With the first overhaul of the US tax code in over 30 years passing this morning, US corporations in particular stand to do very well in 2018, and potentially even top their stellar performance from this year. The S&P 500 saw earnings grow nearly 10% in 2017, a yearly rate not seen since 2011. These companies have more cash on hand than they know what to do with, and while share buybacks dropped in 2017, dividends saw record levels, with CAPEX and R&D increasing as well.

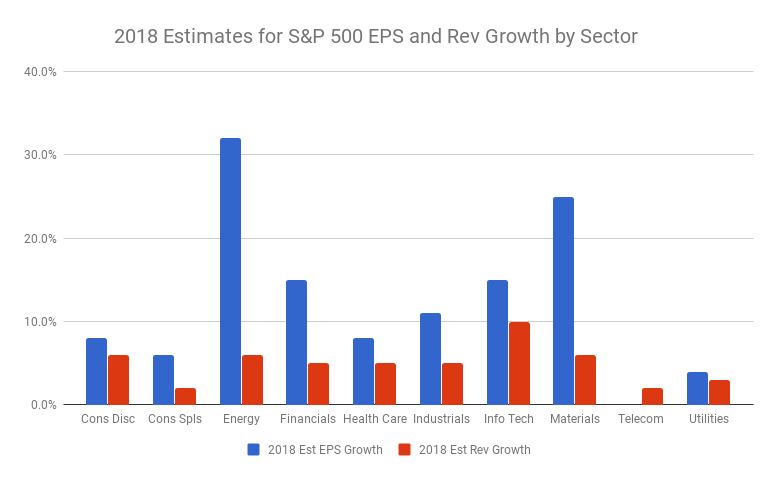

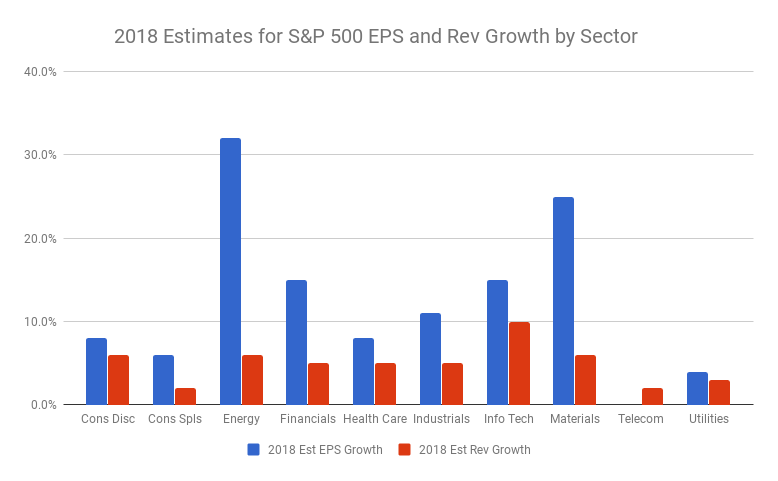

In the new year, S&P 500 earnings growth is expected to put up another 10%, the first time there have been two consecutive years of double-digit growth since 2010 and 2011. Furthermore, five of the ten sectors are estimated to put up double-digit year-over-year (YoY) growth.

After getting crushed in 2015 and 2016, commodities are back! The Energy and Materials sectors were the top two profit growers of 2017, and are expected to hold those titles again in the new year. Year-over-year comparisons are getting more difficult as prices in oil and metals normalizes, meaning the triple-digit profit growth seen for many of these names last year will remain a thing of the past. With that said, Energy is anticipated to put up hefty earnings per share (EPS) growth of 32% with Materials following closely behind at 25%.

Next up we have Financials and Information Technology, both expected see YoY EPS increase by 15%. Insurer’s helped boost the bottom line for the Financials sector in 2017, with analyst’s anticipating names like AIG, Progressive and Travelers will have a repeat performance this year. The big banks will also be one of the largest beneficiaries of a lower corporate tax rate, with Morgan Stanley calculating earlier in the year that a move to 20% rates from 35% would help deliver a double-digit increase in profits for their own bank, in addition to Bank of America, JPMorgan, Goldman Sachs and Wells Fargo. Only Citigroup would would see a single-digit increase due to a balance sheet that includes billions in deferred tax assets.

Leave A Comment