It is one thing to know a truth; it is quite another to witness that truth firsthand. Most investors know that bond prices move inversely to interest rates and that the longer the duration of the bond, the higher the sensitivity to interest rates. But witnessing that firsthand since last July has been jarring to many nonetheless.

Adding insult to injury for bond investors has been the sharp contrast with U.S. equities, which are 13-19% higher (S&P 500 – Russell 2000) since long bond yields bottomed last July. And as I have chronicled (see here and here), the equity advance in recent months has been among the lowest volatility moves in history.

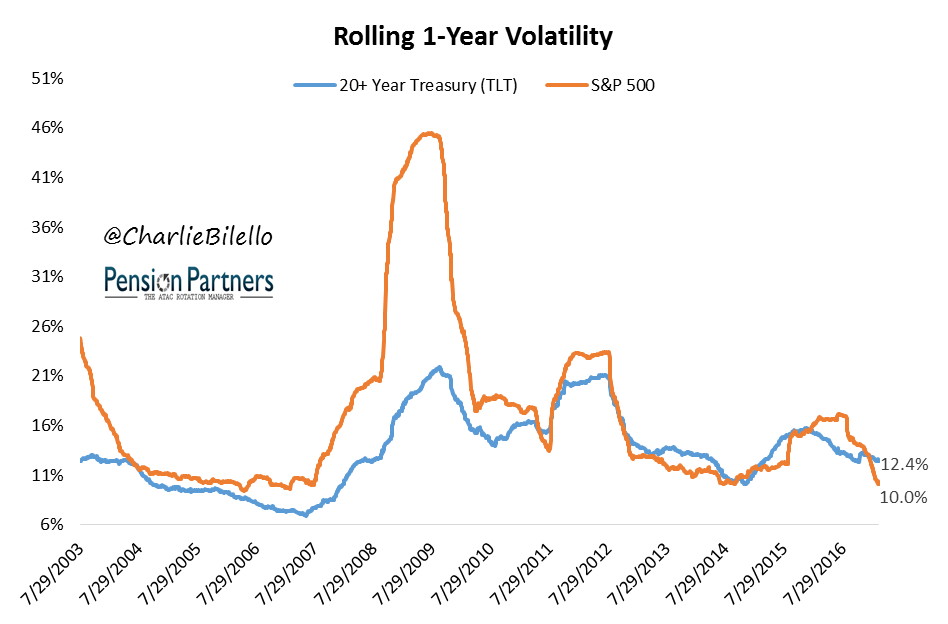

Over the past year, in fact, the S&P 500 has had an annualized volatility of only 10% (going back to 1928, that’s in the lowest 20% of volatility readings). At 12.4%, the volatility of the 20+ Year Treasury ETF (TLT ) has been higher.

On the loss side, long bonds have been exhibiting higher risk as well. Since the start of 2013, TLT has had three separate 15+% declines while the S&P 500 has had a maximum drawdown of only 13% (note: closing basis, total return).

Thus far in 2017, while the S&P 500 has had annualized volatility of only 6.5% and has hit all-time highs 15 times, long duration bonds are mired in an 18% drawdown.

So are long bonds riskier than stocks?

Over the past few years, they certainly have behaved as such. But over the longer-term (since inception of TLT in 2002), stocks have been far riskier.

What matters to investors, though, is not just how much risk they are taking, but how much they are being paid for that risk. Last July, bond investors were being paid very little for a higher level of risk (lower the yield, higher the duration, higher the volatility, given the same change in rates). Today they are being paid a bit more, which is good news for both volatility and return, for the single best predictor of bond returns are beginning yields.

Leave A Comment