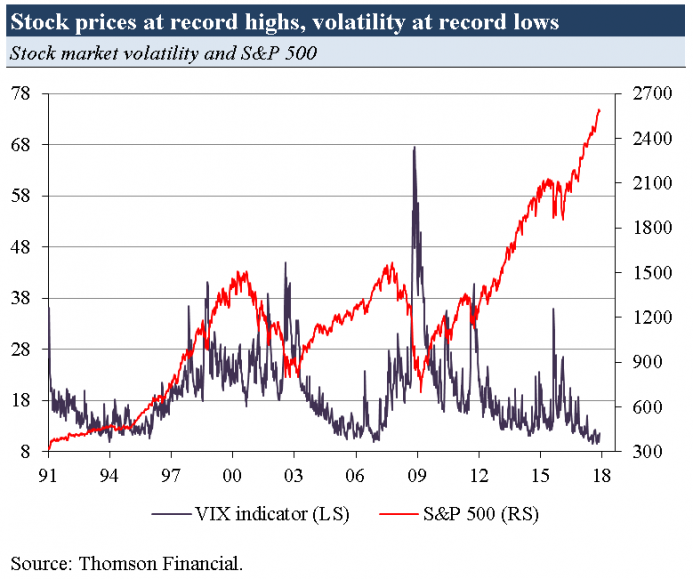

Indicators for financial market “stress” have reached their lowest levels in decades. For instance, stock market volatility has never been this low since the early 1990s. Credit spreads have been shrinking, and prices for credit default swaps have fallen to pre-crisis levels. In fact, investors are no longer haunted by concerns about the stability of the financial system, potential credit defaults, and unfavourable surprises in the economy or financial assets markets. How come?

Monetary policy plays the significant role. By slashing interest rates and ramping up the quantity of money in the banking system, central banks around the world have kick-started the economies following the 2008/2009 crash. But this is not the full story. The fact that investors expect central banks to stand at the ready to fend off a slowdown of the economy and price declines in stock and housing markets is by no means less important.

The truth is that investors expect central banks to provide a “safety net.” This expectation encourages them to make risky investments again (which they would otherwise have declined). That said, central banks have caused a colossal ‘moral hazard’: Investors feel pretty much assured that the risk-reward profile of their investments has become more favorable — that they can enjoy a considerable upside, while the downside is limited.

As a result, investors drive asset prices upwards. As stock prices rise, firms’ cost of capital falls, encouraging risky investments. Consumers, with their real estate assets appreciating, go into even more debt. Maturing debt is rolled over at low interest rates, and borrowers’ spending capacity increases. In other words: The downward manipulation of interest rates and the decline in risk aversion translates into a cyclical strengthening of the economy.

But wait: Will the Fed’s hiking of interest rates and the planned shrinking of its balance sheet not undo the very forces that have pushed economic activity back into positive territory? No, not necessarily. The crucial point is the Fed’s safety net: If investors continue to assume that the Fed willingly remains the ‘lender of last resort’, even a monetary policy of some short-term interest rate hiking is unlikely to do much harm to the current recovery.

Related Posts

US Economic Data ‘Death Cross’?

US Economic Data ‘Death Cross’? A Yen For Yen

A Yen For Yen New York Fed Spending Projections Rise At Top End, Sink At Bottom End: Wealth Effect?

New York Fed Spending Projections Rise At Top End, Sink At Bottom End: Wealth Effect? Markets In TurmOIL: Futures Plunge, Japan Enters Bear Market, Crude And Commodity Currencies Crash

Markets In TurmOIL: Futures Plunge, Japan Enters Bear Market, Crude And Commodity Currencies Crash Even after the pullback, this crypto trading algo’s $100 bag is now worth $20,673

Even after the pullback, this crypto trading algo’s $100 bag is now worth $20,673 Quanta Mechanics

Quanta Mechanics

Leave A Comment