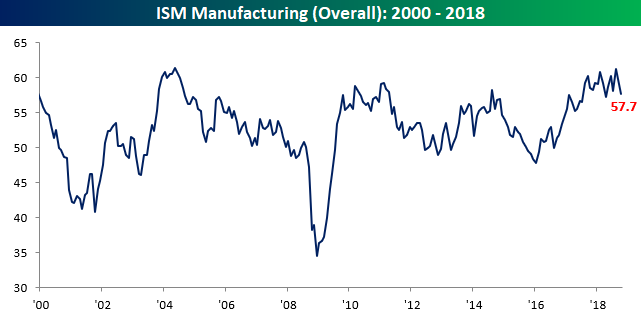

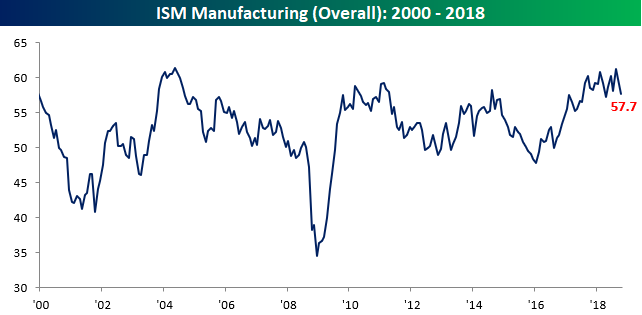

It was pretty widely expected that the ISM Manufacturing report for the month of October was going to show a slower rate of growth, and that’s exactly what we saw. While economists were forecasting the headline index to drop to 59.0 from last month’s reading of 59.8, the actual reading was much weaker at 57.7. That is the lowest reading for the headline index since April, and it was tied for the largest m/m decline since August 2016. Despite the decline and weaker than expected reading, the manufacturing sector is still expanding, but the rate of growth has slowed.

The table below breaks down this month’s report by each of the report’s subcomponents and shows their m/m and y/y changes. On a m/m and y/y basis, most components were down, but the disparity wasn’t all that wide. The only component that is in contraction mode is Customer Inventories, but it has been in the sub-50 range for quite some time now.

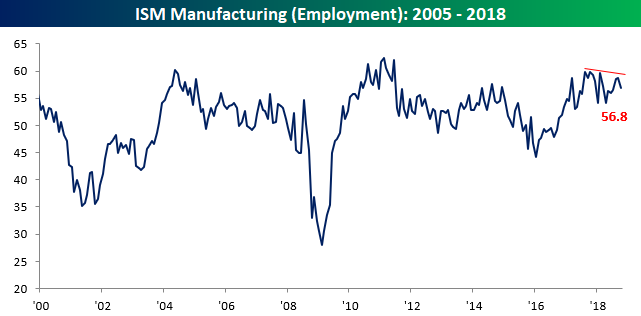

Heading into Friday’s Non-Farm Payrolls report, we wanted to highlight the employment component of this month’s ISM report. As shown above and in the chart below, October saw a two-point decline in the index putting in what is the second lower high since the peak last October. Again, the level of 56.8 still implies growth in employment for the manufacturing sector, just at a slower pace than last month and last year.

Finally, with respect to the commentary section of this month’s report, we wanted to highlight two trends that stand out- inflation and slower activity. The yellow highlights below indicate comments related to higher costs or upward pricing pressures (there’s a lot of them!), while the purple highlights commentary from the Machinery and Fabricated Metals sectors indicating a potential slowdown in the pace of business activity.

Related Posts

Genuine Parts Company Dividend Stock Analysis

Genuine Parts Company Dividend Stock Analysis Market Talk – April 7, 2016

Market Talk – April 7, 2016 Nigerian crypto payment startup shuts down, offers IP for sale

Nigerian crypto payment startup shuts down, offers IP for sale How Warren Buffett Makes The Economy Better Off – And Average People Too

How Warren Buffett Makes The Economy Better Off – And Average People Too 5 Undervalued Companies For The Defensive Investor Near 52 Week Lows – October 2015

5 Undervalued Companies For The Defensive Investor Near 52 Week Lows – October 2015 Kennametal Working Tools Direct From Pittsburgh

Kennametal Working Tools Direct From Pittsburgh

Leave A Comment