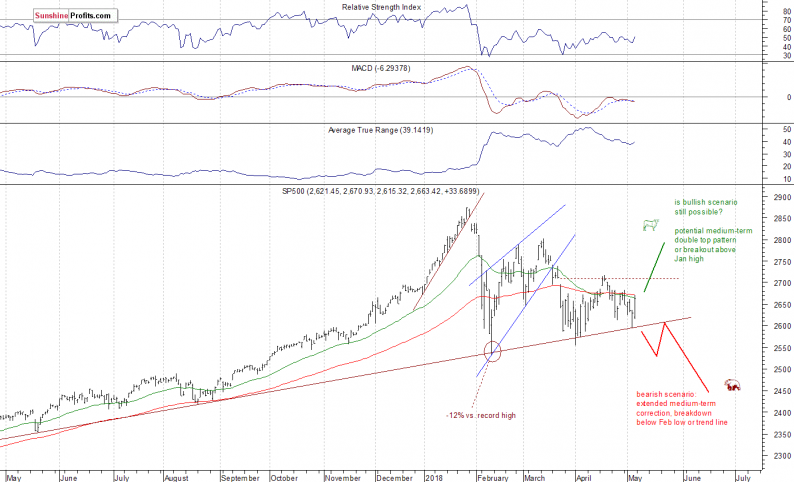

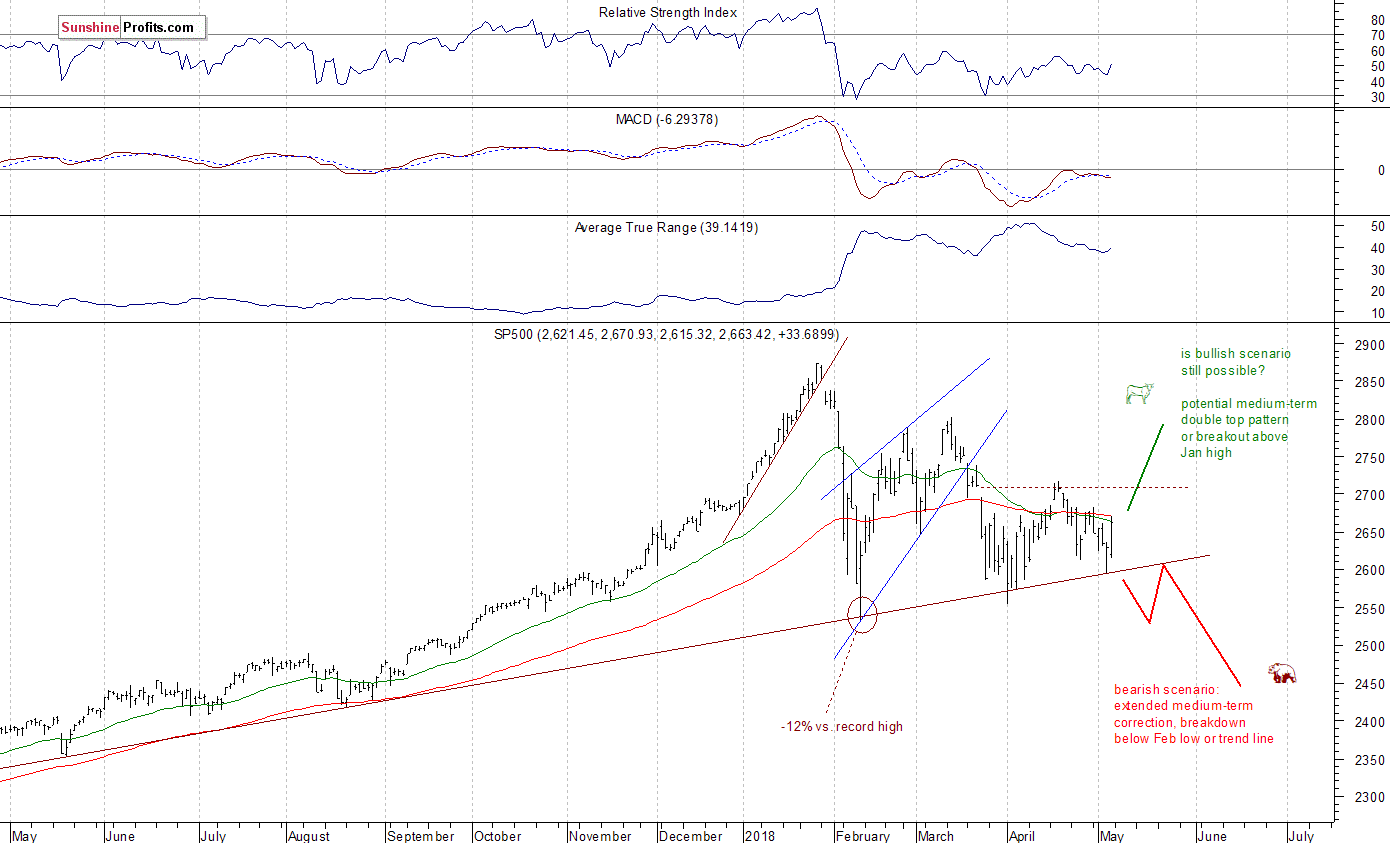

The U.S. stock market indexes gained between 1.3% and 1.7% on Friday, retracing most of their last week’s move down, as investors reacted to monthly jobs data release. The S&P 500 index got closer to its Monday’s local high, and it currently trades 7.3% below January 26 record high of 2,872.87. The Dow Jones Industrial Average gained 1.4%, and the technology Nasdaq Composite gained 1.7% on Friday, as Apple’s stock price led the technology sector higher.

The nearest important level of resistance of the S&P 500 index is now at around 2,670, marked by Friday’s daily high. The next resistance level is at 2,685-2,710, marked by previous local high and March 22 daily gap down of 2,695.68-2,709.79. On the other hand, support level is at 2,595-2,615, marked by recent fluctuations and an over year-long medium-term upward trend line.

The broad stock market continues its medium-term consolidation following late January – early February sell-off. There are still two possible medium-term scenarios – bearish that will lead us below February low following trend line breakdown, and the bullish one in a form of medium-term double top pattern or breakout towards 3,000 mark. There is also a chance that the market will just go sideways for some time, and that would be positive for bulls in the long run (some kind of an extended flat correction):

Positive Expectations

The index futures contracts trade 0.3-0.5% higher vs. their Friday’s closing prices, so expectations before the opening of today’s trading session are positive. The main European stock market indexes have gained 0.1-0.8% so far. There will be no new important economic data announcements. However, investors will wait for more quarterly earnings releases. Friday’s uptrend may extend a little, but we may see more uncertainty, as the broad stock market gets closer to previous local highs. There have been no confirmed negative signals so far.

Related Posts

Existing Home Sales Drop Year-Over-Year For 2nd Straight Month – First Time Since 2014

Existing Home Sales Drop Year-Over-Year For 2nd Straight Month – First Time Since 2014 Not Preventing Market Losses? You Better Start Now

Not Preventing Market Losses? You Better Start Now Nigeria’s Manufacturing Sector Remains Steady

Nigeria’s Manufacturing Sector Remains Steady S&P 500 And Nasdaq 100 Forecast – Monday, April 16

S&P 500 And Nasdaq 100 Forecast – Monday, April 16 USDJPY: Resumes Uptrend, Eyes The 112.61 Resistance Zone

USDJPY: Resumes Uptrend, Eyes The 112.61 Resistance Zone EURJPY Elliott Wave View: Pullback In Progress

EURJPY Elliott Wave View: Pullback In Progress

Leave A Comment