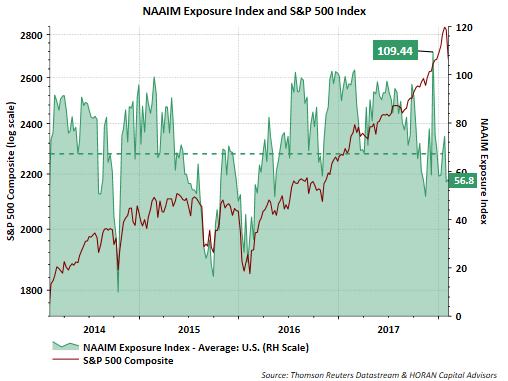

Also hitting a near term high of 109.4 was the NAAIM Exposure Index Index on December 13, 2017. Subsequent to the institutional manager exposure index high, it has since declined to 56.8% this week.

On the heels of these high readings, the equity markets have reversed course and are currently experiencing a more volatile period, which is a more normal function for the markets. No one likes giving back gains for sure, but the below chart shows equity returns remain strong over the course of the last five years. The chart’s absence of percentage labels in 2017 is due to virtually no volatility in the index’s return. Since February of 2016, the S&P 500 Index has mostly moved in one direction and that is higher.

As we noted in our commentary a few days ago, the market’s return to volatility is based on an economic environment that is accelerating at a pace faster than many strategists expected. Importantly, a recession does not seem like a near term outcome; but some stability in interest rates may be necessary to reduce the some of the equity market’s recent volatility.

Related Posts

The future economy: Anticipating the central role of crypto payments in financial transactions

The future economy: Anticipating the central role of crypto payments in financial transactions Capital Flight Intensifies In Italy And Spain; Curiously, Money Flows Into French Banks

Capital Flight Intensifies In Italy And Spain; Curiously, Money Flows Into French Banks Price analysis 8/6: BTC, ETH, BNB, ADA, XRP, DOGE, DOT, UNI, BCH, LINK

Price analysis 8/6: BTC, ETH, BNB, ADA, XRP, DOGE, DOT, UNI, BCH, LINK Investors Fret As Politics Override Bank Earnings

Investors Fret As Politics Override Bank Earnings Philly Fed Back In Contraction, Index Below Any Economist’s Guess

Philly Fed Back In Contraction, Index Below Any Economist’s Guess US Durable Goods Orders Falls By 1.2% – USD Follows

US Durable Goods Orders Falls By 1.2% – USD Follows

Leave A Comment