Cleveland Federal Reserve President Loretta Mester on Monday said that the recent flattening of the yield curve isn’t a sign that the US economy is weakening. Her comment follows a similar observation by Fed Chairman Jerome Powell, who suggested last week that low inflation in recent years has reduced the value of monitoring recession risk based on differences between long and short Treasury yields.

Mester advised that there is “no evidence” for thinking that a flatter curve signals a weaker economy at this time, Reuters reported. She added that “structural factors,” such as bond-buying by central banks, are compressing the curve.

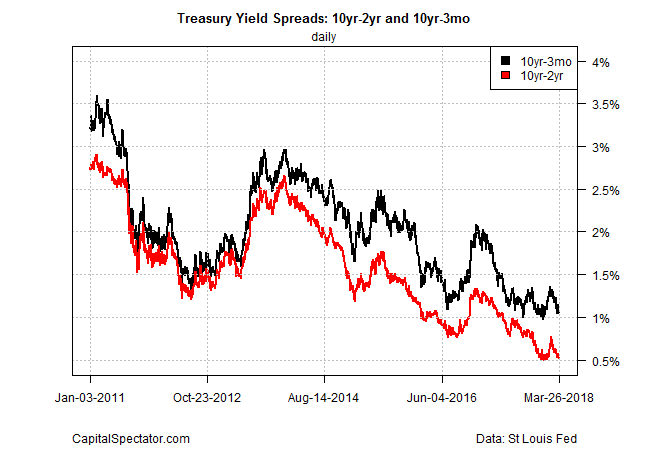

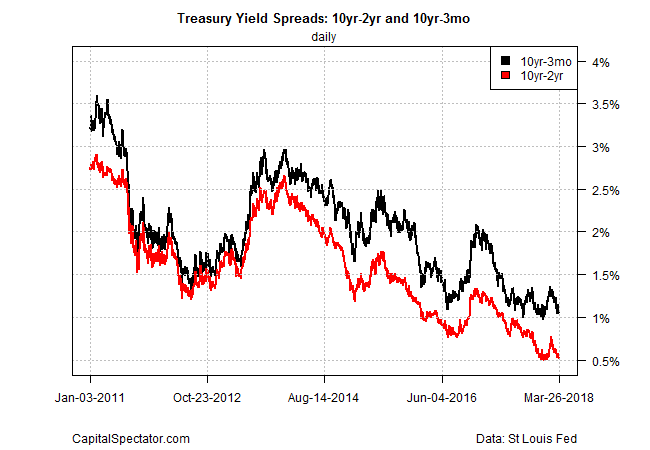

Mester’s comments coincided with a further narrowing of the yield spread based on the 10-year and 2-year Treasury rates. The yield difference between the two maturities fell to 52 basis points yesterday (Mar. 27), close to the lowest level since the recession ended in mid-2009. In January, the 10-year/2-year spread dipped to 50 basis points, a post-recession low.

This isn’t the first time that the Cleveland Fed President has raised doubts about the yield curve’s value for business-cycle analysis. Late last year, Bloomberg reported that she dismissed concerns that a flattening yield curve was a warning sign for the economy. “I just think long rates are going to go up given where we are in the economy and given where we see the economy going,” she said. “But this is another reason why we need to keep raising up the short rate.”

Fast forward nearly four months and current pricing in Fed funds futures supports Mester’s analysis. Following last week’s rate hike, CME this morning reports that Fed funds futures are pricing in a 96% probability that the central bank will raise rates again at the May 2 policy meeting.

Meanwhile, recession risk remains virtually nil, based on data published to date, according to yesterday’s February update of the Chicago Fed National Activity Index. The business cycle benchmark’s three-month moving average increased to +0.37, far above the -0.70 level that marks the start of economic contractions.

Related Posts

The 2016 Small-Cap Biotech Watchlist Debuts At The Biotech Showcase

The 2016 Small-Cap Biotech Watchlist Debuts At The Biotech Showcase Looking Into The Future Of Futures, Via The Latest CoT Report

Looking Into The Future Of Futures, Via The Latest CoT Report SP 500 And NDX Futures Daily Charts – Banking Troubles Worry Stocks

SP 500 And NDX Futures Daily Charts – Banking Troubles Worry Stocks Web 2.0 Business Vs. Politics

Web 2.0 Business Vs. Politics- USDCAD Daily Analysis – Thursday, Jan. 25

Polygon gas fees spike 1,000% amid Ordinals-inspired token craze

Polygon gas fees spike 1,000% amid Ordinals-inspired token craze

Leave A Comment