At year end I posted a rant about the “Brobdingnagian” bubble embedded in Amazon’s (AMZN) market cap. On December 29th it was valued at $325 billion and had gained $180 billion or 55% of that towering figure in just the previous 12 months.

Self-evidently this was a flashing red warning signal that the end of the third great central bank fueled financial bubble of his century was near. AMZN and its three other FANG amigos had accounted for a $530 billion gain in market cap while the other 496 stocks in the S&P 500 had declined by even larger amount.

That is, the apparently flat S&P 500 index of 2015 was hiding an incipient bear—owing to a market narrowing action like none before. Compared to the Fabulous FANGs (Facebook (FB), Amazon (AMZN), Netflix (NFLX) and Google (GOOG) ), the early 1970s Nifty Fifty of stock market lore paled into insignificance.

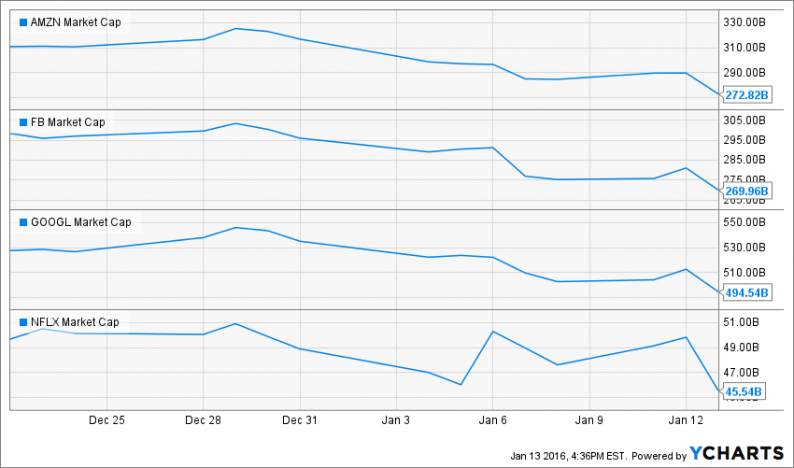

After the worst start to a year in history, some of the air has now been let out of the bubble. Amazon’s market cap is now down by $53 billion or 16% and the story has been roughly the same for the rest of the FANGs.

After Wednesday’s plunge, Goggle is now also down by $52 billion or 10%; Facebook is lower by $33 billion or 10%; and Netflix is off by $6 billion or 11%. In all, the FANGs have given back in eight trading days about $144 billion or 28% of their madcap gains during 2015.

AMZN Market Cap data by YCharts

Call that a start, but in the great scheme of things it doesn’t amount to much. Consider the case of Amazon. Its PE multiple on LTM net income of $328 million has dropped from 985X all the way to…….well, 829X!

Likewise, it’s now valued at 97X its $2.8 billion of LTM free cash flow compared to 117X at year end.

In the same vein, Facebook’s LTM multiple on net income has dropped from108X to 96X.

So the reason to revisit the FANGs, and the Amazon bubble in particular, is not because their market caps have come down to earth; it’s because once you get inside, another characteristic of late stage bubbles comes lurking front and center.

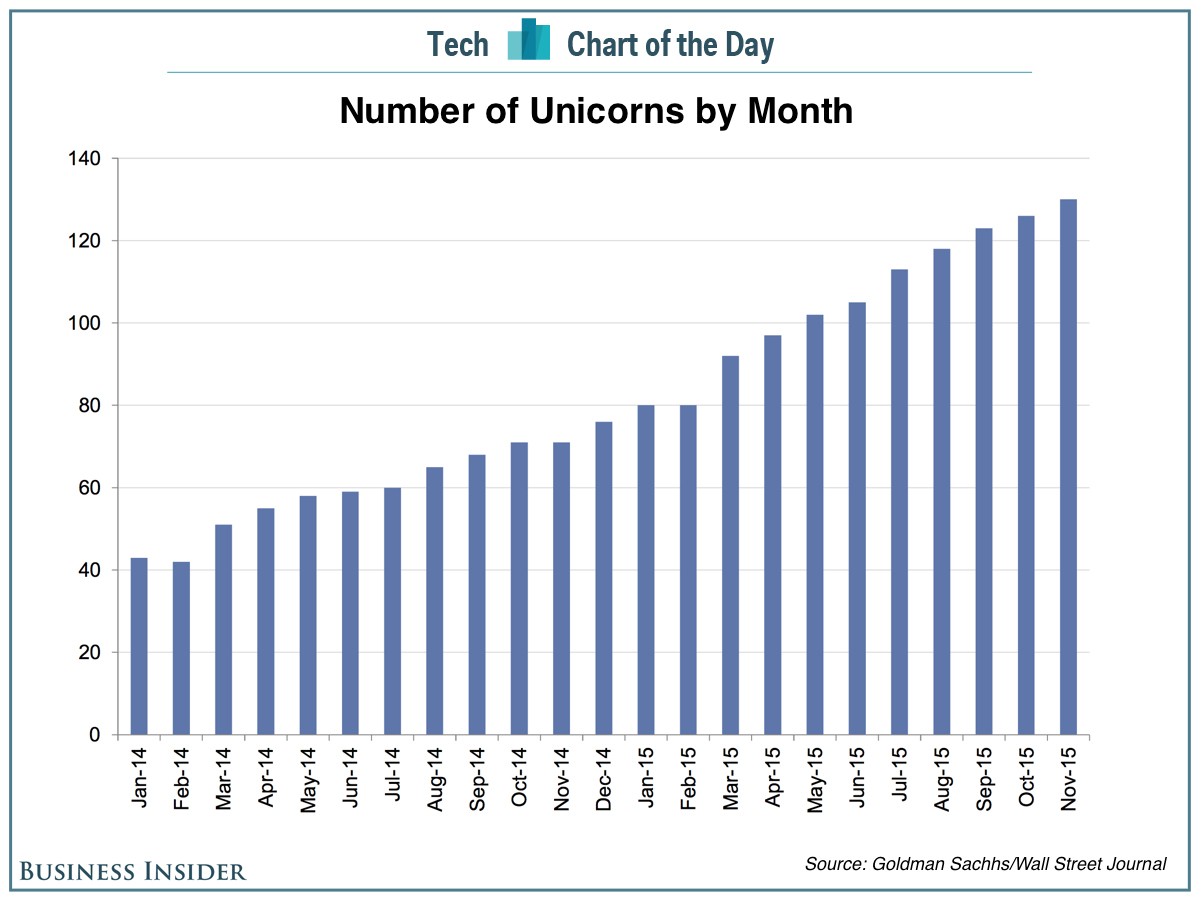

Namely, the tendency for the accounting income of momo tech stocks at bubble tops to be bloated with non-sustainable revenues and profits from Silicon Valley burn babies.

This time we call them Unicorns, and at last count there were upwards of 150 pre-IPO start-ups valued at $1 billion or more. At year-end, estimated “valuation” of the group stood at more than $500 billion. And, as befitting the blow-off stages of a financial bubble, they had been growing like topsy in the last 24 months:

I was reminded of this possibility by an excellent post by Dave Kranzler at Investment Research Dynamics. In a piece called “AMAZON dot CON” he took me to task for being too kind to Jeff Bezos’s ponzi accounting.

Among other things, Kranzler went all the way back to the beginning and offered an even more dramatic juxtaposition of the bubble in the stock versus the reality on the ground:

Throughout its 25-year history as a public stock, AMZN has delivered a cumulative total of $1.9 billion in net income to shareholders. Jeff Bezos made $16 billion on AMZN stock in 2014.

That’s right. So if AMAZN gained $180 billion in market cap during 2015 alone—or 95 times its cumulative earnings during the last quarter century—then either some dramatic acceleration of earnings capacity occurred in 2015 or, as Kranzler put it—

The more time I spend researching and observing AMZN, the more I’m convinced that it’s the biggest Ponzi scheme in the history of the stock market.

And on that score Kranzler hit the nail on the head. The ostensible reason that AMZN’s stock price soared in 2015 was due to the purported “scorching” performance of its cloud services division called AWS. I thought I had done a pretty good job of debunking that, but this turns out to be a case of the late night TV ad man—but wait, there’s more!

It turns out that the surging revenues of AWS may be due to the fact that AMZN is having unicorns for breakfast. But to establish the context, here is what we said at year end:

But this year’s $180 billion market cap eruption has absolutely nothing to do with its newly developed capacity for same day delivery of healthy treats for your pooch. This most recent rip was all about the purportedly “scorching” performance of its AWS division—that is, Amazon’s totally unrelated business as a vendor of cloud computing services.

Indeed, CNBC recently gave air time to one of the most rabid analyst on the block, and this particular stock peddler from UBS left nothing to the imagination. Never mind whether anything emanating from that serial swindler and confessed criminal organization can be taken seriously, here’s what the man said.

AWS is technology’s second coming and is worth $110 billion. We know that because AMZN has recently been thoughtful enough to break out its financials.

They show AWS had sales of $2.1 billion in the September quarter and revenues of $6.9 billion on an LTM basis. So that puts its cloud computing business’ value at 16X sales. No sweat!

Moreover, this means that the balance of the company—that is, its core E-commerce business—is “only” valued at an apparently much more reasonable $215 billion. And by golly, said the UBS man, that’s just 2.3X sales. So what’s not to like?

Well, hold it right there. Someone forgot to do the math in all the excitement about AWS. Yes, the company’s release did show that AWS posted $1.42 billion of operating income or about 20% of sales during the September LTM period.

But consolidated operating income during the quarter was only $1.72 billion, meaning that by the lights of subtraction, Jeff Bezos’ great empire of E-commerce earned the microscopic sum of $300 million in operating income during its most recent year.

By the same magic of subtraction we can see that AMZN’s E-commerce business generated $94 billion of sales. This means that its operating margin was exactly 32 basis points.

That’s right—after 25 years of crushing it on the E-commerce front, Amazon’s core business operating margin is truly a rounding error.

Related Posts

A Weekly Technical Perspective On Gold, Copper, Crude

A Weekly Technical Perspective On Gold, Copper, Crude- E

Forex Analysis Of EUR/USD For Friday, August 10

- Terra injects 450M UST into Anchor reserve days before protocol depletion

- Medical Suppliers Slide As Amazon Looms, Walgreens Pursues AmerisourceBergen

Understanding 2017 Corporate Tax Reform Issues

Understanding 2017 Corporate Tax Reform Issues- What If The Fed Doesn’t Raise Rates?

Leave A Comment