Image Source: Pixabay

Image Source: Pixabay

Several investment professionals that I hold in high regard have made the statement that holding cash has optionality—in that it gives the opportunity to invest later at a lower price level. I would dispute the word option but agree that a tactical under-allocation to return-seeking assets can reduce risk in the near term much like a put option does. It is not a free option. It involves an opportunity cost of missing out on an equity market rally if the timing is wrong (rather than an upfront premium payment of a true option). I do stress the word tactical in this justification of holding cash—over the long term, cash is expected to underperform equities by approximately 5% (the equity risk premium).

Why is it less painful to hold cash now?

Many of our public fund pension clients have a stated return expectation of 7% or more, and that assumption drives the calculation of funded status. In fact, most institutional clients have long-term return expectations, even if it is not quite as prominent a measure as for a public fund. Without a starting assumption of return needs, it is nearly impossible to arrive at a suitable asset allocation.Since the start of 1998 (anything but a normal period to those of us that lived it, but it is the span of my financial career), short-term rates have averaged 2.01%. That average is skewed by nearly a decade of zero interest rate policy (ZIRP).  R-star (R*) is what economists call the neutral short-term rate, it is a conceptual rate that can be estimated but not directly observed. It is not restrictive, it is not accommodative, it is just right—somewhat like Baby Bear’s bed that Goldilocks found irresistible. Due to demographics and increased federal debt levels among other things, it is lower now than it was in 1998, as is the economic potential growth in our maturing economy. That said, Russell Investments’ estimations of R* is in the range of 2.5-3%. Right now, we are firmly in Papa Bear’s bed—5.5% is way too hard for Goldilocks.With high short-term rates, we have opportunities to capture a considerable portion of the total portfolio’s target return with money market funds or Treasury bills (T-Bills) maturing within 1 year. While we have a slight return shortfall of about 1.5% on the cash allocation (7% expected return minus 5.5% on 1-year T-Bills), that is the smallest shortfall since 2007. This is a manageable return shortfall given that 5.5% can be obtained over the next year with near certainty. This was not the case during ZIRP when the risk premia had to deliver 7% all by itself.

R-star (R*) is what economists call the neutral short-term rate, it is a conceptual rate that can be estimated but not directly observed. It is not restrictive, it is not accommodative, it is just right—somewhat like Baby Bear’s bed that Goldilocks found irresistible. Due to demographics and increased federal debt levels among other things, it is lower now than it was in 1998, as is the economic potential growth in our maturing economy. That said, Russell Investments’ estimations of R* is in the range of 2.5-3%. Right now, we are firmly in Papa Bear’s bed—5.5% is way too hard for Goldilocks.With high short-term rates, we have opportunities to capture a considerable portion of the total portfolio’s target return with money market funds or Treasury bills (T-Bills) maturing within 1 year. While we have a slight return shortfall of about 1.5% on the cash allocation (7% expected return minus 5.5% on 1-year T-Bills), that is the smallest shortfall since 2007. This is a manageable return shortfall given that 5.5% can be obtained over the next year with near certainty. This was not the case during ZIRP when the risk premia had to deliver 7% all by itself.

Choosing the appropriate maturity in the liquidity pool

With current cash rates much higher than both the backward-looking average over the past 25 years or a forward-looking estimate of R*, the Fed will enter a rate-cutting cycle at some point. The inverted Treasury yield curve is telling us this is the case. As a result, there is reinvestment risk when a T-Bill matures in a year as rates may be lower at that point. As a result, some investors choose to extend the term of these exposures out a little further, even though the annualized yield can be lower. Doing so is locking in current forward expectations of short-term rates in the future. If the Fed eventually needs to cut more than expected—a 2-year term would outperform repurchasing 1-year T-Bills each year. Contrarily, staying in higher yielding 1-year T-Bills would outperform if the Fed can maintain its higher-for-longer stance without breaking anything.

How do your peers handle this?

Most of our institutional investor don’t have a strategic allocation to cash, so any cash they hold is a tactical underweight to return seeking assets. Holding cash over the long-term causes a drag on total portfolio returns versus expectation, but in shorter periods, it is possible for cash to hold its value when markets decline. When it comes time to close that tactical underweight to return-seeking assets, an exposure that held its value can buy more risky assets after a market correction. Sounds easy right? Well, buying low and selling high requires a level of hindsight this is not possible in real time. For those that believe in a cash allocation currently, there are tools and rules that can help manage it without causing undue performance damage from being out of markets.

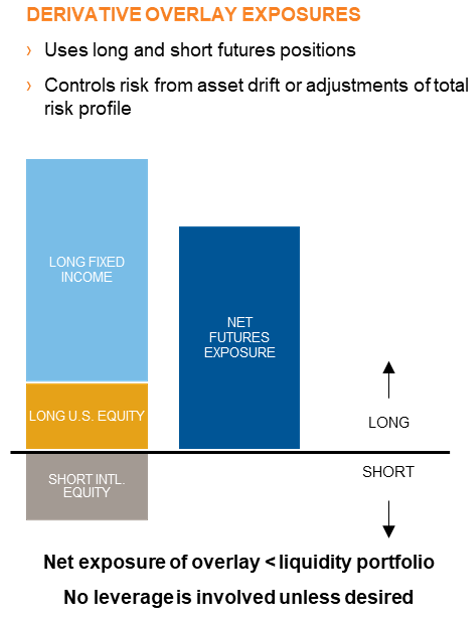

Tools

Rules

The bottom line

It is often said that there are no bad investment positions, only bad timing. Holding tactical cash is less painful now for the reasons outlined, but it is not a long-term strategy for beating the investment policy. That said, there are considerable corporate and real estate debt rollover needs in the coming 3-5 years, and at some point, these refinancing needs could lead to increased systemic stress in lending markets. Only time will tell if there if there is enough dislocation in the markets to create notable bargains in select return-seeking assets.More By This Author:How Could An Energy Transition Impact Global Markets And Economies?

Why Are U.S. Treasury Yields Soaring?

Expanding (Investment) Horizons: The Case For Investing Globally

Leave A Comment